Email Encryption Market Summary

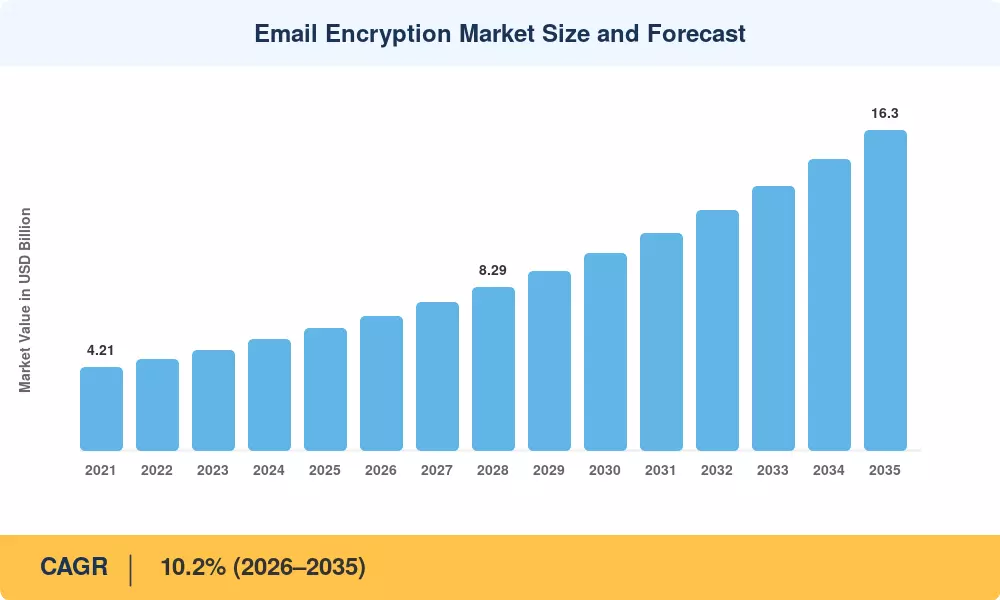

The Email Encryption Market stood at an estimated USD 6.2 billion in 2025 and is projected to grow from USD 6.8 billion in 2026 to USD 16.3 billion by 2035, registering a CAGR of 10.2% during the forecast period (2026–2035). This expansion is anchored in the accelerating wave of data privacy regulation worldwide — the EU's enforcement of GDPR Article 32 mandating encryption of personal data, and the U.S. Cybersecurity and Infrastructure Security Agency (CISA) pushing zero-trust architecture across federal agencies — both of which have placed email data loss prevention with encryption at the center of enterprise security roadmaps [2][3].

A fundamental technology shift is reshaping how organizations secure electronic correspondence. Legacy perimeter-based gateway solutions are giving way to end-to-end encrypted enterprise email solutions that protect messages from sender to recipient without relying on intermediary decryption. Gartner estimated that enterprise spending on messaging security — including TLS encryption for email in transit and S/MIME and PGP email encryption standards — exceeded USD 3.9 billion globally in 2024, reflecting a 14% year-over-year increase. Microsoft's native integration of sensitivity labels with encryption in Microsoft 365, and Google's client-side encryption rollout for Workspace, have moved cloud email encryption for Microsoft 365 and Google Workspace from a niche add-on to a mainstream expectation.

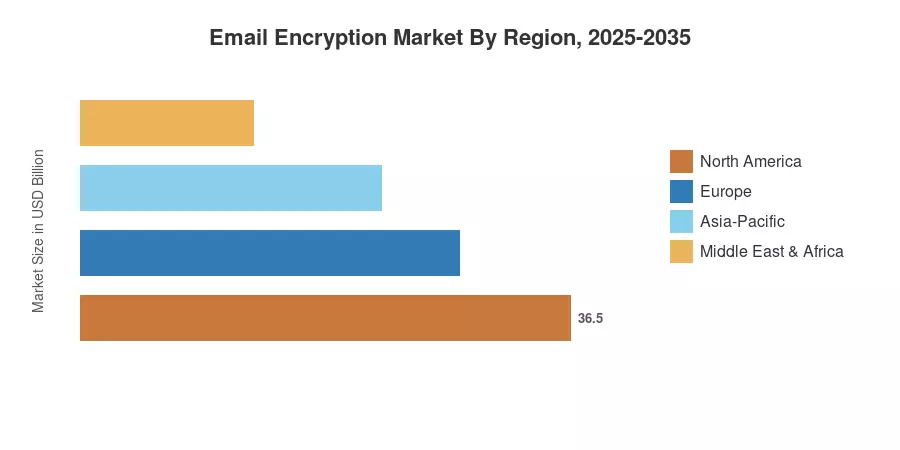

North America commands approximately 38% of the Email Encryption Market, driven by stringent HIPAA, GLBA, and CMMC requirements across healthcare, finance, and defense. Asia-Pacific is the fastest-growing region at a projected 13.8% CAGR, propelled by India's Digital Personal Data Protection Act 2023 and China's expanding cybersecurity law enforcement. Europe holds the second-largest share at roughly 28%, where GDPR compliance obligations continue to fuel demand for email data loss prevention with encryption across both public and private sectors [5]. The next decade will see encryption shift from a compliance checkbox to a foundational layer of enterprise communication infrastructure.

Key Report Takeaways

• By Component

- Cloud-based deployment dominates the Email Encryption Market, accounting for approximately 58% of total revenue in 2025, as organizations migrate to hosted security stacks that simplify key management and policy enforcement

- Gateway encryption solutions are projected to register a CAGR of 9.4% through 2035, driven by regulated industries requiring centralized policy control over TLS encryption for email in transit

- Services (managed and professional) contributed USD 1.9 billion in 2025, reflecting growing demand for outsourced encryption operations among mid-market enterprises

• By End-User Vertical

- BFSI leads the Email Encryption Market with a 26% revenue share, as financial regulators worldwide mandate encrypted communications for customer data handling

- Healthcare is the fastest-growing vertical at 12.6% CAGR, fueled by HIPAA enforcement actions and the proliferation of telehealth correspondence containing protected health information

- Government and defense spending on end-to-end encrypted enterprise email solutions reached approximately USD 870 million in 2025

• By Region

- North America generated USD 2.36 billion in 2025, anchored by U.S. federal zero-trust mandates

- Asia-Pacific is expanding at 13.8% CAGR, with India and China driving adoption through new data protection legislation

- Europe holds a 28% share of the Email Encryption Market, sustained by GDPR and the EU Cybersecurity Act requirements

MARKET RESEARCH FUTURE (MRFR)'s market sizing combines bottom-up revenue estimates from vendor financial disclosures, IDC and Gartner tracker databases, enterprise procurement surveys across 14 countries, and triangulation against regulatory compliance spending benchmarks published by NIST and ENISA. Historical figures (2021–2024) reflect reported revenues, while the base year (2025) and forecast period (2026–2035) apply econometric modeling calibrated to IT security budget growth, cloud migration rates, and regulatory enforcement timelines.