US Proteinuria Treatment Market Overview

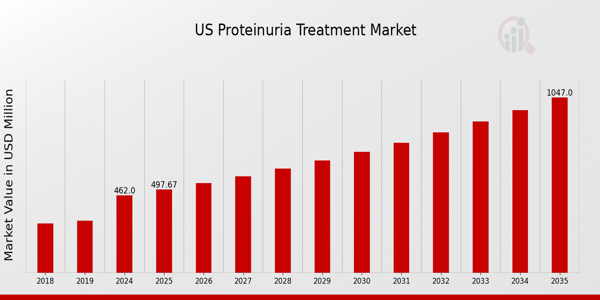

As per MRFR analysis, the US Proteinuria Treatment Market Size was estimated at 431.09 (USD Million) in 2023. The US Proteinuria Treatment Market Industry is expected to grow from 462 (USD Million) in 2024 to 1,047 (USD Million) by 2035. The US Proteinuria Treatment Market CAGR (growth rate) is expected to be around 7.721% during the forecast period (2025 - 2035).

Key US Proteinuria Treatment Market Trends Highlighted

The US Proteinuria Treatment Market is witnessing significant growth driven by increasing awareness of kidney diseases and the rising incidence of conditions such as diabetes and hypertension, which are closely linked to proteinuria. The emphasis on early diagnosis and treatment is fostering a shift towards more advanced diagnostic tools and therapies. Additionally, there is a growing trend towards personalized medicine, where treatments are tailored to individual patient profiles, enhancing their effectiveness and improving outcomes. This focus on customized therapy reflects a broader movement in the healthcare sector towards precision treatment strategies.

Opportunities within the market are primarily centered around technological advancements. Innovators are developing novel therapeutic agents and drugs specifically aimed at managing proteinuria. Furthermore, the integration of telemedicine in patient care offers convenient access to specialists, which reflects a shift towards remote management of chronic conditions while improving patient engagement and adherence to treatment regimens.

In recent times, there has been an increase in clinical trials focusing on proteinuria treatments in the US, indicating strong interest in developing effective therapies. Regulatory bodies are also playing a crucial role by streamlining the approval process for new treatments, enabling quicker access for patients. This trend is complemented by funding initiatives for research into kidney diseases, which underscores the urgency to address renal health in the US. As a result, healthcare companies are exploring partnerships and collaborations to expedite the development of new solutions for proteinuria, capturing the market potential effectively.

Source: Primary Research, Secondary Research, Market Research Future Database and Analyst Review

US Proteinuria Treatment Market Drivers

Increasing Prevalence of Chronic Kidney Disease

The increasing prevalence of Chronic Kidney Disease (CKD) in the United States is a significant driver for the US Proteinuria Treatment Market Industry. According to the Centers for Disease Control and Prevention (CDC), approximately 15% of American adults, or about 37 million people, have CKD. This growing patient population presents an urgent need for effective proteinuria treatments, as proteinuria is a common sign and a predictor of CKD progression.

The National Kidney Foundation's educational campaigns underline this urgency, as untreated CKD can lead to more severe health conditions, necessitating costly treatments such as dialysis or kidney transplants. Furthermore, the focus on early diagnosis and management to reduce healthcare costs is pivotal, with projections suggesting a significant rise in demand for proteinuria-specific therapies over the next decade. This translates into a thriving market as increased awareness and the rise in CKD cases drive the adoption of novel treatment modalities.

Advancements in Research and Development

The US Proteinuria Treatment Market Industry is significantly bolstered by advancements in Research and Development (R&D) for novel therapies. Major pharmaceutical companies such as Pfizer, Merck, and Johnson & Johnson are heavily investing in R&D for drugs specifically targeting proteinuria, with the aim of improving treatment outcomes for patients with CKD and other related conditions.

The U.S. National Institutes of Health (NIH) reported an increase of nearly 5% in funding for kidney disease research last fiscal year, boosting the pipeline of potential therapies. This investment is expected to bring new proteinuria treatments to market, addressing unmet medical needs and consequently driving market growth as these innovative solutions become available to healthcare providers.

Increasing Awareness and Education Programs

Rising awareness and educational programs aimed at both healthcare providers and patients are also vital drivers of the US Proteinuria Treatment Market Industry. Organizations such as the American Kidney Fund and the National Kidney Foundation are increasingly engaging in campaigns to educate the public about kidney health and the implications of proteinuria.

A study published in the American Journal of Kidney Diseases found that educational interventions significantly improved patient understanding of CKD risks and management strategies. This increased awareness leads to higher rates of early diagnosis and treatment adherence, driving demand for related therapies. As more people become informed about the risks associated with proteinuria and CKD, the need for effective treatments is expected to grow.

US Proteinuria Treatment Market Segment Insights

Proteinuria Treatment Market Disease Type Insights

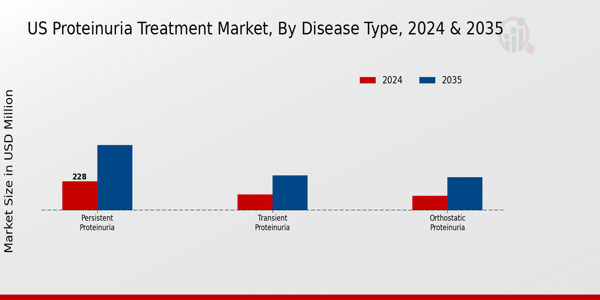

The US Proteinuria Treatment Market, particularly within the Disease Type segment, presents a diverse landscape characterized by various conditions that lead to proteinuria. Among these, Transient Proteinuria is particularly noteworthy, as it often resolves itself quickly and is frequently associated with temporary factors such as dehydration, stress, or vigorous exercise. This type is commonly detected in routine screenings, playing a critical role in initiating follow-up and potential diagnosis.

On the other hand, Orthostatic Proteinuria is identified when individuals experience proteinuria during standing, typically affecting adolescents and young adults. The significance of Orthostatic Proteinuria lies in its benign nature, generally requiring monitoring rather than intensive treatment; however, its recognition remains essential to distinguish from underlying renal diseases.

The third condition, Persistent Proteinuria, is of great concern as it serves as a potential marker for chronic kidney disease or other serious health issues. Persistent Proteinuria can lead to severe long-term health implications, garnering attention from healthcare professionals and researchers alike. The increasing prevalence of diabetes and hypertension within the US population further drives the demand for effective treatments and management protocols across these disease types.

Overall, the US Proteinuria Treatment Market is shaped significantly by these disease types, each influencing patient management strategies and healthcare outcomes in unique ways. The ongoing research and advancements in treatment options for these conditions underline the importance of this market segment in improving patient quality of life and enhancing healthcare strategies in the United States.

Source: Primary Research, Secondary Research, Market Research Future Database and Analyst Review

Proteinuria Treatment Market Drug Class Insights

The Drug Class segment within the US Proteinuria Treatment Market plays a crucial role in the management of proteinuria, a condition often associated with chronic kidney disease and other renal disorders. Angiotensin-converting Enzyme (ACE) Inhibitors and Angiotensin Receptor Blockers (ARBs) are particularly significant for their ability to lower blood pressure and reduce protein loss, thereby protecting kidney function.

Dipeptidyl Peptidase (DPP) IV Inhibitors are gaining attention due to their effectiveness in managing diabetes, which may co-exist with proteinuria, suggesting an integrated approach to treatment. Aldosterone Antagonists are important for their role in diuresis and combating sodium retention, which can contribute to proteinuria. Selective use in proteinuria is increasingly recognized for tailoring treatment plans based on individual patient needs.

Diuretics also play a supportive role in reducing fluid overload, enhancing kidney function, and relieving symptoms associated with hypertension. This diversity in the Drug Class segment reflects a comprehensive strategy to manage proteinuria, addressing both systemic conditions and renal health, which is critical as the prevalence of kidney-related ailments continues to rise in the US.

Proteinuria Treatment Market Route of Administration Insights

The Route of Administration segment within the US Proteinuria Treatment Market plays a crucial role in determining the effectiveness and convenience of therapeutic approaches for managing proteinuria. This market segment comprises various delivery methods, primarily focusing on Oral and Intravenous administration.

Oral treatments are often favored due to their ease of use, patient compliance, and the ability to take medications at home, thus significantly contributing to the overall market growth. Intravenous treatments, on the other hand, are critical for cases requiring immediate intervention, providing rapid therapeutic effects, particularly in hospital settings.

The segmentation underscores a shift toward personalized medicine, with healthcare providers increasingly tailoring treatment routes based on patient needs, conditions, and preferences. This flexibility allows for improved management of proteinuria and enhances patient quality of life. Furthermore, the increasing prevalence of chronic kidney diseases in the United States drives demand for innovative treatment options, resulting in a dynamic environment for the US Proteinuria Treatment Market. The focused developments in drug formulations and delivery mechanisms are expected to enhance treatment efficacy and patient outcomes, ensuring that both administration routes maintain significance in the evolving landscape of proteinuria management.

Proteinuria Treatment Market Distribution Channel Insights

The Distribution Channel segment within the US Proteinuria Treatment Market plays a pivotal role in ensuring accessibility and availability of therapeutic options for patients. Hospital Pharmacies contribute significantly by providing medications directly to hospitalized patients, ensuring immediate access to treatment regimens, while also offering comprehensive patient management services.

Retail Pharmacies dominate by serving the general population, presenting a crucial touchpoint for outpatient prescriptions and patient education. Their extensive networks across urban and rural areas facilitate easy access to proteinuria treatments.

Meanwhile, Online Pharmacies have gained traction, particularly following advancements in digital health, enabling patients to order medications conveniently from the comfort of their homes. This growth is driven by increased consumer preference for online services, expedited delivery options, and the rise of telehealth services. Through these varied channels, the market demonstrates flexibility in meeting diverse patient needs, enhancing the overall reach of proteinuria treatments across the US healthcare landscape. The evolution of these distribution channels reflects broader trends in the market, where patient-centric models and accessibility are prioritized, indicating a dynamic and responsive industry landscape.

US Proteinuria Treatment Market Key Players and Competitive Insights

The US Proteinuria Treatment Market is characterized by a diverse array of pharmaceutical products aimed at managing and treating conditions associated with excess protein in urine, a common marker of kidney disease. The market features a competitive landscape populated by various players who offer a mix of established treatments and innovative therapies.

The increasing prevalence of kidney disorders and the rising awareness about the importance of early diagnosis and management have spurred growth in this sector. Companies are focusing on enhancing their product offerings through advanced formulations, improved delivery mechanisms, and novel therapeutic approaches. Additionally, the landscape is marked by strategic partnerships, collaborations, and mergers among key players, which further intensify the competition and accelerate the pace of innovation.

Celgene stands as a notable player within the US Proteinuria Treatment Market, leveraging its strong research and development capabilities to provide effective treatments aimed at managing proteinuria-related conditions. The company has established a strong presence through its innovative therapies that target underlying mechanisms contributing to excess protein in urine.

Celgene's strengths lie in its commitment to advancing clinical research and focusing on patient-centered solutions. By maintaining robust relationships with healthcare providers and investing in educational initiatives, the company ingrains itself in the healthcare ecosystem effectively. The strong pipeline of products poised for market approval amplifies its competitive edge, enabling Celgene to respond promptly to the evolving needs of patients suffering from kidney disease.

Novartis occupies a significant position within the US Proteinuria Treatment Market, boasting a portfolio of key products designed to mitigate the impact of proteinuria in patients with chronic kidney diseases. The company's market presence is bolstered by its focus on innovative therapies and a proactive approach to research and development.

Novartis emphasizes the importance of addressing the unmet needs in the field of nephrology through ongoing clinical trials and collaborations with leading academic institutions. That positions Novartis favorably among prescribers and healthcare professionals. Moreover, the company has engaged in strategic mergers and acquisitions that enhance its capabilities in renal therapies, thus fortifying its market reach and reinforcing its reputation as a leader in this niche area. Novartis strives to improve patient outcomes through its comprehensive offerings and commitment to advancing treatment in the US proteinuria landscape.

Key Companies in the US Proteinuria Treatment Market Include

US Proteinuria Treatment Market Industry Developments

The US Proteinuria Treatment Market has witnessed significant developments recently. Important regulatory decisions have been made, including the FDA approving new medications aimed at reducing protein levels in patients with chronic kidney disease, which has spurred investment and research efforts among leading companies like Celgene, Novartis, and Merck.

Additionally, the growing prevalence of kidney-related disorders in the US, attributed to factors such as diabetes and hypertension, is fueling market growth. In terms of mergers and acquisitions, Eli Lilly announced its acquisition of a biotech firm in April 2023, bolstering its pipeline in kidney disease therapeutics.

Furthermore, Gilead Sciences has expanded its research initiatives in the sector, focusing on innovative solutions for proteinuria, which has been positively received in the market. The overall market valuation for key players like Bristol Myers Squibb and Pfizer has shown upward momentum, reflecting increased investor interest and confidence in the future of proteinuria treatments.

Furthermore, in 2022, Sanofi launched a targeted campaign to raise awareness about the importance of proteinuria monitoring among healthcare providers and patients, highlighting the growing focus on this area. These dynamics indicate a vibrant and evolving landscape for the US Proteinuria Treatment Market.

US Proteinuria Treatment Market Segmentation Insights

Proteinuria Treatment Market Disease Type Outlook

Proteinuria Treatment Market Drug Class Outlook

- Angiotensin-converting Enzyme (ACE) Inhibitors

- Angiotensin Receptor Blockers (ARBs)

- Dipeptidyl Peptidase (DPP) IV Inhibitors

- Selective use in proteinuria

Proteinuria Treatment Market Route of Administration Outlook

Proteinuria Treatment Market Distribution Channel Outlook

| Report Attribute/Metric Source: |

Details |

| MARKET SIZE 2018 |

431.09(USD Million) |

| MARKET SIZE 2024 |

462.0(USD Million) |

| MARKET SIZE 2035 |

1047.0(USD Million) |

| COMPOUND ANNUAL GROWTH RATE (CAGR) |

7.721% (2025 - 2035) |

| REPORT COVERAGE |

Revenue Forecast, Competitive Landscape, Growth Factors, and Trends |

| BASE YEAR |

2024 |

| MARKET FORECAST PERIOD |

2025 - 2035 |

| HISTORICAL DATA |

2019 - 2024 |

| MARKET FORECAST UNITS |

USD Million |

| KEY COMPANIES PROFILED |

Celgene, Novartis, AstraZeneca, Merck, Eli Lilly, GlaxoSmithKline, BristolMyers Squibb, Gilead Sciences, Pfizer, Amgen, Roche, AbbVie, Sanofi, Johnson and Johnson, Bayer |

| SEGMENTS COVERED |

Disease Type, Drug Class, Route of Administration, Distribution Channel |

| KEY MARKET OPPORTUNITIES |

Increased awareness and screening programs, Development of targeted therapies, Expansion of telemedicine solutions, Personalized medicine advancements, Collaborations with healthcare providers |

| KEY MARKET DYNAMICS |

Rising prevalence of kidney diseases, Increased awareness of proteinuria, Advancements in diagnostic technologies, Growing demand for targeted therapies, Expanding healthcare reimbursement options |

| COUNTRIES COVERED |

US |

Frequently Asked Questions (FAQ):

The US Proteinuria Treatment Market is expected to be valued at 462.0 million USD in 2024.

By 2035, the US Proteinuria Treatment Market is projected to reach 1047.0 million USD.

The expected CAGR for the US Proteinuria Treatment Market during the forecast period is 7.721%.

Transient Proteinuria is valued at 122.0 million USD in 2024 and is expected to grow to 274.0 million USD by 2035.

Orthostatic Proteinuria is projected to be valued at 112.0 million USD in 2024 and reach 258.0 million USD by 2035.

Persistent Proteinuria is expected to be valued at 228.0 million USD in 2024 and grow to 515.0 million USD by 2035.

Major players in the market include Celgene, Novartis, AstraZeneca, Merck, and Eli Lilly.

The market faces challenges such as regulatory hurdles and the need for innovative treatment options.

Emerging trends include advancements in personalized medicine and increased focus on preventive care.

The growth rate varies, with Persistent Proteinuria expected to experience significant growth, reflecting the increasing prevalence of chronic kidney diseases.