Ceiling Fan Market Summary

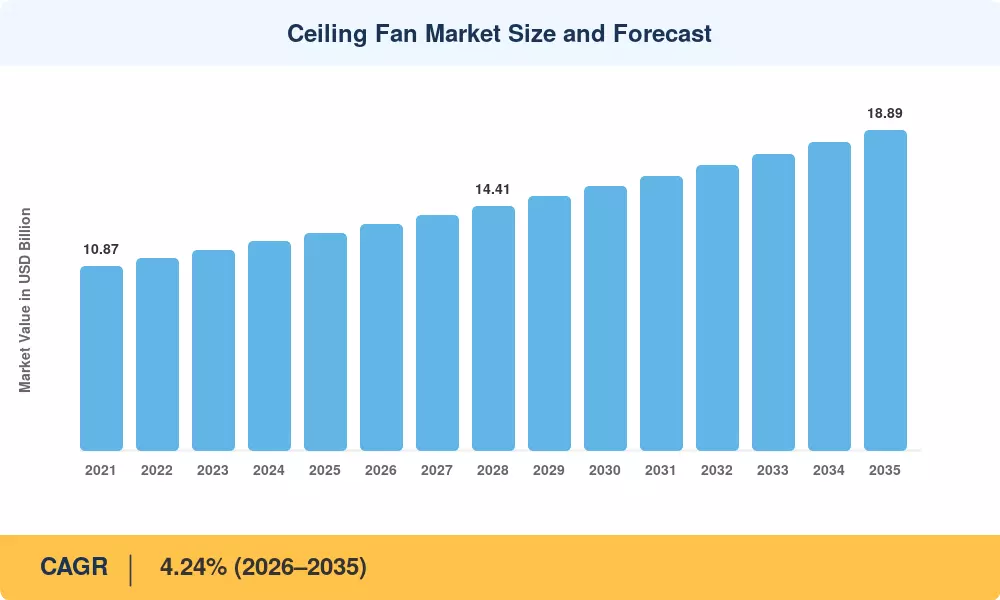

The Ceiling Fan Market reached an estimated USD 12.83 billion in 2025 and is projected to grow from USD 13.52 billion in 2026 to USD 18.89 billion by 2035, registering a CAGR of 4.24% during the forecast period. Government-led energy-efficiency mandates — including the U.S. Department of Energy's updated ceiling fan energy conservation standards effective 2025 and India's Bureau of Energy Efficiency (BEE) star-rating expansion — are creating a regulatory floor that accelerates replacement demand across residential and commercial segments [2]. The Ceiling Fan Market is benefiting from urbanization rates exceeding 55% globally, which drives new housing construction and retrofit activity in equal measure.

A technology transition is remolding the Ceiling Fan Market from motor outwards. The majority of the installed base is still legacy AC induction designs, although these are slowly being replaced with energy-efficient BLDC ceiling fan types that use 50–65% less electricity at equivalent airflow. For instance, India’s EESL bulk-procurement program alone has targeted the distribution of over 10 million BLDC units by 2026 with USD 180 million in subsidy support [3]. Commodity appliance now a connected-home node via smart Wi-Fi ceiling fan controls that integrate with voice assistants and home-automation hubs that increase average selling prices 18–25% per unit.

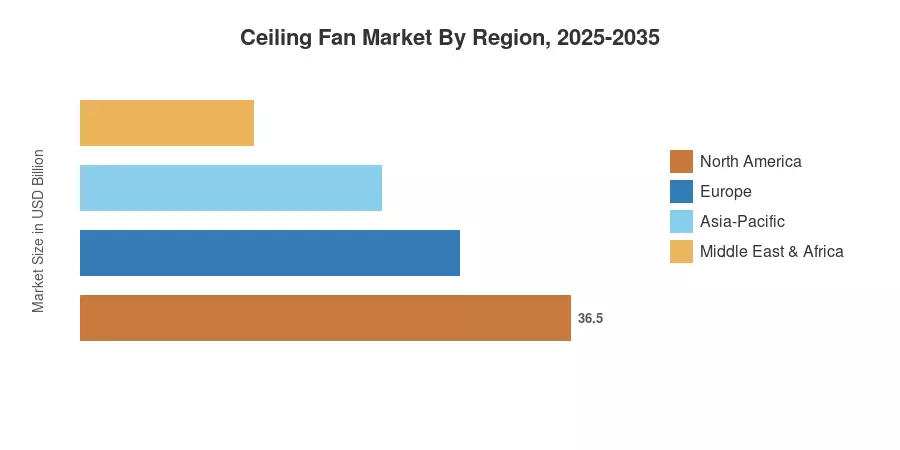

The Asia-Pacific region accounts for over 52% of the Ceiling Fan Market, led by India and China, where tropical and sub-tropical temperatures support demand throughout the year. The region also registers the fastest CAGR at 5.48% until 2035. North America is the second largest contributor to the market with a share of over 21%. The decorative ceiling fan with light upgrades in the renovation channel in this region is expected to boost the market. Southern Europe hospitality venues drive Europe expansion through usage of outside weatherproof ceiling fans. In the next decade, ceiling fan installation service networks and quick-commerce delivery models will further shorten the purchase-to-use cycle, providing support for the increasing trajectory of the Ceiling Fan Market [4].

Key Report Takeaways

• By Product Type

- Standard 3-blade AC models held approximately 40% of the Ceiling Fan Market in 2025, though their share is declining as consumers trade up to decorative and energy-savings variants

- Energy-efficient BLDC ceiling fan models are forecast to expand at a 5.81% CAGR through 2035, outpacing all other product categories in the Ceiling Fan Market

• By Technology

- AC motor-based fans captured about 58% share of the Ceiling Fan Market in 2025, a position that will erode as regulatory minimums tighten

- BLDC motor fans are projected to grow at a 6.60% CAGR to 2035, making them the fastest-growing technology segment

• By End User

- Residential applications accounted for roughly USD 9.73 billion in 2025, reflecting the dominance of household demand

- Commercial applications are expected to rise at a 5.65% CAGR through 2035 as hospitality and retail facilities adopt smart Wi-Fi ceiling fan control systems

• By Distribution Channel

- Multi-brand retail stores represented about 42% of distribution in 2025, though online channels are compressing that lead

- Online sales are advancing at a 6.23% CAGR to 2035, supported by quick-commerce platforms and ceiling fan installation service bundling

• By Region

- Asia-Pacific generated the largest regional share of the Ceiling Fan Market in 2025 and is on track for the fastest growth at 5.48% CAGR

- North America held approximately 21% regional share, driven by decorative ceiling fans with light replacement cycles

Ceiling Fan Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s sizing methodology triangulates manufacturer shipment data, import/export customs records, and distributor sell-through figures across 42 countries. Historical values (2021–2024) are validated against national appliance-industry associations; forecasts (2026–2035) apply a bottom-up build from segment-level demand models calibrated to macroeconomic indicators, including housing starts, urbanization rates, and electricity tariff trends.