Certified Global Research Member

Key Questions Answered

- Global Market Outlook

- In-depth analysis of global and regional trends

- Analyze and identify the major players in the market, their market share, key developments, etc.

- To understand the capability of the major players based on products offered, financials, and strategies.

- Identify disrupting products, companies, and trends.

- To identify opportunities in the market.

- Analyze the key challenges in the market.

- Analyze the regional penetration of players, products, and services in the market.

- Comparison of major players’ financial performance.

- Evaluate strategies adopted by major players.

- Recommendations

Why Choose Market Research Future?

- Vigorous research methodologies for specific market.

- Knowledge partners across the globe

- Large network of partner consultants.

- Ever-increasing/ Escalating data base with quarterly monitoring of various markets

- Trusted by fortune 500 companies/startups/ universities/organizations

- Large database of 5000+ markets reports.

- Effective and prompt pre- and post-sales support.

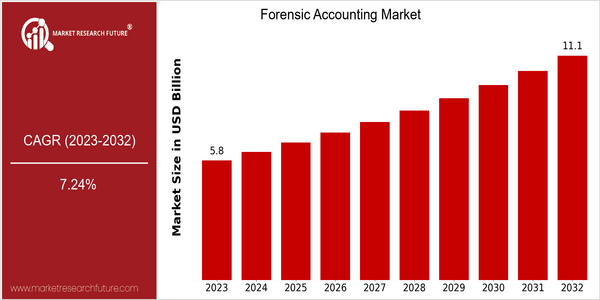

Market Size Snapshot

| Year | Value |

|---|---|

| 2023 | USD 5.84 Billion |

| 2032 | USD 11.06 Billion |

| CAGR (2024-2032) | 7.24 % |

Note – Market size depicts the revenue generated over the financial year

The forensic accounting market is estimated to reach $ 5.84 billion in 2023, and to reach $ 11.06 billion in 2032, with a CAGR of 7.24% from 2024 to 2032. The forensic accounting market is a very high growth market. The main reasons for this growth are the increasing complexity of financial fraud, the need for regulatory compliance, and the need for transparency in various industries. The role of forensic accountants in investigating financial irregularities and ensuring compliance with the law is more important than ever. This growth is mainly due to technological innovations, such as data analytics, artificial intelligence, and blockchain, which are transforming the accounting profession. These new technological tools enable forensic accountants to perform more accurate and thorough investigations and gain deeper insights into financial data. In this market, the main players are Deloitte, PwC, KPMG, etc., which are investing heavily in technological innovations and forming strategic alliances. For example, recent collaborations between technology companies and major accounting companies aim to integrate advanced data analytics into forensic accounting services to improve the efficiency and accuracy of forensic accounting. Strategic alliances like this will further drive the growth of the forensic accounting market in the coming years.

Regional Market Size

Regional Deep Dive

The forensic accounting market is growing in various regions, driven by an increase in fraud and a growing need for financial transparency. In North America, the forensic accounting market is characterized by high demand for forensic accounting services, mainly due to strict regulations and a strong legal framework. In Europe, there is a varied regulatory framework, while in Asia-Pacific, forensic accounting is rapidly becoming a part of the everyday life of the population, as economies develop and financial crimes increase. In the Middle East and Africa, forensic accounting is gaining ground, especially in the oil and gas sector. In Latin America, forensic accounting is increasingly used to enhance financial integrity.

Europe

- The European Union's Anti-Money Laundering (AML) directives have prompted a surge in forensic accounting services, as organizations seek to comply with stricter regulations and avoid hefty fines.

- Notable developments include the establishment of the European Financial Reporting Advisory Group (EFRAG), which aims to enhance transparency and accountability in financial reporting, thereby increasing the demand for forensic accounting expertise.

Asia Pacific

- Countries like India and China are witnessing a growing trend in forensic accounting due to the rapid increase in financial crimes, leading to the establishment of specialized forensic accounting firms such as KPMG and EY.

- The introduction of the Insolvency and Bankruptcy Code in India has created a need for forensic accountants to investigate financial irregularities in distressed companies, further driving market growth.

Latin America

- Brazil's recent anti-corruption laws have spurred the growth of forensic accounting services, as companies seek to ensure compliance and mitigate risks associated with financial misconduct.

- The rise of digital currencies in Latin America has led to an increased focus on forensic accounting to address the unique challenges posed by cryptocurrency transactions and related fraud.

North America

- The rise in cybercrime has led to an increased demand for forensic accountants who specialize in digital fraud investigations, with firms like Deloitte and PwC expanding their forensic services to address this trend.

- Regulatory changes, such as the implementation of the Sarbanes-Oxley Act, continue to shape the forensic accounting landscape, compelling companies to adopt more rigorous financial reporting and auditing practices.

Middle East And Africa

- The UAE has launched initiatives to combat financial fraud, such as the Dubai Financial Services Authority's (DFSA) regulations, which have increased the demand for forensic accounting services in the region.

- In South Africa, the establishment of the Financial Sector Conduct Authority (FSCA) has led to a greater emphasis on compliance and risk management, prompting organizations to invest in forensic accounting capabilities.

Did You Know?

“Approximately 70% of organizations worldwide have reported experiencing some form of financial fraud, highlighting the critical role of forensic accounting in mitigating such risks.” — Association of Certified Fraud Examiners (ACFE)

Segmental Market Size

The forensic accounting market is experiencing steady growth, as the demand for fraud prevention and detection services rises. In particular, the complexity of financial crimes and the increasing regulatory pressure are driving the growth of the forensic accounting market. As the organizations are more aware of the risks of fraud, the need for forensic accounting services to investigate and resolve the financial reporting discrepancies is also growing. However, forensic accounting is now in a mature stage. Deloitte and PwC are the leading forensic accounting service providers, specializing in fraud investigations across various industries. The major applications of forensic accounting include litigation support, fraud investigation, and compliance audits, especially in the banking, insurance, and healthcare industries. These applications are expected to grow in line with the digital transformation of the financial services industry and the growing cybercrime trend. The new forensic accounting technology, such as data analytics and artificial intelligence, is expected to help the industry perform more accurate and efficient investigations.

Future Outlook

Forensic accounting is a growing market. From 2023 to 2032, the forensic accounting market is expected to reach $11.06 billion, with a CAGR of 7.24% from 2023 to 2032. This growth is driven by the increasing demand for fraud prevention and detection services in all sectors, including finance, health and government. Because of the increased pressure of public scrutiny and regulation, forensic accounting will become more and more important in identifying financial irregularities and ensuring compliance. The penetration of forensic accounting services is expected to reach about one-quarter of all accounting services in 2032, compared with about one-fifth in 2023, which shows that forensic accounting services have become a new tool for safeguarding assets and maintaining the integrity of enterprises. Artificial intelligence and data analysis have been developed. They are expected to be a major revolution in the field of forensic accounting. The use of these two technologies will improve the efficiency and accuracy of forensic accounting, and they will be able to quickly analyze large amounts of data and find the abnormality. In addition, with the rise of cybercrime, the complexity of financial transactions will also increase the demand for forensic accounting services. The role of forensic accounting will become more and more important as the regulatory environment changes. The market will continue to grow and develop.

Covered Aspects:| Report Attribute/Metric | Details |

|---|---|

| Market Size Value In 2023 | USD 5.84 Billion |

| Growth Rate | 7.24% (2024-2032) |

Forensic Accounting Market Highlights:

Leading companies partner with us for data-driven Insights

Kindly complete the form below to receive a free sample of this Report

Tailored for You

- Dedicated Research on any specifics segment or region.

- Focused Research on specific players in the market.

- Custom Report based only on your requirements.

- Flexibility to add or subtract any chapter in the study.

- Historic data from 2014 and forecasts outlook till 2040.

- Flexibility of providing data/insights in formats (PDF, PPT, Excel).

- Provide cross segmentation in applicable scenario/markets.