E commerce Market Summary

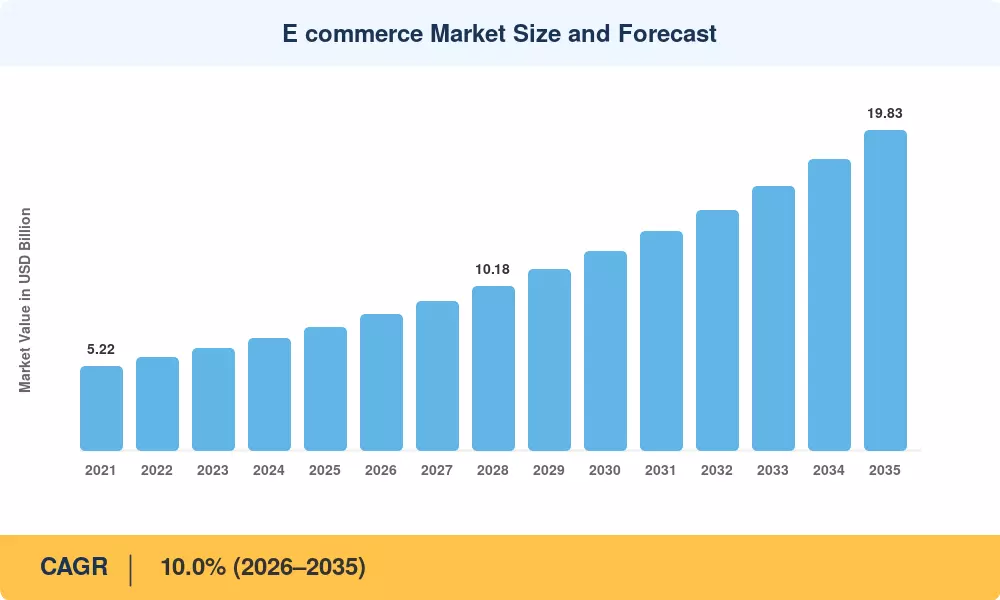

The global E Commerce Market reached an estimated USD 7.65 trillion in 2025 and is projected to grow from USD 8.42 trillion in 2026 to USD 19.83 trillion by 2035, registering a CAGR of 10.0% during the forecast period (2026–2035). This expansion is anchored in two converging forces: the worldwide proliferation of smartphone-connected consumers — with mobile internet penetration crossing 5.5 billion users in 2025 [2] — and aggressive government-led digital economy programs such as India's Digital India initiative and the EU's Digital Markets Act, both of which are reshaping how goods and services flow through e-commerce platforms [3].

A structural transformation is underway across the E Commerce Market as legacy monolithic storefronts give way to headless commerce for omnichannel retail architectures that decouple front-end experiences from back-end operations. Retailers invested over USD 22 billion globally in AI-powered product recommendation engines during 2024 alone, driving conversion-rate improvements of 15–25% for early adopters. D2C direct-to-consumer e-commerce platforms are dismantling traditional wholesale distribution, enabling brands to own the customer relationship end-to-end while leveraging mobile-first e-commerce checkout optimization to reduce cart abandonment rates below 55% for the first time [5].

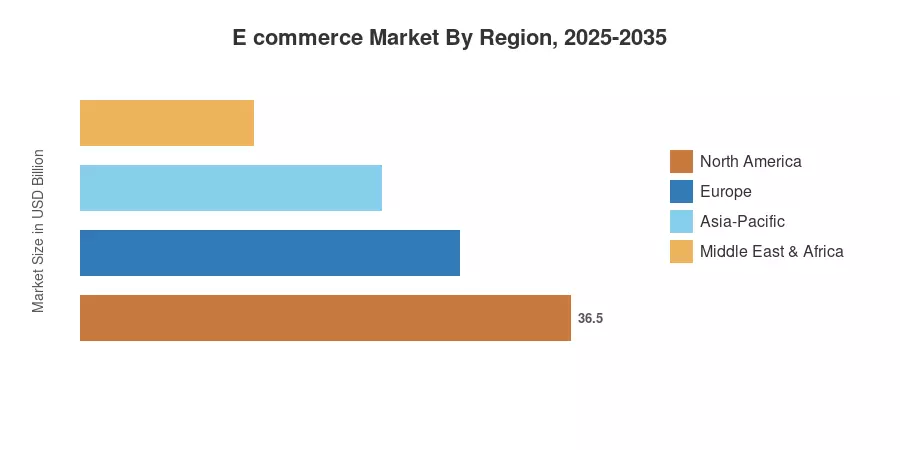

Asia-Pacific commands the largest share of the E Commerce Market at roughly 42.5%, led by China's mature ecosystem and India's rapid digital payments adoption. South America is emerging as the fastest-growing region with an estimated CAGR of 13.8%, fueled by fintech expansion and cross-border e-commerce logistics and compliance improvements across Brazil and Mexico [6]. North America holds approximately 24.3% of the global value, driven by subscription commerce and same-day delivery infrastructure. The E Commerce Market trajectory through 2035 will be defined by how quickly sellers adopt composable technology stacks and how effectively regulators harmonize cross-border trade rules.

Key Report Takeaways

• By Business Model

- D2C direct-to-consumer e-commerce platforms account for approximately 18.5% of total E Commerce Market revenue in 2025, driven by lower customer acquisition costs and direct data ownership

- Marketplace model remains the dominant format, projected to grow at a CAGR of 10.6% through 2035, supported by network effects and seller aggregation

- Subscription commerce is the fastest-growing model segment within the E Commerce Market, registering 12.1% CAGR

• By Product Category

- Electronics & media represent the largest product vertical at approximately USD 1.98 trillion in 2025

- Fashion & apparel are expanding at 11.3% CAGR, propelled by virtual try-on features and AI-powered product recommendation engines

- Grocery & fresh food capture roughly 9.2% of the E Commerce Market, accelerating post-pandemic

• By Region

- Asia-Pacific leads the E Commerce Market with 42.5% share, anchored by China, India, and Southeast Asia

- South America posts the highest regional CAGR at 13.8%, with Brazil and Mexico driving growth

- Europe holds approximately 20.1% of global value, with headless commerce for omnichannel retail adoption accelerating in the UK and Germany

E Commerce Market Size and Forecast (2021–2035)

MRFR's market sizing combines top-down revenue modeling from national statistical agencies and e-commerce industry bodies with bottom-up aggregation of platform GMV disclosures, payment processor data, and logistics throughput analysis. Historical figures (2021–2024) rely on audited filings and government trade data; forecasts (2026–2035) apply econometric modeling with adjustments for mobile-first e-commerce checkout optimization adoption curves, regulatory shifts, and macroeconomic scenarios.

.webp?v=1783339232)