Micro Inverter Market Summary

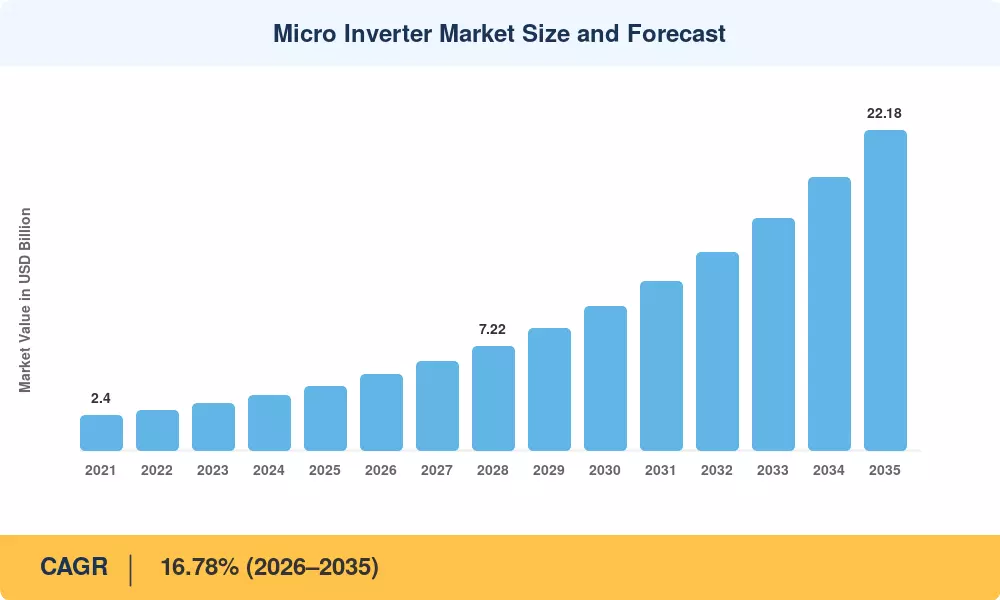

The Micro Inverter Market reached an estimated USD 4.46 billion in 2025 and is projected to grow from USD 5.27 billion in 2026 to USD 22.18 billion by 2035, registering a CAGR of 16.78% across the forecast window. This expansion is anchored in two powerful policy catalysts: the United States' Inflation Reduction Act, which allocates over USD 60 billion in clean energy tax credits through the early 2030s, and the European Union's revised Energy Performance of Buildings Directive mandating rooftop solar readiness on all new residential construction by 2030 [2]. Panel-level power conversion is no longer a premium option — it is becoming the default specification for code-compliant installations in major economies.

A decisive technology shift is underway as solar micro inverter systems replace legacy string inverter architectures across residential and light-commercial rooftops. Vendors are migrating power stages to silicon-carbide (SiC) and gallium-nitride (GaN) switching topologies that push peak efficiency past 97% while trimming unit weight by nearly a third [3]. Factory-integrated "AC modules" — where MLPE micro inverter technology ships pre-bonded to high-wattage bifacial panels — accounted for roughly 18% of North American residential shipments in 2024, up from just 9% two years earlier. These plug-and-produce assemblies cut installation labor by 25–40 minutes per panel, a saving that resonates with cost-pressured installers.

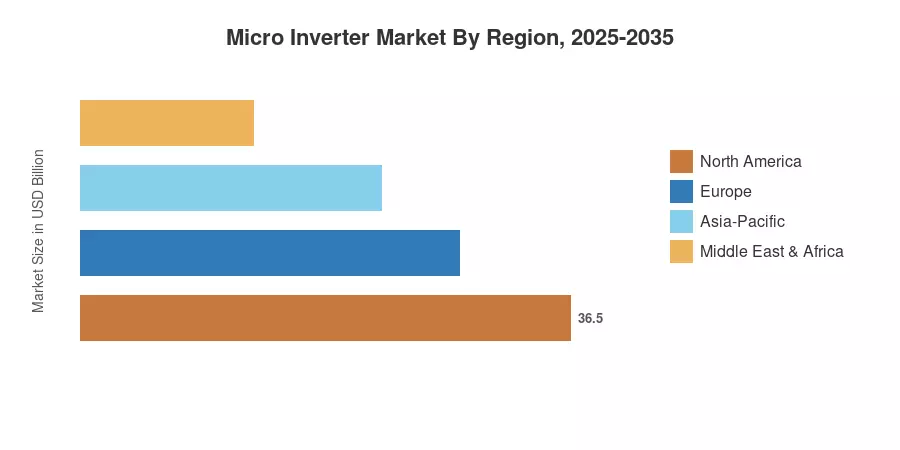

North America retained the dominant position within the Micro Inverter Market in 2025, commanding approximately 34% of global revenue thanks to NEC 690.12 rapid-shutdown enforcement and robust residential solar inverters demand Asia-Pacific emerged as the fastest-growing region, propelled by India's PM Surya Ghar program and China's distributed-generation subsidies, while Europe secured the second-largest share at around 28%, driven by simplified plug-in solar rules encouraging sub-1 kW balcony kits. The decade ahead will reward suppliers who pair grid-tied micro inverters with battery-coupling firmware and intelligent monitoring platforms.

Key Report Takeaways

• By Phase Type

- Single-phase units claimed the majority revenue share of the Micro Inverter Market in 2025, reflecting heavy residential solar inverters adoption in North America and Europe

- Three-phase models are forecast to post a 17.2% CAGR through 2035 as commercial rooftops and utility-fringe sites increasingly require balanced grid-support functions

• By Communication Technology

- Wired communication solutions held roughly 55% share in 2025, though wireless protocols are expanding at the fastest pace as installers demand simplified commissioning for panel-level power conversion

• By Component

- Hardware accounted for approximately 67% of the Micro Inverter Market in 2025, though software-and-services revenue is accelerating on the strength of monitoring subscriptions and predictive-maintenance platforms

• By Sales Channel

- Indirect distribution channels — including specialized solar distributors and certified installers — handled the majority of transactions, yet direct OEM and online routes are gaining share as MLPE micro inverter technology becomes more consumer-accessible

• By Region

- North America led the Micro Inverter Market with roughly 34% regional share in 2025, underpinned by rapid-shutdown mandates and IRA incentives

- Asia-Pacific is poised to record the highest regional CAGR through 2035, with India and China together adding more distributed PV capacity than any other region

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s sizing model combines bottom-up shipment tracking across 28 countries with top-down cross-validation against import/export databases, company filings, and third-party benchmarks[5]. Historical figures reflect actual trade data; forecast values apply the calibrated 16.78% CAGR with year-specific adjustments for policy phase-ins and supply-chain events.