Market Analysis

In-depth Analysis of Automotive Semiconductor Market Industry Landscape

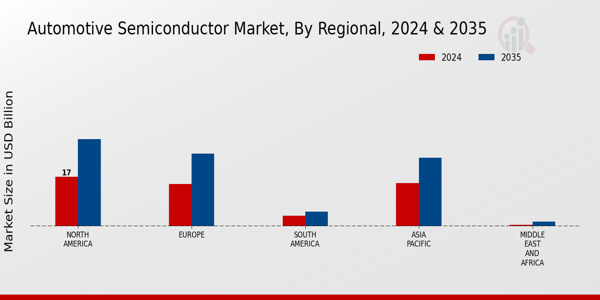

The global automotive semiconductor market is set to reach US$ 85,727.8 MN by 2030, at an 8.6% CAGR between years 2023-2030. The market is transforming with the fast evolution of automotive industry towards electrification, connectivity and ADAS features. This market’s dynamics are closely related to the broader forces driving automotive industry. Vehicle demand has increased to incorporate more electronic components in automotive designs that promote safety, performance, and a better driving experience. The rising use of electric vehicles (EVs) is one major force behind market dynamics. With the increasing carbon footprint of mankind, automotive companies are spending enormous amounts on electric powertrains. This transition necessitates a dramatic increase in semiconductor content to drive different elements including electric motors, power management systems and battery management system. Therefore, semiconductor suppliers are adapting their approaches to match the increasing need for these high-end components. Another important aspect to define the market for automotive semiconductors is connectivity. From the point of view, answers to connected cars and autonomy become possible only due to advanced semiconductor technologies. The advent of high-end infotainment systems, V2X communication and sensor fusion technologies require powerful semiconductors. In this segment, innovation has been driven by the demand for reliable and high-speed connectivity solutions. Semiconductor companies are also racing to develop modern technologies that can be used in addressing issues considered unique to an automotive environment. Secondly, ADAS growth has become a key pillar in the improvement of vehicle safety and driving experience. Semiconductors have a critical function in providing the sensors, cameras, radar systems and processing units that provide features such as adaptive cruise control, lane keeping assistance and automatic emergency braking. In automotive, growth in demand for specialized chips specifically designed to handle complex algorithms and real-time processing of data has been observed due to the nature of these safety critical applications. However, the market dynamics are not free from challenges. A key challenge for the automotive semiconductor industry is supply chain constraints that have risen over time. Such causes as increased demand, geopolitical tensions and aftermath of COVID-19 has led to the shortage worldwide in semiconductors that also impacted a wide range of sectors including automobile industry. This has prompted the stakeholders to reassess and possibly consider measures for supplying future risks. One of the remarkable characteristics in market dynamics is increasing competition between semiconductors manufacturers. The traditional players are facing competition from new entrants, and strategic partnerships and collaborations have become very common. Companies try to unite efforts in order to realize synergies and apply collective knowledge for overcoming the specific needs of automotive industry.

Leave a Comment