Smart Medical Devices Market Summary

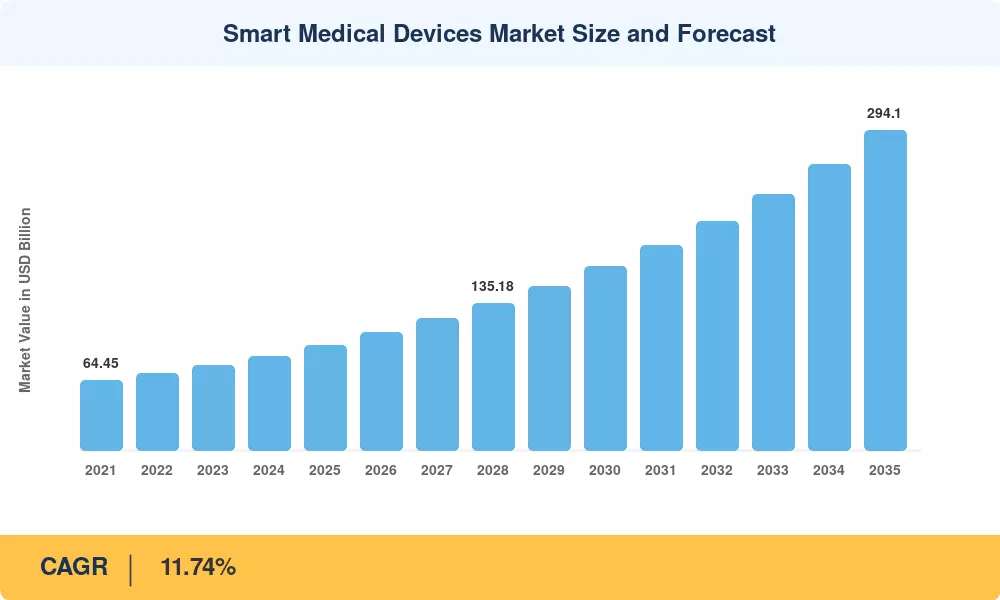

The Global Smart Medical Devices Market size was valued at USD 96.88 Billion in 2025, and the market is projected to grow from USD 108.25 Billion in 2026 to USD 294.10 Billion by 2035, registering a CAGR of 11.74% during the forecast period 2026–2035. Two catalysts are reshaping the landscape: the U.S. FDA's 2025 draft guidance on performance baselines for software-as-a-medical-device, which has lowered regulatory ambiguity and drawn fresh venture commitments, and the European Commission's EUR 1.3 Billion digital-health allocation under Horizon Europe, which is accelerating cross-border interoperability frameworks [1][2].

A fundamental technology shift is underway. Legacy standalone instruments — bedside monitors that print paper strips, glucometers requiring manual logbooks — are giving way to sensor-rich platforms that fuse edge AI with 5G backhaul. In 2024 alone, digital-health venture funding exceeded USD 16 Billion globally, with roughly 38% directed at connected diagnostics and continuous-monitoring platforms [3]. Miniaturised semiconductors and MEMS sensors now cost less than a third of their 2019 equivalents, enabling OEMs to embed intelligence into devices previously considered too low-margin for connectivity.

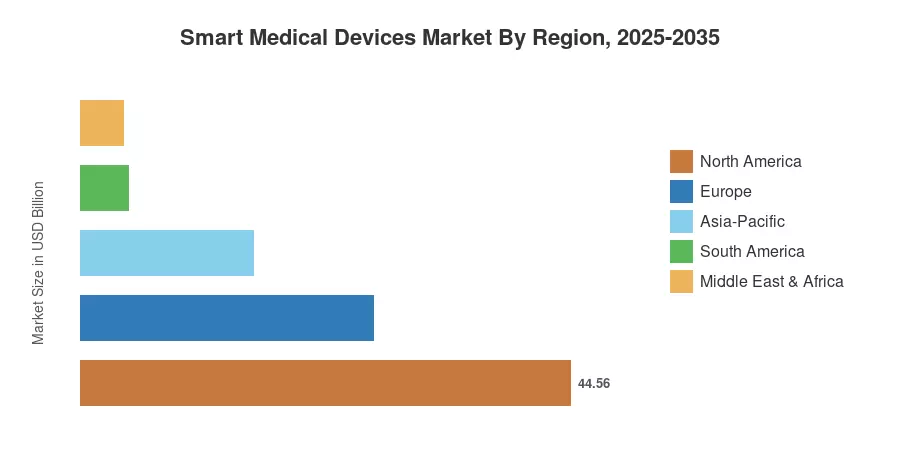

North America commanded approximately 46.0% of the Smart Medical Devices Market in 2025, buoyed by value-based reimbursement models that reward real-time outcome tracking. Asia-Pacific is the fastest-expanding region, posting a projected CAGR of 16.24% through 2035 as government-led digitisation campaigns in India, China, and ASEAN nations drive adoption. Europe held the second-largest share at an estimated 27.5%, anchored by the EU MDR transition and growing telehealth mandates. The convergence of payer incentives, component deflation, and clinical evidence is positioning the Smart Medical Devices Market for sustained double-digit expansion over the coming decade.

Key Report Takeaways

• By Product Type

- Diagnostic and monitoring devices captured roughly 58.6% of the Smart Medical Devices Market in 2025, reflecting strong demand for continuous glucose monitors, pulse oximeters, and AI-enabled imaging peripherals.

- Therapeutic devices are forecast to register the fastest segment CAGR of approximately 14.2% through 2035 as smart insulin pumps, closed-loop neurostimulators, and robotic surgical assistants gain regulatory clearances.

• By End User

- Hospitals and clinics represented about 48.9% of the Smart Medical Devices Market in 2025, driven by enterprise-wide interoperability mandates and bundled procurement contracts.

- Home-care settings are expected to expand at a 14.78% CAGR, the quickest among end-user categories, fuelled by aging demographics and insurer-funded remote-monitoring programmes.

• By Region

- North America led with a 46.0% share of the Smart Medical Devices Market in 2025.

- Asia-Pacific is projected to grow at a 16.24% CAGR through 2035, with China, India, and Japan serving as primary growth engines.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework triangulates revenue data from public filings, regulatory databases, primary interviews with device OEMs, and secondary syndicated sources. Historical figures (2021–2024) reflect audited shipment data and ASP tracking; forecast figures (2026–2035) apply a compound growth model calibrated against macroeconomic indicators and healthcare-expenditure projections.