Identity Verification Market Summary

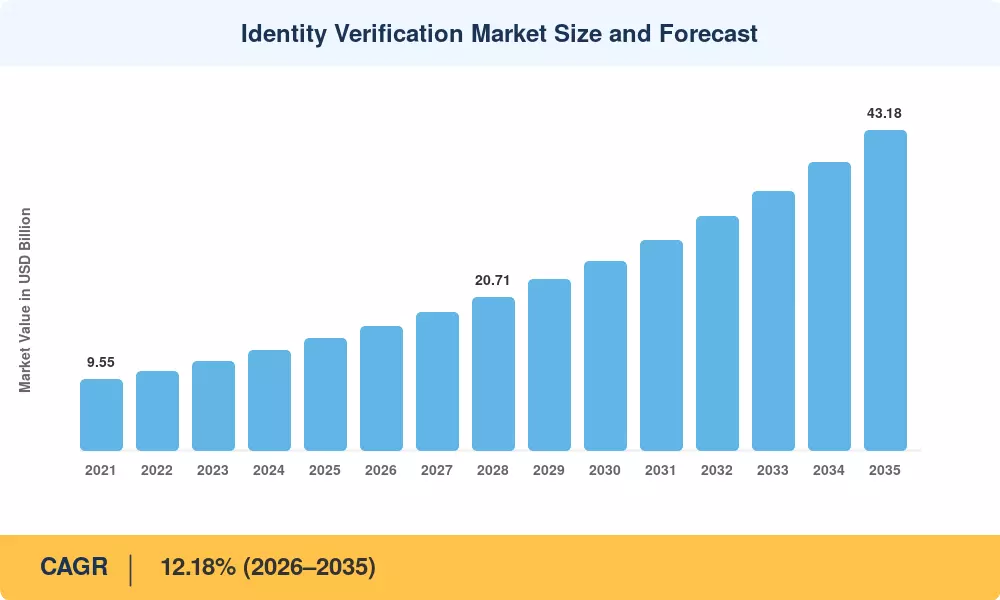

The Identity Verification Market reached an estimated USD 15.12 billion in 2025 and is projected to grow from USD 16.89 Billion in 2026 to USD 43.18 billion by 2035, registering a CAGR of 12.18% during the forecast period (2026–2035). This expansion is anchored in tightening global anti-money laundering mandates — the EU's Anti-Money Laundering Authority (AMLA), launched in 2024, now enforces direct supervisory powers over high-risk obliged entities across 27 member states [2]. Enterprises that once treated identity checks as a compliance checkbox are now channeling strategic budgets into digital ID authentication platforms capable of intercepting AI-generated fraud in real time.

A significant technological transformation is currently in progress. AI-orchestrated pipelines are replacing legacy manual review queues and rules-based document verification software. These pipelines combine optical character recognition, passive liveness detection, and behavioral biometrics into a single API call. In 2024, the global expenditure on biometric identity checks infrastructure surpassed USD 4.8 billion, primarily due to the financial institutions' urgency to comply with the Financial Action Task Force's revised Recommendation 10 on customer due diligence [3]. Vendors are now able to support online identity proofing at scale across jurisdictions and push model updates instantaneously, as cloud-native deployment now dominates new rollouts.

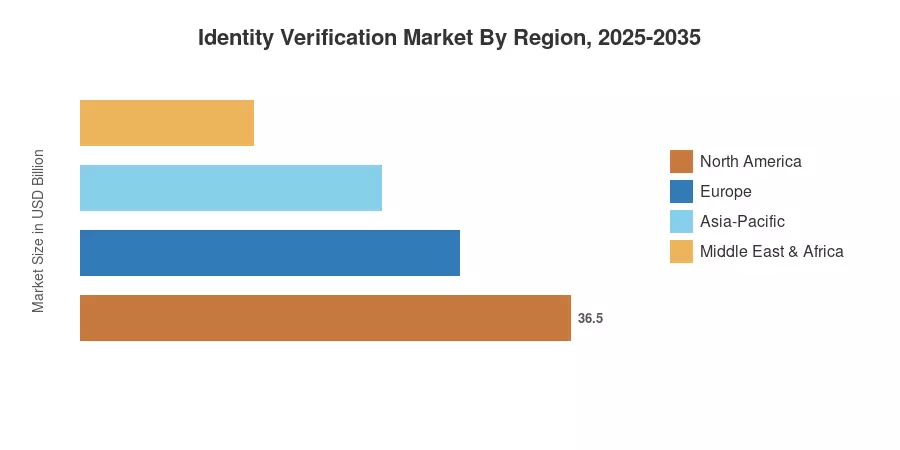

North America accounts for approximately 34% of the Identity Verification Market, which is supported by the pervasive adoption of KYC verification solutions across banking and fintech, as well as the stringent FinCEN beneficial-ownership rules The Aadhaar-linked eKYC ecosystem in India and the expanding social credit frameworks in China are the driving forces behind the quickest growth in the Asia-Pacific region, which is achieving a 12.56% CAGR. The eIDAS 2.0 regulation has established a unified digital identity wallet framework for 450 million citizens, resulting in Europe holding the second-largest proportion at approximately 27%. As portable credential architectures mature and deepfake threats intensify, the Identity Verification Market is on the brink of sustained double-digit growth.

Key Report Takeaways

• By Deployment Model

- Cloud platforms captured a 69.4% share of the Identity Verification Market in 2025, reflecting enterprises' preference for scalable, API-first digital ID authentication architectures

- On-premises deployments are projected to grow at an 8.9% CAGR through 2035, sustained by defense and government agencies with air-gapped security requirements

• By Solution Type

- Biometric verification led all solution categories with USD 5.56 billion in 2025 revenue, driven by passive liveness and behavioral analytics adoption

- Document-centric identity verification, including document verification software with AI forensics, is advancing at the fastest CAGR of 14.08% through 2035

• By End-User Industry

- Financial services retained a 32.8% share of the Identity Verification Market in 2025, underscoring banking's role as the primary buyer of KYC verification solutions

- Gaming and gambling are advancing at a 12.26% CAGR, as regulators mandate age and identity checks for online wagering platforms

• By Organization Size

- Large enterprises commanded 77.2% of identity verification spending in 2025

- SMEs record the fastest CAGR at 13.32%, fueled by affordable SaaS-based online identity proofing tools

• By Regional

- North America accounted for USD 5.14 billion in 2025, anchored by US regulatory enforcement

- Asia-Pacific posts the highest regional growth at 12.56% CAGR, driven by digital ID authentication mandates across India, China, and ASEAN economies

Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework triangulates vendor revenues, regulatory filings, and enterprise procurement surveys to construct bottom-up market sizing. Historical figures (2021–2024) are validated against annual reports and industry association data, while forecast values (2026–2035) apply the calibrated 12.18% CAGR with adjustments for anticipated regulatory catalysts and technology adoption curves.