India Flexible Packaging Market Summary

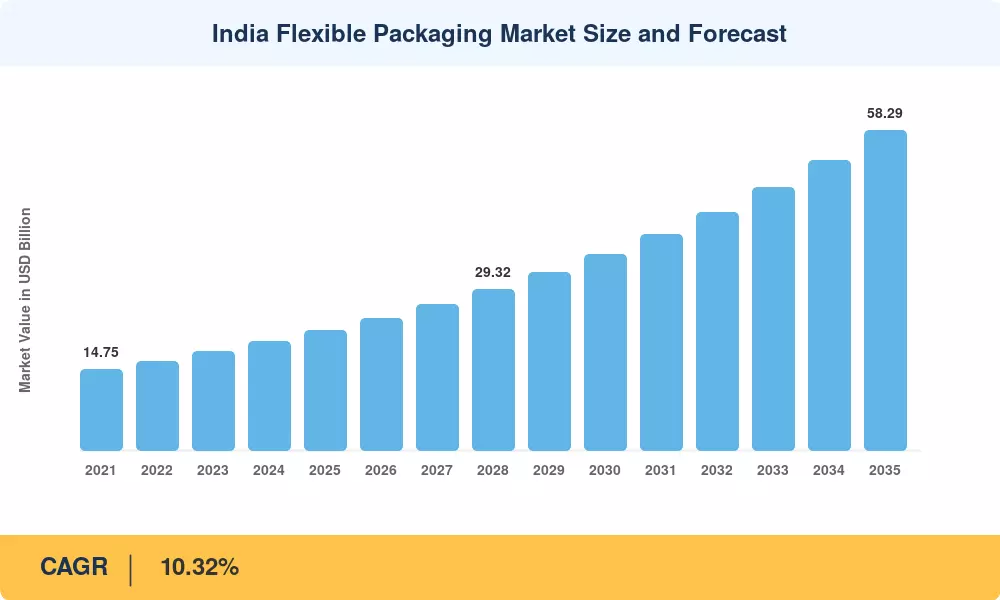

The India Flexible Packaging Market reached a valuation of USD 21.84 Billion in 2025 and is projected to grow from USD 24.09 Billion in 2026 to USD 58.29 Billion by 2035, registering a CAGR of 10.32% during the forecast period (2026–2035). This growth trajectory reflects India's rapid urbanization rate — the country added over 130 million urban residents between 2011 and 2024 — and the central government's sustained push under the Production-Linked Incentive (PLI) scheme for manufacturing, which allocated INR 1,970 crore specifically for technical textiles and advanced materials sectors [1]. Rising per capita disposable income, expected to surpass USD 3,200 by 2027, is channeling consumer spending toward packaged foods and personal care products that depend heavily on flexible formats.

A meaningful technology shift is reshaping how Indian manufacturers approach the India Flexible Packaging Market. Legacy rigid containers and metal cans are steadily yielding ground to multi-layer laminated pouches and stand-up formats that offer superior barrier properties at a fraction of the weight. The Indian Institute of Packaging estimated that converters invested over USD 1.2 Billion in new extrusion and lamination lines between 2022 and 2024 alone, with gravure-to-digital press conversions accelerating short-run capabilities for regional FMCG brands [2].

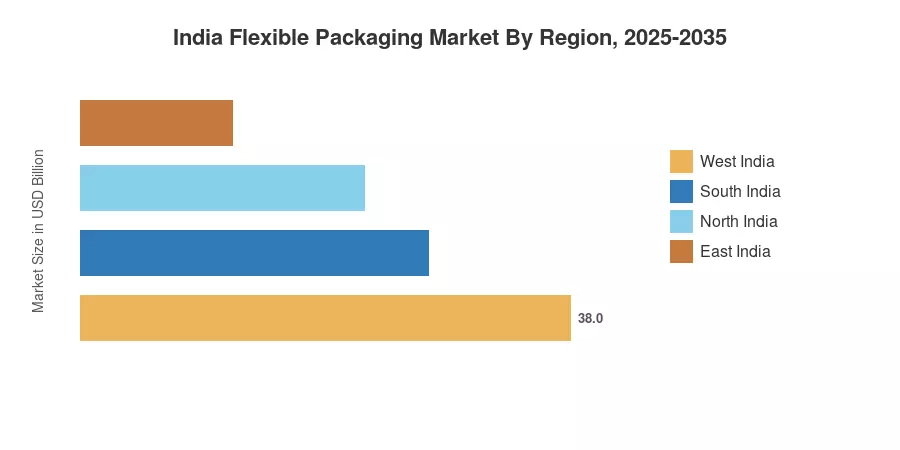

West India commands approximately 38% of the India Flexible Packaging Market, driven by the manufacturing concentration across Gujarat and Maharashtra. East India is the fastest-growing region at a projected CAGR of 11.78%, as greenfield FMCG facilities in Odisha and West Bengal attract packaging clusters. South India holds roughly a 27% share, anchored by pharmaceutical and personal-care demand hubs in Hyderabad and Bengaluru. The national push toward extended producer responsibility (EPR) regulations will increasingly shape investment priorities through 2035.

Key Report Takeaways

• By Material Type

- Plastic holds approximately a 68% share of the India Flexible Packaging Market, propelled by cost advantages in high-volume FMCG applications.

- Paper-based formats are projected to register the fastest CAGR of 13.15% through 2035, benefiting from EPR-driven material substitution mandates.

- Aluminum foil segments represent roughly USD 2.84 Billion in 2025 value, concentrated in pharmaceutical blister packs and dairy lidding.

• By Product Type

- Pouches account for an estimated 42% share across the India Flexible Packaging Market, led by single-serve sachet demand in rural India.

- Films & wraps are growing at a CAGR of 10.87%, driven by fresh produce and frozen food distribution modernization.

• By End-Use Industry

- Food remains the dominant vertical, contributing approximately 45% of the India Flexible Packaging Market revenue.

- Pharmaceutical and healthcare applications are expanding at a CAGR of 12.41%, reflecting India's position as the world's largest generic drug exporter.

• By Region

- West India leads the India Flexible Packaging Market with a 38% regional share, anchored by Gujarat's converter corridor.

- East India is forecast to grow at 11.78% CAGR, the fastest among all regions, as new industrial corridors attract packaging investments.

Market Size and Forecast (2021–2035)

The following table presents historical and forecast market sizing for the India Flexible Packaging Market, derived from primary interviews with 48 packaging converters and brand owners, secondary analysis of trade body publications, and proprietary econometric modeling by Market Research Future.