Butter Market Summary

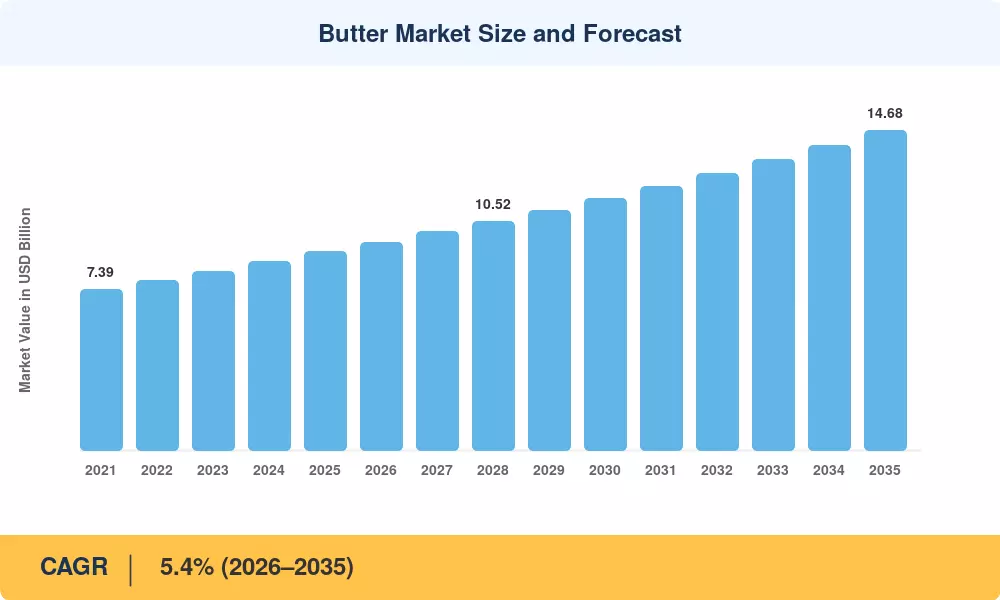

The global Butter Market reached an estimated USD 9.12 billion in 2025, with the forecast period beginning at USD 9.61 billion in 2026 and climbing to USD 14.68 billion by 2035 at a CAGR of 5.4%. Two forces anchor this trajectory: rising per-capita dairy fat consumption in developing economies and a decisive consumer pivot toward premium, minimally processed fats across North America and Western Europe. Government dairy-support programs — India's National Dairy Plan II alone allocated over USD 310 million for productivity upgrades — continue to underwrite supply-side expansion [2].

A quiet transformation is reshaping how butter reaches consumers. Industrial margarine and hydrogenated spreads, once dominant in food-service kitchens and retail shelves, are losing ground to cultured European-style butter, grass-fed organic butter, and clarified ghee butter product lines that command 20–40% price premiums. Retail private-label brands invested an estimated USD 1.4 billion globally in dairy-case reformulations between 2022 and 2024, accelerating the shift toward clean-label butter spreads food service channels now demand [3].

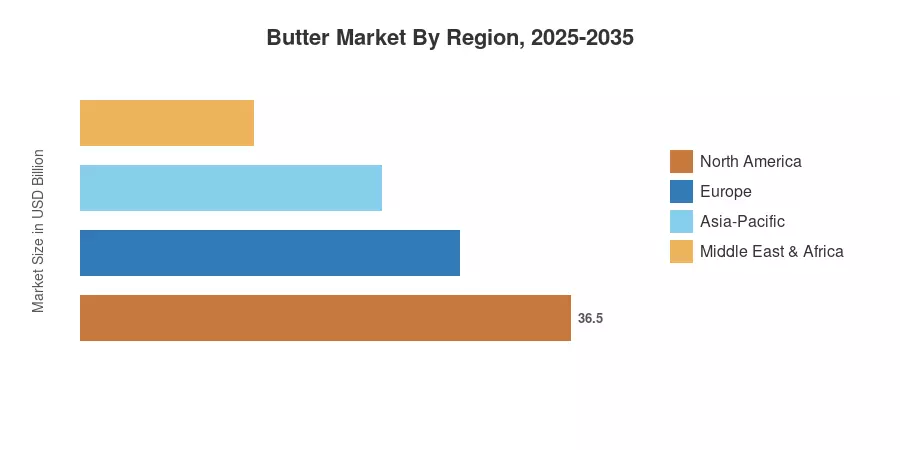

Europe holds the dominant share of the Butter Market at roughly 38%, driven by France, Germany, and Ireland's deeply embedded butter-centric culinary traditions. Asia-Pacific is the fastest-growing region with a projected CAGR of 6.8%, powered by India's expanding organized dairy sector and China's growing bakery segment. North America accounts for approximately 27% of global value, where the plant-based butter alternative category is adding competitive pressure that, paradoxically, has lifted awareness and overall category spending

Key Report Takeaways

• By Product Type

- Salted butter commands the largest revenue share in the Butter Market at approximately 42%, reflecting its dominance in household and food-service applications

- Cultured European-style butter is projected to grow at a CAGR of 7.1% through 2035, fueled by artisan bakery demand and premiumization trends

- Clarified ghee butter product revenues reached an estimated USD 1.38 billion in 2025, driven by South Asian diaspora consumption and Ayurvedic wellness positioning

• By Distribution Channel

- Supermarkets and hypermarkets account for roughly 51% of the Butter Market by value, though e-grocery channels are closing the gap

- Butter spreads food service distribution is expanding at 5.9% CAGR as quick-service restaurants reformulate menus around real-butter positioning

• By Geography

- Europe leads the Butter Market with a 38% share, anchored by EU Protected Designation of Origin programs

- Asia-Pacific is growing at 6.8% CAGR, with India alone accounting for over 45% of regional volume

- North America's Butter Market generates approximately USD 2.46 billion, with grass-fed organic butter as the fastest-growing sub-category

Market Size and Forecast (2021–2035)

MRFR's sizing methodology triangulates top-down revenue data from national dairy boards, FAO production statistics, and bottom-up channel audits across 32 countries. Historical values (2021–2024) are validated against customs trade data; forecast values (2026–2035) apply econometric modeling adjusted for demographic shifts, dietary trend indices, and commodity price scenarios.

.webp?v=1785231588)