Specialty Medical Chairs Market Summary

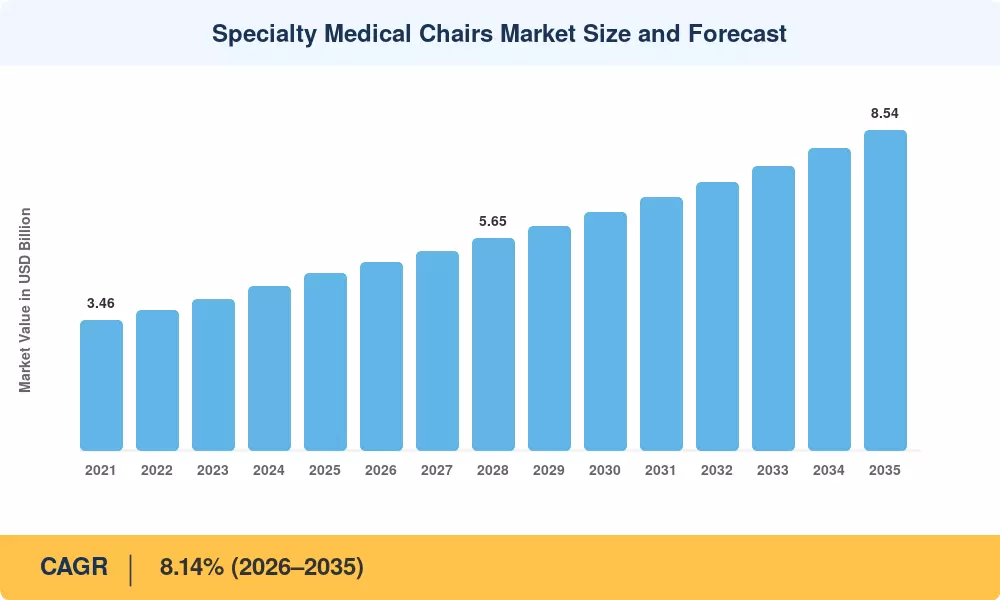

The Global Specialty Medical Chairs Market size was valued at USD 4.73 Billion in 2025, and the market is projected to grow from USD 5.04 Billion in 2026 to USD 8.54 Billion by 2035, registering a CAGR of 6.04% during the forecast period 2026–2035. Two converging forces are accelerating this expansion: aging populations requiring prolonged outpatient treatments and a decisive policy push by payers and regulators toward ambulatory-first care delivery models. The U.S. Centers for Medicare & Medicaid Services (CMS) alone shifted an estimated USD 11.2 billion in procedural reimbursement from inpatient to outpatient settings between 2022 and 2025, directly increasing demand for purpose-built seating across day-surgery, infusion, and dialysis facilities [2].

The Specialty Medical Chairs Market is experiencing a technology change with fully electric programmable platforms embedded with IoT sensors replacing legacy hydraulic and manual-adjust units. These next-gen chairs automate Trendelenburg positioning, height adjustment and tilt sequencing, decreasing room turnover times by as much as 22% and reducing caregiver musculoskeletal injuries that account for about a third of nursing lost-time incidents [3]. The Joint Commission published pressure-injury criteria in 2024 that are forcing hospitals to replace old inventory with sensor-equipped devices that can digitally capture patient repositioning events [4].

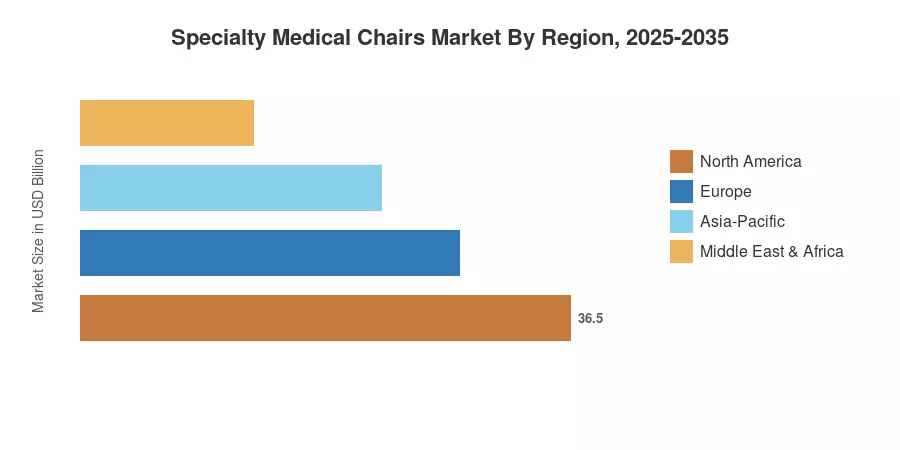

The Specialty Medical Chairs Market in North America holds around 39.2% of the worldwide market share, owing to high per capita healthcare expenditure and tight ergonomic compliance regulations. Asia-Pacific is the fastest expanding market at 8.14% CAGR driven by hospital capacity expansion in India, China and ASEAN countries. Next up is Europe, with EU Medical Device Regulation (MDR) enhancements that demand fleet-wide equipment renewals. The next decade will be rewarding for manufacturers that build cybersecurity compliance, flexible upgrade paths and predictive maintenance into their product strategy.

Key Report Takeaways

• By Product Type

- Examination chairs accounted for 40.7% of the Specialty Medical Chairs Market revenue in 2025, led by primary-care and diagnostic facility procurement cycles.

- Treatment chairs are expanding at a 7.84% CAGR through 2035, propelled by rising outpatient chemotherapy and infusion volumes.

• By End User

- Hospitals represented 39.8% of total spending in 2025, anchored by surgical suite and emergency department replacement programs.

- Ambulatory surgery and day-care centers are the fastest-growing end-user segment at a 9.95% CAGR, reflecting reimbursement migration.

• By Technology

- Fully electric programmable models captured 41.4% of the Specialty Medical Chairs Market technology spend in 2025, supported by workforce safety mandates.

• By Geography

- North America led the Specialty Medical Chairs Market with a 39.2% share in 2025.

- Asia-Pacific is advancing at an 8.14% CAGR, the fastest among all regions through 2035.

Specialty Medical Chairs Market Size and Forecast (2021–2035)

Market Research Future’s sizing methodology combines a bottom-up revenue model based on manufacturer shipments and facility procurement databases with a top-down validation against healthcare capital expenditure benchmarks released by the WHO and OECD through a triangulation approach. Historical estimates (2021–2024) are based on audited company filings and customs trade data, while projected forecasts (2026–2035) take into account population aging indices, reimbursement policy trajectories and planned hospital development pipelines[5].