Telehealth Market Summary

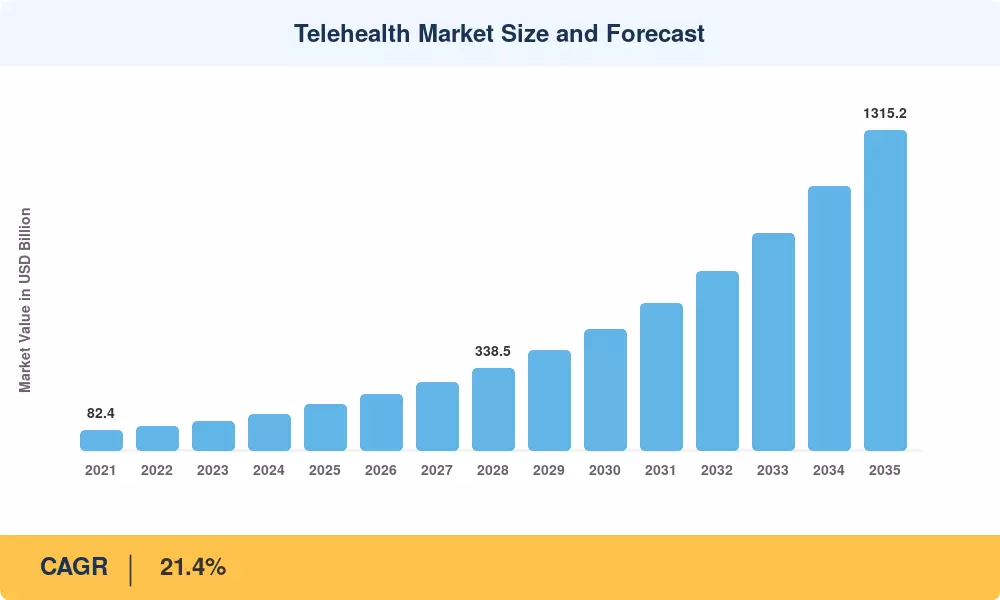

The Telehealth Market size was valued at USD 189.20 Billion in 2025, and the market is projected to grow from USD 229.70 Billion in 2026 to USD 1,315.20 Billion by 2035, registering a CAGR of 21.4% during the forecast period 2026–2035. This trajectory reflects a healthcare system in active reconfiguration — the U.S. Centers for Medicare & Medicaid Services permanently extended over 250 telehealth billing codes in late 2024, while the European Commission committed EUR 1.3 billion to its European Health Data Space initiative, both acting as structural demand accelerators for the Telehealth Market through 2035 [1][2].

The technology transformation underway is displacing legacy in-clinic-only care models with AI-augmented, cloud-native delivery architectures. Hospital systems that once relied on fragmented electronic health record (EHR) portals are migrating to unified platforms capable of asynchronous triage, real-time video consultations, and remote diagnostics. Global venture funding into digital health surpassed USD 18.5 billion across 2023–2024, with a growing share flowing into ambient clinical intelligence and chronic-disease monitoring solutions [3].

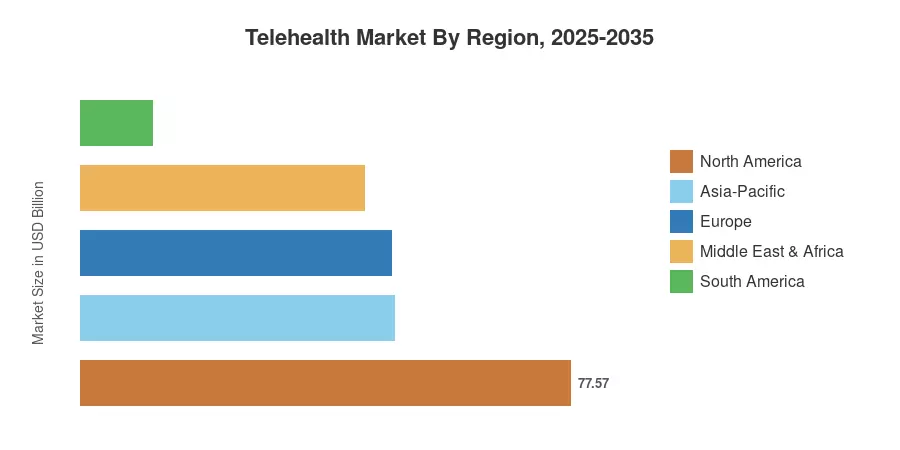

North America commands the largest share of the Telehealth Market at approximately 41% of global revenue, supported by mature payer reimbursement frameworks and high broadband penetration. Asia-Pacific is the fastest-growing region with a forecast CAGR of 26.3%, driven by India's Ayushman Bharat Digital Mission and China's internet-hospital licensing expansion. Europe holds the second-largest share at roughly 26%, anchored by the NHS's digital-first primary care mandate and Germany's DiGA regulatory pathway for prescribed digital health applications. The Telehealth Market is positioned for sustained double-digit expansion as regulatory permanence replaces pandemic-era temporary flexibilities.

Key Report Takeaways

• By Product Type

- Services dominate the Telehealth Market, accounting for approximately 52% of global revenue in 2025, driven by physician adoption of synchronous and asynchronous consultation workflows.

- Software is the fastest-growing product segment with a projected CAGR of 24.8% through 2035, fueled by enterprise demand for interoperable platform licensing.

- Hardware contributes USD 34.20 Billion in 2025, reflecting continued investment in connected diagnostic peripherals and kiosk-based telehealth stations.

• By Application

- Teleconsultations represent the largest application segment within the Telehealth Market, holding an estimated 58% share in 2025.

- Teleradiology is growing at a CAGR of 22.1%, supported by AI-assisted image interpretation and cross-border diagnostic outsourcing.

• By Region

- North America remains the dominant region for the Telehealth Market, contributing roughly 41% of global revenue.

- Asia-Pacific leads regional growth trajectories with a projected CAGR of 26.3% across the forecast period.

- Europe accounts for an estimated USD 49.19 Billion in 2025, with regulatory clarity accelerating adoption.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary sizing model triangulates bottom-up provider billing data, top-down payer reimbursement volumes, and vendor-disclosed platform utilization metrics to construct the Telehealth Market forecast below. Historical values reflect audited industry benchmarks adjusted for post-pandemic utilization normalization.