Interactive Kiosk Market Summary

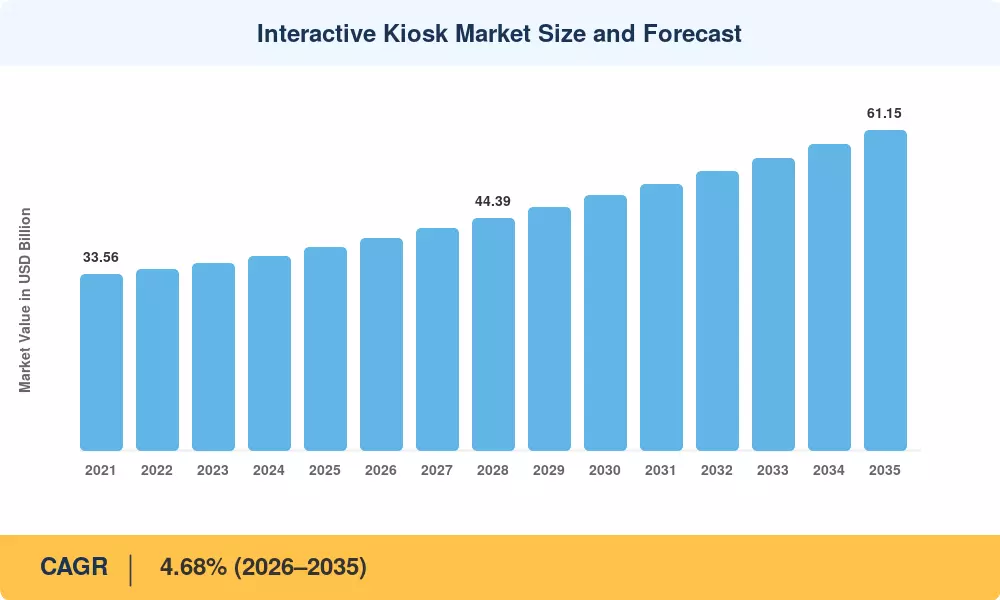

The Interactive Kiosk Market reached USD 38.70 billion in 2025 and is projected to grow from USD 40.51 billion in 2026 to USD 61.15 billion by 2035, registering a CAGR of 4.68% during the forecast period (2026–2035). Two catalysts anchor this trajectory: a post-pandemic shift toward contactless self-service infrastructure and aggressive government digitization mandates — the European Commission's Digital Decade program alone channels EUR 7.5 billion toward citizen-facing digital service points by 2030 [1]. Retail chains, airports, and municipal service centers are replacing staffed counters with intelligent terminals at a pace not seen in the previous decade.

The technology transition of the Interactive Kiosk Market is the shift away from old resistive-touch, single-function hardware to modular, cloud-connected platforms driven by energy-efficient ARM processors. Multi-service capabilities such as bill payment, identity verification and telehealth intake are adding to the industry’s backbone of traditional ATM deployments. It is predicted that U.S. banking institutions invested USD 2.1 billion in next-generation branch automation alone in 2024, indicating that hardware refresh cycles are getting shorter [2].

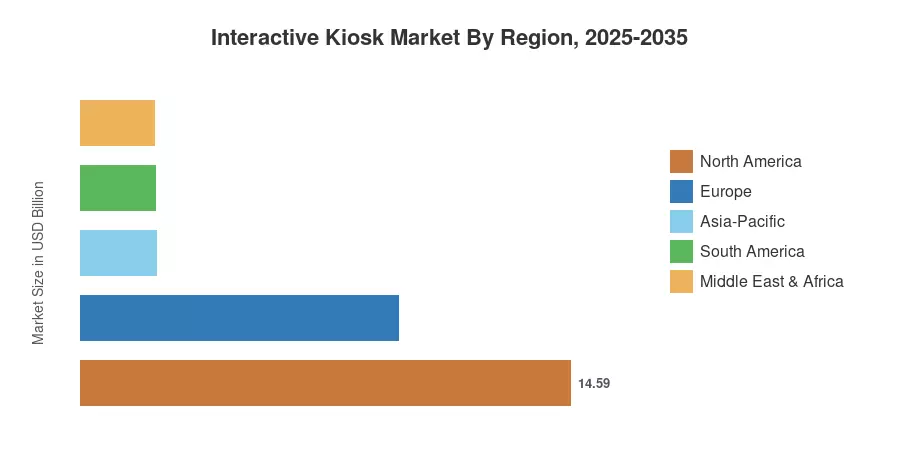

North America held the highest share of 37.70% of the Interactive Kiosk Market in 2025 due to the developed retail and BFSI ecosystems. Asia-Pacific is the fastest-growing market with a CAGR of 5.86%, driven by the smart-city projects in China, India, and ASEAN countries. The second largest is Europe, with around 24.50%, where the transit authority modernization and healthcare digitization are driving uptake. Over the next decade, emerging markets in the Middle East and South America will scale digital governance programs, closing the deployment gap.

Key Report Takeaways

• By Type

- ATM kiosks captured 34.10% of the Interactive Kiosk Market in 2025, reflecting sustained demand from banking branch transformation programs.

- Ticketing kiosks are forecast to grow at a 5.58% CAGR through 2035, propelled by transit modernization and live-event venue upgrades.

• By Component

- Hardware accounted for 59.40% of the Interactive Kiosk Market in 2025, though the software-and-services mix is gaining ground rapidly.

- Managed services are advancing at a 4.88% CAGR as fleet operators shift from CAPEX to OPEX models.

• By Geography

- North America led the Interactive Kiosk Market with 37.70% revenue share, anchored by the United States' retail and financial sectors.

- Asia-Pacific is on track for a 5.86% CAGR, with China and India accounting for the bulk of new installations.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) applies a sizing technique that includes bottom-up tracking of hardware shipments, analysis of software licensing revenues, and data from managed-service contracts for 42 nations. Historical figures (2021-2024) are derived from verified corporate filings and customs-trade databases. Forecast estimations (2026-2035) are derived from scenario-weighted CAGR modeling, cross-verified with macroeconomic data and regional deployment pipelines.