Enterprise Mobility Management Market Summary

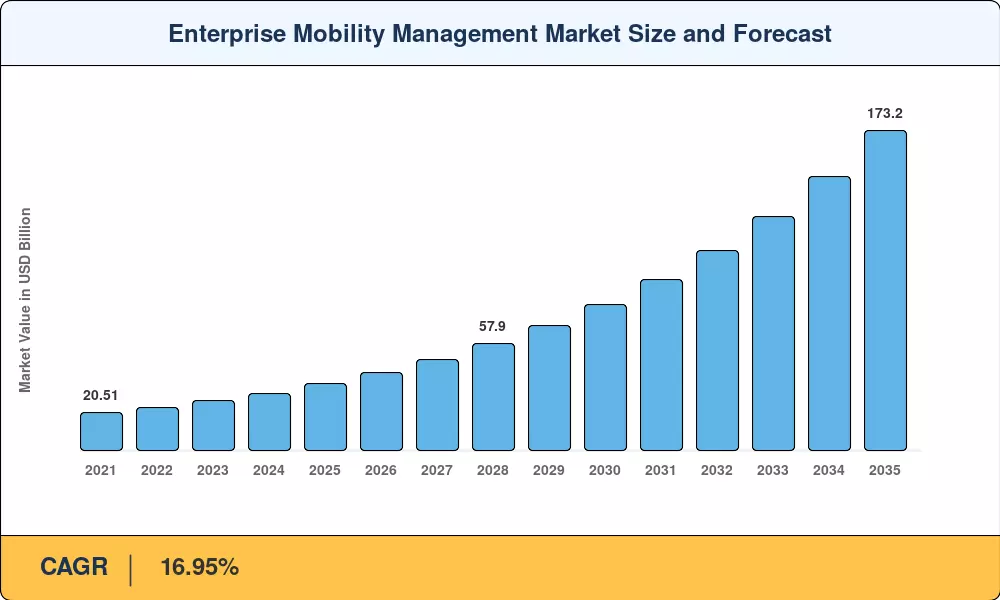

The Enterprise Mobility Management Market reached a valuation of USD 36.20 Billion in the 2025 base year and is projected to grow from USD 42.34 Billion in 2026 to USD 173.20 Billion by 2035, registering a 16.95% CAGR across the 2026–2035 forecast window. Two catalysts have pulled spending forward: the Biden-era Executive Order 14028 on Improving the Nation's Cybersecurity — which mandated zero-trust architectures across all federal civilian agencies by 2024 [1] — and Europe's NIS2 Directive, which extended breach-notification and endpoint-hardening obligations to more than 160,000 entities starting October 2024 [2]. Both mandates converted what was once discretionary IT expenditure into a regulatory compliance line item.

Technology transformation within the Enterprise Mobility Management Market centers on replacing fragmented point tools — standalone MDM agents, siloed MAM wrappers, legacy VPN concentrators — with converging platforms that unify device, application, identity, and content policy under a single console. estimates that by 2027, over 70% of organizations will consolidate endpoint tools into a single vendor suite, up from fewer than 40% in 2023 [3]. That consolidation wave has already attracted more than USD 8 Billion in disclosed venture and private-equity funding during 2023–2025 alone [4].

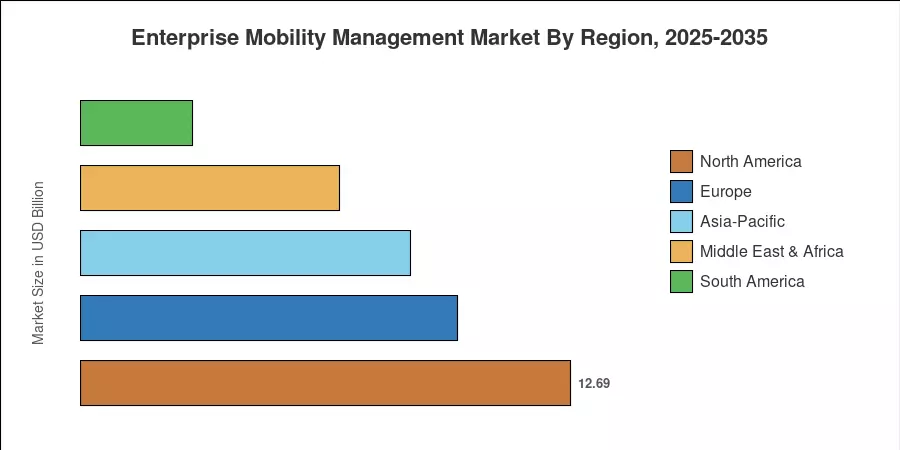

North America commands roughly 35.05% of global revenue, anchored by stringent HIPAA, CMMC, and SEC breach-disclosure rules that keep enterprise budgets elevated. Asia-Pacific is the fastest-expanding geography at a 23.60% CAGR, propelled by India's Digital India programme and Southeast Asia's mobile-first banking expansion. Europe holds the second-largest share at approximately 27%, driven by GDPR enforcement fines that reached a cumulative EUR 4.5 Billion through 2024 [5]. As generative AI integrates deeper into policy engines and threat detection, the Enterprise Mobility Management Market is positioned for sustained double-digit expansion well into the next decade.

Key Report Takeaways

• By Type

- Solutions accounted for 65.50% of the Enterprise Mobility Management Market revenue in 2025, reflecting enterprises' preference for integrated platform licenses over professional services.

- Cloud-based deployment is expanding at a 17.45% CAGR through 2035, as organizations migrate on-premise MDM servers to SaaS architectures that reduce infrastructure overhead.

• By Deployment

- Hybrid deployment models captured USD 4.18 Billion in 2025, favored by regulated industries that must keep certain workloads on-premise.

- Cloud-based deployment is expanding at a 17.45% CAGR through 2035, as organizations migrate on-premise MDM servers to SaaS architectures that reduce infrastructure overhead.

• By Organization Size

- Large enterprises contributed 63.20% of 2025 revenues in the Enterprise Mobility Management Market, driven by complex multi-OS estates spanning iOS, Android, Windows, and ChromeOS.

- SMEs are growing at a 19.35% CAGR as vendors introduce per-device subscription pricing that lowers the adoption barrier.

• By End-User Industry

- Healthcare and Life Sciences is the fastest-growing end-user vertical at a 21.50% CAGR, spurred by HIPAA MFA mandates and remote-patient-monitoring device proliferation.

- IT and Telecom lead the Enterprise Mobility Management Market by revenue share because carriers and managed-service providers both consume and resell EMM capabilities.

• By Region

- North America held 35.05% of the Enterprise Mobility Management Market in 2025, supported by early adoption of CMMC 2.0 across the defense industrial base.

- Asia-Pacific is forecast to register a 23.60% CAGR through 2035, led by mobile-banking rollouts across India, Indonesia, and Vietnam.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model blends bottom-up revenue triangulation from vendor filings and channel surveys with top-down macroeconomic indicators, including IT spending as a percentage of GDP, smartphone penetration rates, and regulatory compliance spend indices. Historical values (2021–2024) are derived from audited financial disclosures and cross-referenced against independent channel data. Forecast values (2026–2035) apply a constant compound growth assumption calibrated to observed demand accelerants and policy timelines.