Emulsifiers Market Summary

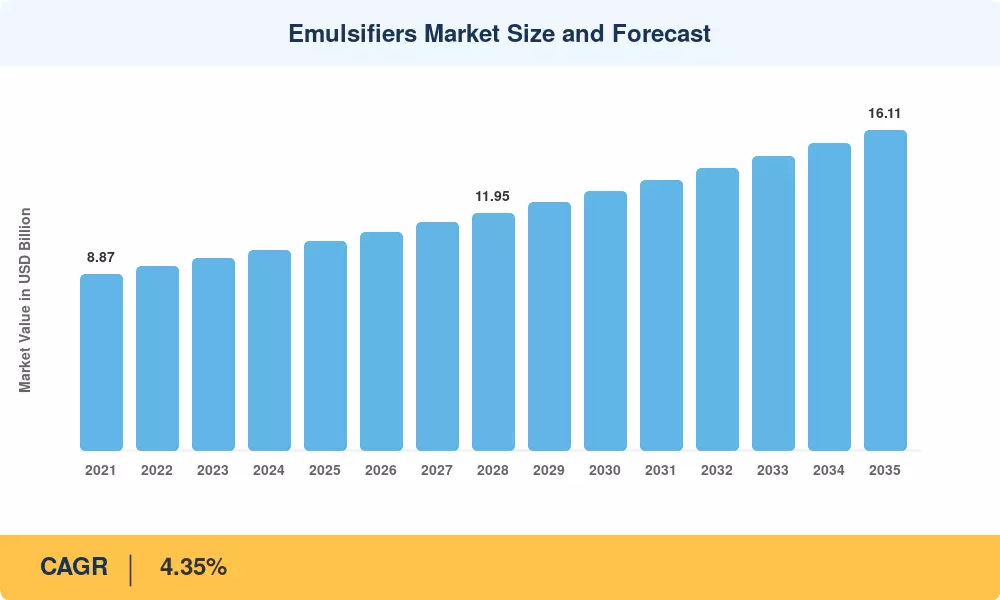

The global Emulsifiers Market stood at USD 10.52 Billion in 2025 and is projected to grow from USD 10.98 Billion in 2026 to USD 16.11 Billion by 2035, registering a CAGR of 4.35% across the forecast period (2026–2035). That steady expansion is anchored in two powerful catalysts: the worldwide shift toward packaged and processed food consumption, and tightening clean-label regulations that push manufacturers toward next-generation food emulsifier ingredients and bio-based surfactant chemicals. Government food-safety programs — including the EU's Farm-to-Fork Strategy and FSSAI's revised additive standards in India — are accelerating reformulation cycles, pulling demand for advanced stabilizing agents across bakeries, dairy, and confectionery.

Across the specialty chemical value chain, legacy petroleum-derived formulation stabilizers are progressively giving way to bio-based emulsification platforms. The global bio-surfactant sector attracted over USD 1.8 billion in R&D and capacity investment between 2022 and 2024, largely driven by consumer demand for sustainable cosmetic emulsifiers and plant-derived food processing additives [3]. Major ingredient houses are retooling enzymatic and fermentation lines, enabling drop-in replacement of synthetic lecithin and mono-diglyceride blends with rapeseed-, sunflower-, and soy-derived alternatives.

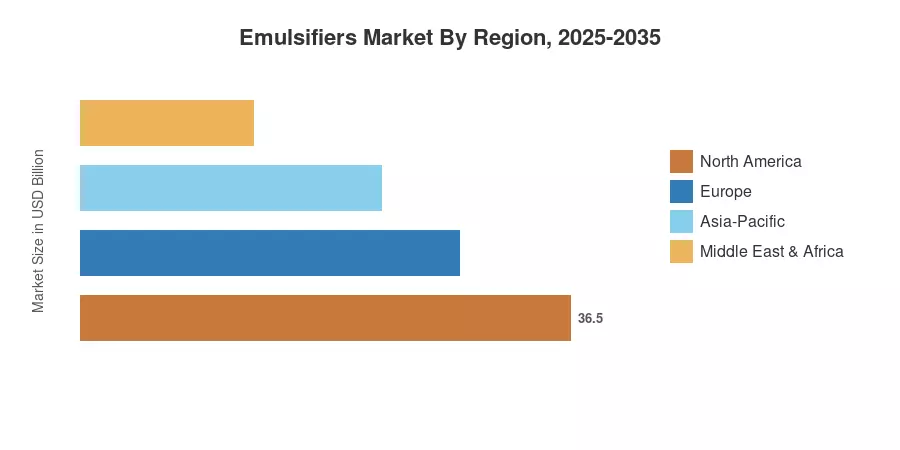

Asia-Pacific commands the largest share of the Emulsifiers Market at roughly 43% of global revenue, propelled by surging bakery ingredient additives demand in China and India. The region also holds the fastest-growing CAGR, estimated near 5.1% through 2035. North America follows as the second-largest regional contributor, accounting for approximately 23% of global value, underpinned by the US clean-label movement and expanding personal care ingredient formulations. Europe's well-established regulatory framework keeps it a close third. Looking ahead, rising urbanization across Southeast Asia and Latin America will broaden the addressable base for surfactant chemicals and specialty emulsification platforms well into the next decade.

Key Report Takeaways

• By Source

- Bio-based emulsifiers dominate the Emulsifiers Market with approximately 58% revenue share in 2025, driven by clean-label reformulation and consumer preference for plant-derived stabilizing agents.

- Synthetic emulsifiers are forecast to register a CAGR of 3.6% (2026–2035) as oilfield and agrochemical end-uses sustain baseline demand for cost-effective surfactant chemicals.

• By Application

- Food products remain the largest application segment in the Emulsifiers Market, valued at approximately USD 5.78 Billion in 2025, fueled by growth in bakery ingredient additives and dairy processing.

- Personal care and cosmetics products represent the fastest-growing application, with a projected CAGR of 5.4% as formulators integrate advanced cosmetic emulsifiers into skincare and haircare lines.

- Pharmaceuticals contribute roughly 8% of total market value, underpinned by drug-delivery innovation using formulation stabilizers.

• By Region

- Asia-Pacific leads the Emulsifiers Market with a 43% global share and the highest regional CAGR of 5.1%.

- North America holds around 23% share, with the US accounting for over 68% of regional revenue from food processing additives and personal care ingredients.

- Europe commands approximately 22% of global value, driven by stringent EU additive regulations and demand for specialty chemical emulsifiers.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s sizing methodology combines bottom-up revenue estimation from manufacturer shipments, trade-flow analysis, and top-down cross-validation against regional consumption data, import/export logs, and industry body publications[4].