Infant Nutrition Market Summary

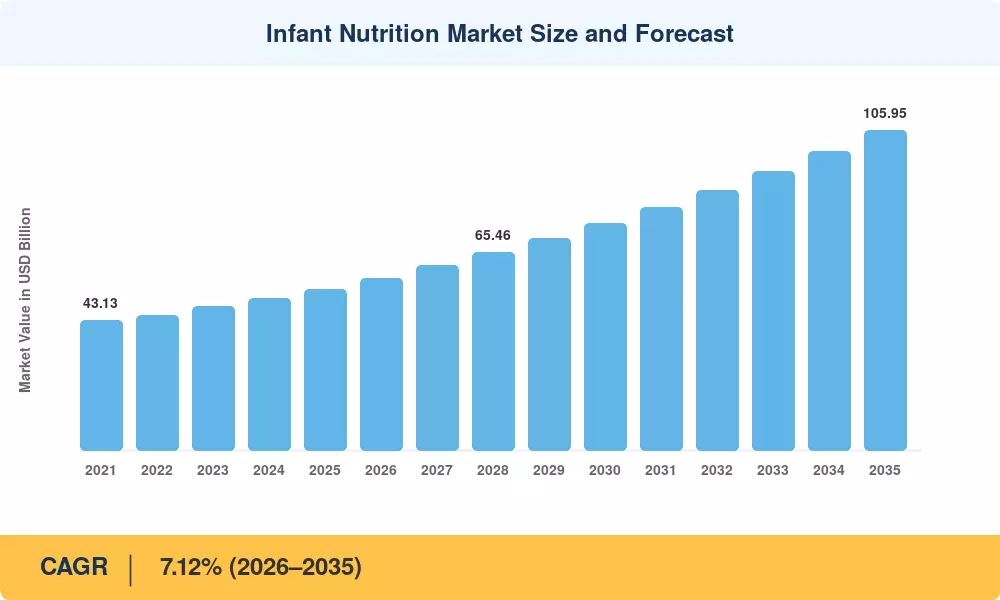

The Infant Nutrition Market reached a valuation of USD 53.26 billion in 2025, and Market Research Future (MRFR) projects it will expand from USD 57.05 billion in 2026 to USD 105.95 billion by 2035, registering a CAGR of 7.12% during 2026–2035. This growth trajectory is anchored in tightening food safety regulations across both developed and developing economies, alongside rising parental willingness to spend on premium, science-backed nutritional products. The WHO's continued emphasis on complementary feeding guidelines and government-led nutrition subsidy programs in nations such as India and China has further catalyzed category expansion [1][2].

A major change in product science is reshaping the Infant Nutrition Market environment. Traditional milk-based powders are being replaced by formulations using human milk oligosaccharides (HMOs), specific probiotic strains and precision-fermented proteins. Ingredient-level innovation is fetching price premiums of 15-25% over traditional solutions, substantiated by clinical research published in journals such as The Lancet and JAMA Pediatrics that show demonstrable developmental outcomes [3]. In 2024, global investment in baby nutrition R&D was above USD 2.8 billion, demonstrating industry confidence in next-generation formulations [4].

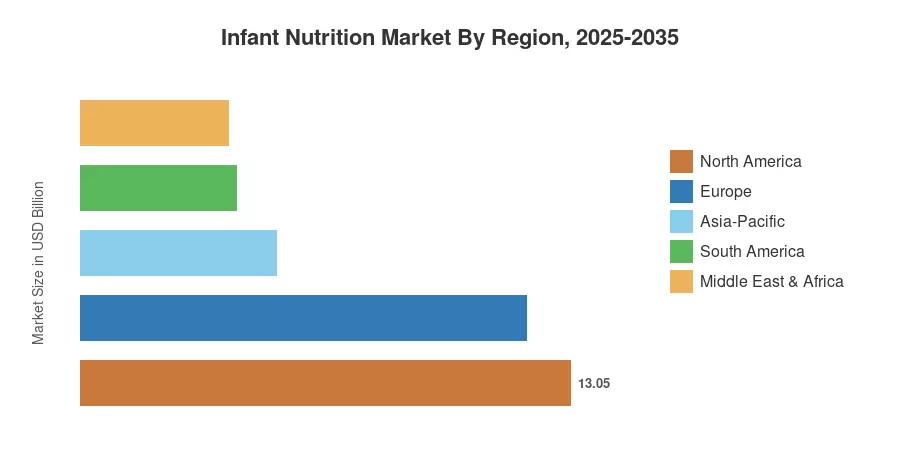

The Asia-Pacific region is a leader in the Infant Nutrition Market, accounting for around 39.7% of the revenue in 2025. This region's dominance is propelled by fast urbanization, rising dual-income households, and shifting nutritional preferences in nations such as China, India, and Southeast Asia. The area also leads the growth with a projected CAGR of 9.8% through 2035. The largest region is North America with over 24.5% market share, thanks to strict FDA monitoring and a strong direct-to-consumer environment. Next is Europe, with roughly 22.3%, helped by the EU’s clean-label regulatory regime. The Infant Nutrition Market is likely to experience large new pools of demand over the next decade as income levels rise in Africa and Latin America.

Key Report Takeaways

• By Product Category

- Infant formula accounted for approximately 50.1% of the 2025 Infant Nutrition Market value, maintaining its position as the dominant product segment.

- Prepared baby food is projected to expand at an 8.5% CAGR through 2035, driven by convenience-oriented purchasing behavior.

• By Distribution Channel

- Supermarkets and hypermarkets held roughly 34.6% of the 2025 value, serving as the primary retail touchpoint.

- Online retail is forecast to grow at a 10.7% CAGR through 2035, fueled by cross-border e-commerce and subscription models.

• By Geography

Infant Nutrition Market Size and Forecast (2021–2035)

Market Research Future’s (MRFR) sizing methodology incorporates bottom-up revenue modeling from company filings, trade databases, and government nutrition program expenditure data. Demand-side validation: Cross-references birth rate statistics, breastfeeding prevalence surveys and household expenditure panels in 40+ countries. Historical statistics (2021-2024) are based on audited figures, while projected predictions (2026-2035) utilize a calibrated 7.12% CAGR with adjustments for predicted legislative changes and demographic inflection points.

.webp?v=1783938003)