Certified Global Research Member

Key Questions Answered

- Global Market Outlook

- In-depth analysis of global and regional trends

- Analyze and identify the major players in the market, their market share, key developments, etc.

- To understand the capability of the major players based on products offered, financials, and strategies.

- Identify disrupting products, companies, and trends.

- To identify opportunities in the market.

- Analyze the key challenges in the market.

- Analyze the regional penetration of players, products, and services in the market.

- Comparison of major players’ financial performance.

- Evaluate strategies adopted by major players.

- Recommendations

Why Choose Market Research Future?

- Vigorous research methodologies for specific market.

- Knowledge partners across the globe

- Large network of partner consultants.

- Ever-increasing/ Escalating data base with quarterly monitoring of various markets

- Trusted by fortune 500 companies/startups/ universities/organizations

- Large database of 5000+ markets reports.

- Effective and prompt pre- and post-sales support.

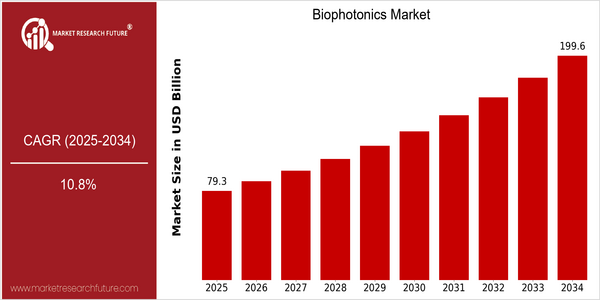

Market Size Snapshot

| Year | Value |

|---|---|

| 2025 | USD 79.31 Billion |

| 2034 | USD 199.64 Billion |

| CAGR (2025-2034) | 10.8 % |

Note – Market size depicts the revenue generated over the financial year

The biophotonics market is undergoing a remarkable growth, with a current market value of $ 79.31 billion in 2025, and a forecast of $ 199.64 billion by 2034. This is a CAGR of 10.8 % over the forecast period. The growing demand for diagnostics and medical treatment and the rising prevalence of chronic diseases are the main drivers of this growth. In addition, the integration of biophotonics into various applications, such as drug discovery, environment monitoring and food safety, will further enhance its market potential. Technological developments, such as the development of new diagnostic tools and therapies, are expected to drive the market growth. And biophotonics industry leaders, such as Hamamatsu, Carl Zeiss AG and Olympus, are constantly investing in research and development to launch new products and expand their market share. Strategic initiatives, such as establishing strategic alliances and collaborating with various players to enhance product capabilities and market presence, further demonstrate the industry's dynamism. As the biophotonics market develops, it is expected to play an important role in the future of medicine and related fields.

Regional Market Size

Regional Deep Dive

The biophotonics market is experiencing significant growth in all regions, owing to technological advances in medical science, the growing demand for non-intrusive diagnostic procedures, and the increasing emphasis on individualized medicine. Each region has its own distinct characteristics, which are influenced by the economic conditions, regulations, and technological innovations. North America leads in research and development, Europe focuses on innovation and regulation, and Asia-Pacific is rapidly adopting biophotonics devices as its healthcare system develops. The Middle East and Africa are undergoing rapid growth as a result of government initiatives to improve the quality of medical care. Latin America is gradually embracing biophotonics as a means to modernize its healthcare system.

Europe

- The European Union's Horizon 2020 program is funding numerous biophotonics research projects, fostering collaboration between academia and industry to drive innovation.

- Regulatory changes in the EU are pushing for stricter compliance in medical device manufacturing, which is leading companies to invest in more sophisticated biophotonics technologies to meet these standards.

Asia Pacific

- Countries like China and India are rapidly expanding their healthcare infrastructure, leading to increased adoption of biophotonics technologies for diagnostics and treatment.

- Innovations in laser technology and imaging systems are being spearheaded by companies such as Olympus Corporation and Nikon Corporation, enhancing the capabilities of biophotonics applications in the region.

Latin America

- Brazil is seeing a rise in biophotonics research, supported by government grants aimed at improving healthcare technologies and diagnostics.

- Local companies are beginning to collaborate with international firms to enhance their biophotonics capabilities, particularly in the areas of imaging and therapeutic devices.

North America

- The U.S. Food and Drug Administration (FDA) has recently streamlined the approval process for biophotonics devices, encouraging innovation and faster market entry for new technologies.

- Key players like Hamamatsu Photonics and Thermo Fisher Scientific are investing heavily in R&D to develop advanced biophotonics solutions, particularly in the fields of cancer diagnostics and imaging.

Middle East And Africa

- Governments in the UAE and Saudi Arabia are investing in healthcare modernization initiatives, which include the integration of biophotonics technologies in medical facilities.

- Collaborations between local universities and international firms are emerging, focusing on research and development in biophotonics, particularly in diagnostics and therapeutic applications.

Did You Know?

“Biophotonics is not only used in medical diagnostics but also plays a crucial role in agricultural applications, helping to monitor plant health and optimize crop yields.” — International Society for Optics and Photonics (SPIE)

Segmental Market Size

Biophotonics is a growing field, and one of the most promising of the future. It is based on the advancement of medical technology and the increased demand for non-intrusive diagnostic methods. The increasing number of chronic diseases requires more and more accurate diagnostics, and the growing trend towards individualization of treatment, which is being met by biophotonics, will continue to increase the development of this field. In addition, the regulatory framework, which favors the use of new medical technology, is also expected to further increase the dynamics of the market. At present, the biophotonics industry is in a transitional period from a pilot stage to full-scale implementation. The leading companies in this field are Hamamatsu Photonics and PerkinElmer. The main applications of biophotonics are in medical diagnostics, in which biophotonics is used for early disease diagnosis, and in medical therapy, for example, photodynamic therapy for cancer treatment. The most important trends accelerating the growth of the market are the continuous search for sustainable solutions in health care and the impact of global health crises on the need for rapid and effective diagnostic tools. The main trends in this market are optical coherence tomography and fluorescence.

Future Outlook

The Biophotonics Market is expected to grow at a CAGR of 10.8% from 2025 to 2034. This growth is based on the increasing adoption of biophotonics in medical diagnostics, therapeutic applications, and in the field of the environment. The penetration of biophotonics in clinical settings is expected to reach over 60% by 2034, from about 30% in 2025. In addition, technological advances such as the development of advanced optical imaging systems and the integration of artificial intelligence into biophotonics applications will also drive market growth. Furthermore, government initiatives to promote research and development in biophotonics will increase innovation and access. In addition, the growing importance of personalized medicine and the rising prevalence of chronic diseases will accelerate the adoption of biophotonics. In view of these factors, biophotonics market players must prepare for a dynamic environment with rapid technological development and expanding application areas, and be able to take advantage of the opportunities that lie ahead.

Covered Aspects:| Report Attribute/Metric | Details |

|---|---|

| Market Size Value In 2022 | USD 58.3 Billion |

| Market Size Value In 2023 | USD 64.6 Billion |

| Growth Rate | 10.80% (2023-2032) |

Biophotonics Market Highlights:

Leading companies partner with us for data-driven Insights

Kindly complete the form below to receive a free sample of this Report

Tailored for You

- Dedicated Research on any specifics segment or region.

- Focused Research on specific players in the market.

- Custom Report based only on your requirements.

- Flexibility to add or subtract any chapter in the study.

- Historic data from 2014 and forecasts outlook till 2040.

- Flexibility of providing data/insights in formats (PDF, PPT, Excel).

- Provide cross segmentation in applicable scenario/markets.