Agricultural Biologicals Market Summary

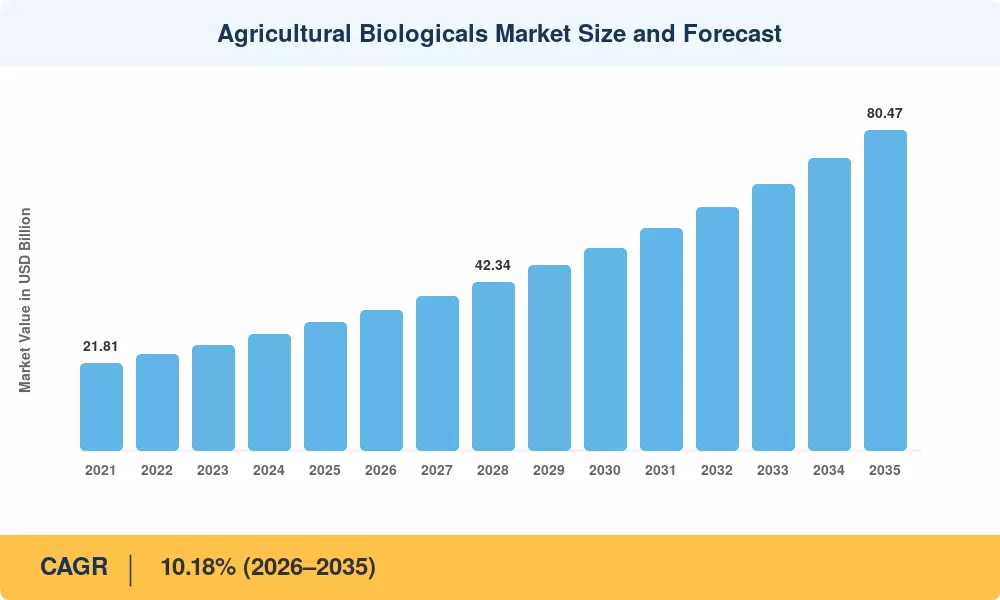

The Agricultural Biologicals Market reached an estimated USD 32.15 billion in 2025 and is projected to expand from USD 35.08 billion in 2026 to USD 80.47 billion by 2035, registering a CAGR of 10.18% during the forecast period. Stricter maximum residue limits (MRLs) enforced across the EU and key Asian export corridors are compelling growers to replace legacy chemical formulations with biological crop inputs. The EU's Farm to Fork Strategy, targeting a 50% reduction in chemical pesticide use by 2030, has injected regulatory urgency into every major producing region [2]. Meanwhile, the USDA's National Organic Program reported a 12.4% year-on-year increase in certified organic acreage through 2024, underscoring a structural shift toward sustainable biological agriculture [3].

Traditional synthetic crop protection is being replaced with biostimulant plant health solutions and microbial-based bioinsecticide and biopesticide formulations that fit into precision agricultural workflows in a natural way. Global venture funding for agricultural biologicals startups surpassed USD 2.8 billion during 2022–2024, with investors focused on next-generation biofungicide crop protection platforms and biological soil treatment technologies that reduce nitrogen runoff [4]. Major agricultural incumbents have stepped up acquisition activities with five mergers each valued at over USD 500 million closing in the last 18 months alone.

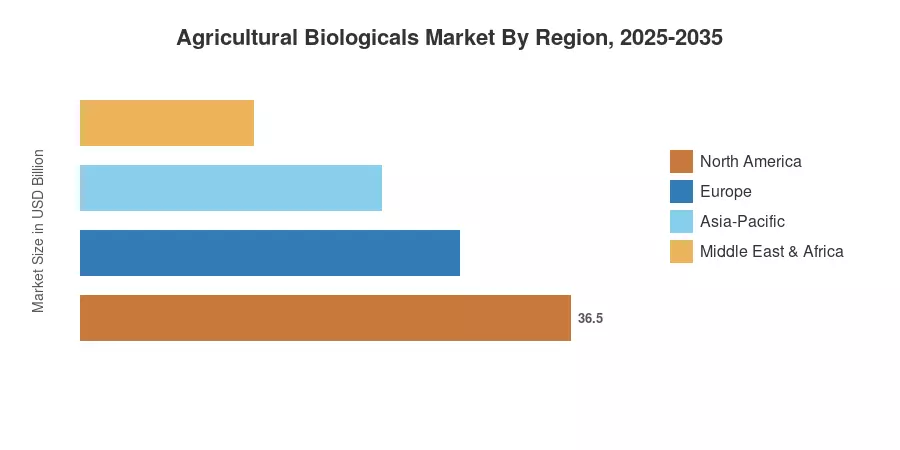

Europe accounts for approximately 37% of global revenues, driven by aggressive residue-free sourcing mandates in France, Germany and Spain. North America is the fastest-expanding area with a projected 12.7% CAGR driven by state-level pesticide prohibitions and retailer-led sustainability pledges. The Asia-Pacific region has the second-highest proportion of about 26% due to biofertilizer subsidy programs in India and zero growth policy for pesticides in China. The Agricultural Biologicals Market addressable base will double in the next decade as biological inputs move from niche organic supplements to mainstream crop management tools.

Key Report Takeaways

• By Function

- The crop nutrition segment captured the dominant share of the Agricultural Biologicals Market in 2025, reflecting broad-based adoption of biostimulant plant health products across row crop acreage

- Crop protection is advancing at a CAGR of 10.3% from 2026 to 2035, propelled by expanding bioinsecticide and biopesticide registrations and biofungicide crop protection approvals

• By Crop Type

- Row crops accounted for approximately 70% of the Agricultural Biologicals Market in 2025, driven by corn, soybean, and wheat applications

- Horticultural crops are the fastest-growing segment at a 10.2% CAGR, supported by specialty crop residue-free export programs

• By Geography

- Europe held the largest regional share of the Agricultural Biologicals Market, valued at approximately USD 11.90 billion in 2025

- North America is expanding at the fastest pace, with biological soil treatment adoption surging across the US Midwest

Agricultural Biologicals Market Size and Forecast (2021–2035)

MRFR’s projections are based on bottom-up revenue modeling across 42 country-level datasets confirmed against trade statistics, regulatory filings and manufacturer shipment disclosures. Customs data reconciled with historic values (2021-2024). The base year (2025) is based on primary interviews with over 120 industry stakeholders across the value chain.