Pasta Market Summary

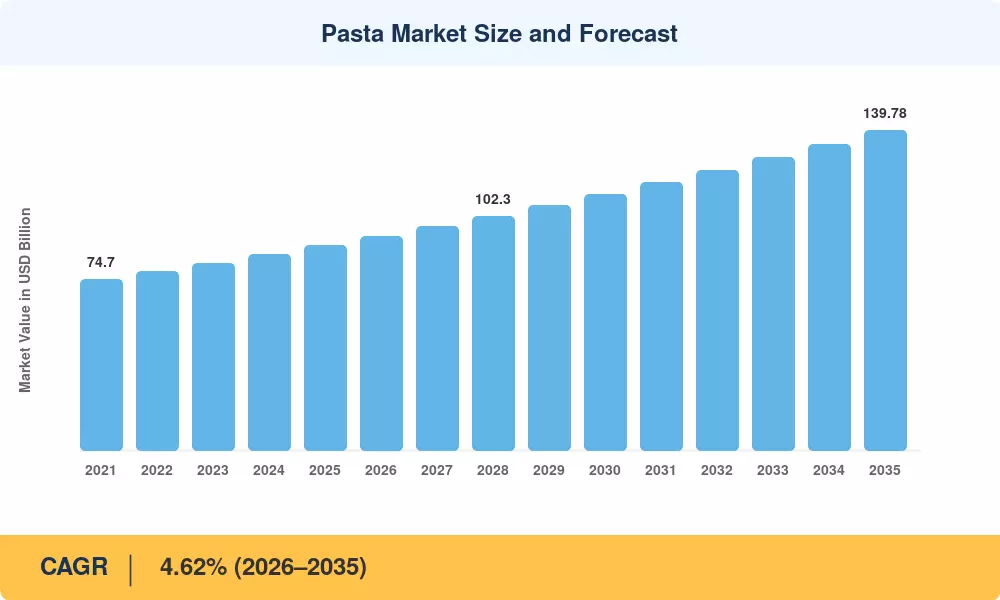

The Pasta Market was valued at USD 89.49 Billion in 2025 and is projected to reach USD 93.38 Billion by 2026, climbing to USD 139.78 Billion by 2035 at a CAGR of 4.62% during the forecast period (2026–2035). Rising consumer appetite for convenient meal solutions and the growing emphasis on health-conscious eating habits are primary catalysts shaping the Pasta Market trajectory. Governments across Europe and North America have reinforced food safety standards and nutritional labeling mandates, channeling investment into modernized pasta manufacturing process infrastructure — the European Commission's Farm to Fork Strategy alone earmarked over EUR 1.8 Billion for sustainable food production improvements through 2030 [2].

A transformation is underway in how durum wheat semolina pasta reaches consumers. Legacy batch-processing facilities are giving way to automated, continuous-line extrusion systems integrated with AI-driven quality monitoring. Capital expenditure in advanced pasta manufacturing process technology exceeded USD 2.4 Billion globally in 2024, according to the International Pasta Organisation [3]. Innovations such as 3D-printed pasta shapes and high-protein formulations using pulse flour blends are redefining product portfolios for major producers. Whole wheat and enriched pasta formulations now represent a fast-growing niche as nutritional awareness deepens across demographics.

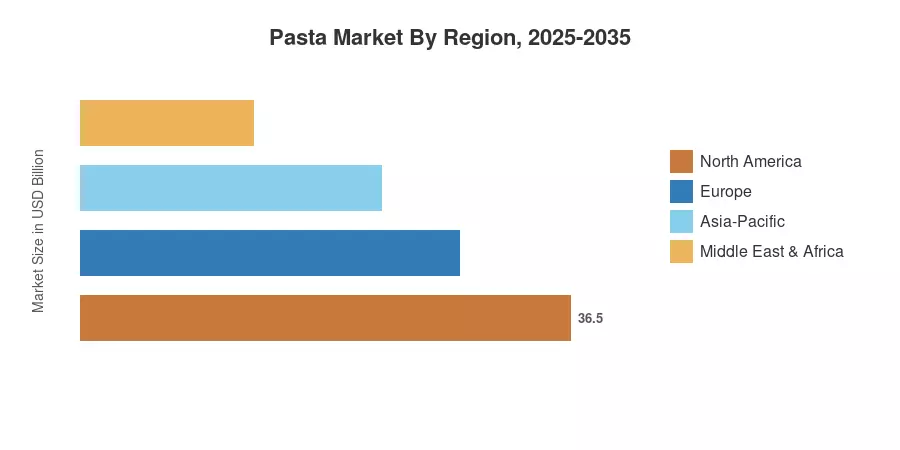

Europe commands the largest share of the Pasta Market at approximately 38.4% of global revenue in 2025, anchored by Italy's dominant production and export ecosystem Asia-Pacific stands out as the fastest-growing region with a projected CAGR of 8.07%, driven by rapid urbanization and the adoption of westernized diets in China and India. North America holds the second-largest position, with strong retail penetration of gluten-free pasta varieties and dried and fresh pasta types fueling steady demand. The decade ahead promises accelerated consolidation and innovation across every segment of the Pasta Market.

Key Report Takeaways

• By Product Type

- Dried pasta led the Pasta Market with a 75.93% revenue share in 2025, reflecting its unmatched shelf stability and cost efficiency among dried and fresh pasta types

- Fresh/chilled pasta is forecast to expand at a 9.92% CAGR through 2035, propelled by consumer preference for artisanal and gourmet offerings

• By Category

- Conventional durum wheat semolina pasta captured USD 72.95 Billion in 2025, underscoring the enduring consumer preference for traditional formulations

- Free-form and specialty products — including gluten-free pasta varieties — are advancing at a 10.15% CAGR, the fastest among all category segments

• By Region

- Europe held a 38.4% share of the Pasta Market in 2025, buoyed by Italy's robust export infrastructure

- Asia-Pacific is on course for an 8.07% CAGR over the forecast period, making it the Pasta Market's primary growth engine

- North America accounted for approximately USD 22.37 Billion in 2025, with whole wheat and enriched pasta gaining shelf space rapidly

Pasta Market Size and Forecast (2021–2035)

MRFR's Pasta Market sizing draws on primary interviews with leading producers, distributor shipment data, trade association statistics from the International Pasta Organisation (IPO), and customs/import-export records across 45 countries. Historical figures (2021–2024) reflect actual reported data, while the base year (2025) represents validated estimates. Forecast projections (2026–2035) apply a calibrated CAGR model adjusted for macroeconomic indicators, commodity price trends for durum wheat semolina pasta, and category-level adoption curves for gluten-free pasta varieties and whole wheat and enriched pasta.