Enterprise Asset Management Market Summary

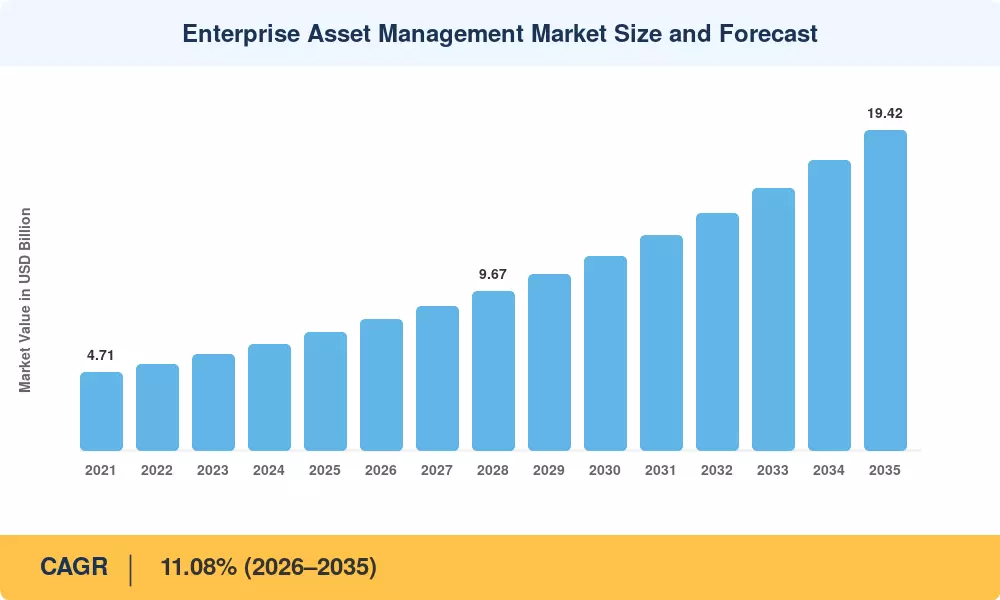

The Enterprise Asset Management Market was valued at USD 7.17 billion in 2025 and is projected to reach USD 7.91 billion in 2026 before climbing to USD 19.42 billion by 2035, registering an 11.08% CAGR during 2026–2035. Stricter ESG-linked performance mandates across the European Union and North America — alongside the U.S. Infrastructure Investment and Jobs Act channeling over USD 550 billion toward aging public works — are compelling asset-intensive industries to replace reactive maintenance with predictive work models [2]. The Enterprise Asset Management Market sits at the center of this shift, providing the software backbone for asset lifecycle management for infrastructure spanning power grids, rail networks, and manufacturing floors.

As outdated on-premise work-order systems are replaced, the technology migration to cloud-native platforms with AI-powered predictive asset maintenance and digital-twin engines is underway. Since 2022, IBM, SAP and Oracle have committed more than USD 4 billion in R&D on ERP-integrated enterprise asset management capabilities, incorporating generative AI copilots to automate failure-mode analysis and spare-parts procurement [3]. Some IoT-connected asset tracking systems are now churning millions of sensor data points each hour onto centralized dashboards, turning raw vibration, temperature and pressure readings into actionable maintenance plans and asset performance optimization with analytics.

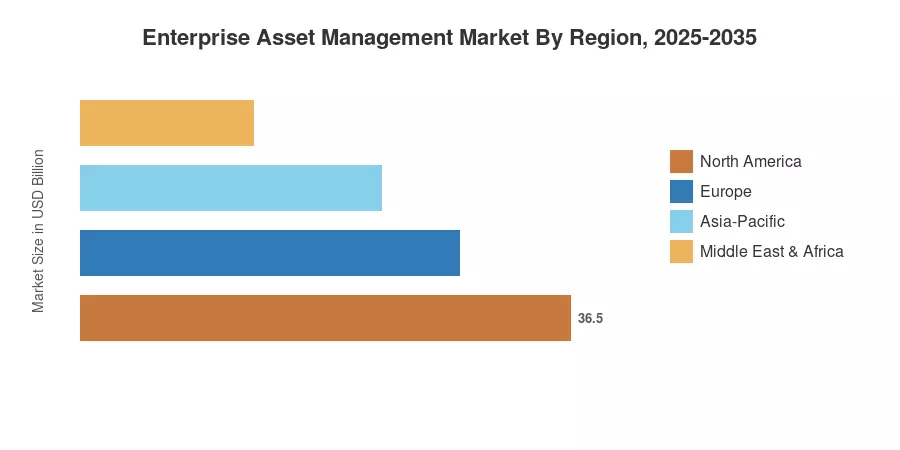

North America commands roughly 35.50% of global revenue, anchored by advanced utility grids and defense installations. Asia-Pacific is the fastest-growing region at a 12.65% CAGR, driven by China's smart-manufacturing push and India's National Infrastructure Pipeline. Europe holds the second-largest share, near 27.80%, propelled by the EU's Corporate Sustainability Reporting Directive that ties capital access to demonstrable asset reliability [4]. As workforce shortages intensify globally, the Enterprise Asset Management Market is poised for sustained double-digit expansion through 2035.

Key Report Takeaways

• By Type

- Solutions contributed approximately 69.10% of the 2025 Enterprise Asset Management Market revenue, reflecting deep penetration of platform licenses and SaaS subscriptions across heavy industries.

- The services segment is expanding at the fastest pace — a projected 14.15% CAGR to 2035 — as organizations outsource implementation, training, and managed maintenance analytics.

• By Deployment

- Cloud deployment captured a dominant share of the Enterprise Asset Management Market in 2025 and continues to grow at a 14.05% CAGR, fueled by lower capital outlays and faster analytics rollouts.

- On-premises and hybrid models retain relevance in defense and critical infrastructure, where data sovereignty is non-negotiable.

• By End-User Industry

- Manufacturing led all verticals with USD 1.83 billion in 2025 revenue, relying on IoT-connected asset tracking systems for shop-floor uptime.

- Healthcare is poised for the strongest vertical CAGR at 16.20% through 2035, driven by biomedical equipment compliance mandates and asset lifecycle management for infrastructure in hospital networks.

• By Region

- North America remains the dominant region, supported by federal infrastructure spending and mature ERP-integrated enterprise asset management deployments.

- Asia-Pacific leads to growth with a 12.65% CAGR, while Europe maintains the second-largest share.

• Enterprise Asset Management Market Size and Forecast (2021–2035)

Our market-sizing methodology triangulates top-down macroeconomic data (IT spend as a share of GDP), bottom-up vendor revenue disclosures, and primary interviews with 120+ procurement leaders in manufacturing, energy, and transportation. Historical data (2021–2024) are based on actuals, 2025 is the validated base year, and 2026–2035 values use the calibrated 11.08% CAGR with modifications for known investment cycles.]