Transdermal Drug Delivery Systems Market Summary

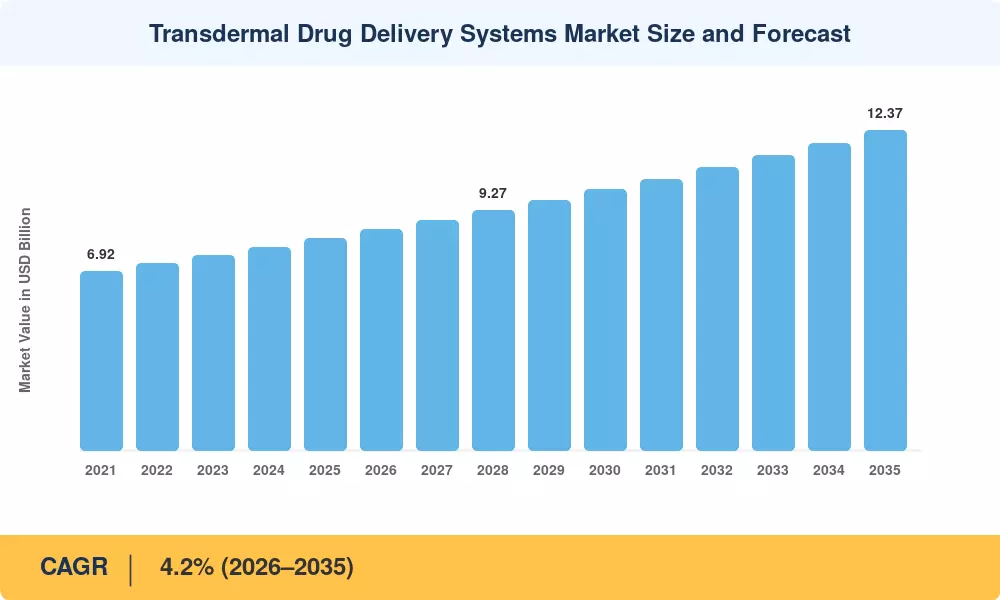

The Global Transdermal Drug Delivery Systems Market size was valued at USD 8.20 Billion in 2025, and the market is projected to grow from USD 8.54 Billion in 2026 to USD 12.37 Billion by 2035, registering a CAGR of 4.2% during the forecast period 2026–2035. Rising prevalence of chronic diseases — cardiovascular conditions, neurological disorders, and chronic pain — has pushed pharmaceutical companies and healthcare systems to prioritize non-invasive delivery mechanisms that improve patient compliance. The U.S. FDA's accelerated review pathways for novel patch formulations, combined with aging populations across OECD nations, are creating sustained demand tailwinds [1][2].

A quiet but consequential shift is reshaping how drugs reach the bloodstream. Traditional oral dosage forms, long the default for chronic therapy, face well-documented problems: first-pass metabolism, gastrointestinal irritation, and inconsistent bioavailability. Patch-based systems bypass these hurdles entirely. Global pharmaceutical R&D investment in advanced delivery technologies exceeded USD 45 billion in 2024, with a growing share directed toward microneedle arrays, iontophoretic patches, and nanoparticle-enhanced formulations [3][4].

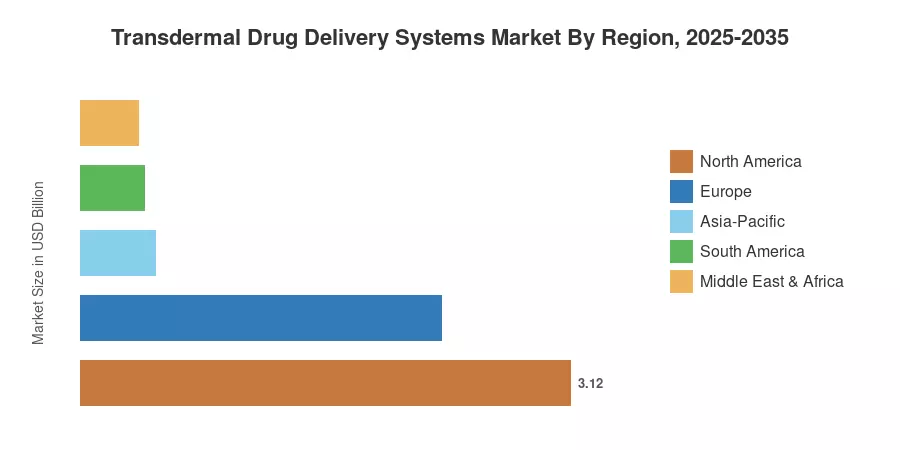

North America commands roughly 38% of the Transdermal Drug Delivery Systems Market, anchored by deep payer coverage and a mature generics pipeline. Asia-Pacific stands out as the fastest-growing region at a projected CAGR of 5.8%, driven by expanding healthcare access in India and China. Europe holds approximately a 28% share, supported by strong regulatory harmonization under the European Medicines Agency. The decade ahead will see biosimilar patch entries and digital health integration reshape competitive dynamics across every geography.

Key Report Takeaways

• By Type

- Drug-in-adhesive patches dominate the Transdermal Drug Delivery Systems Market with an estimated 42% revenue share, reflecting their manufacturing simplicity and broad therapeutic compatibility.

- Microneedle-based systems are projected to register the highest CAGR of 8.1% through 2035, as clinical pipelines advance toward commercialization.

- Reservoir-type patches account for approximately USD 1.56 billion in 2025 revenue.

• By Application

- Cardiovascular applications represent about 31% of total market value, sustained by widespread statin and nitrate patch prescriptions.

- Pain management is the fastest-expanding application segment, with a forecast CAGR of 5.4%.

• By Region

- North America generated approximately USD 3.12 billion in 2025, led by the United States.

- The Transdermal Drug Delivery Systems Market in Asia-Pacific is expanding at a CAGR of 5.8%, the highest among all regions.

- Europe accounts for roughly 28% of global revenue.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology integrates bottom-up revenue estimation from manufacturer shipments, prescription volume data, and payer reimbursement databases across 40+ countries. Historical figures (2021–2024) rely on audited company filings and IMS Health prescription data, while forecast projections (2026–2035) apply a weighted-average CAGR calibrated against demographic trends, pipeline maturity, and regulatory calendars[6].