Vanilla Bean Market Summary

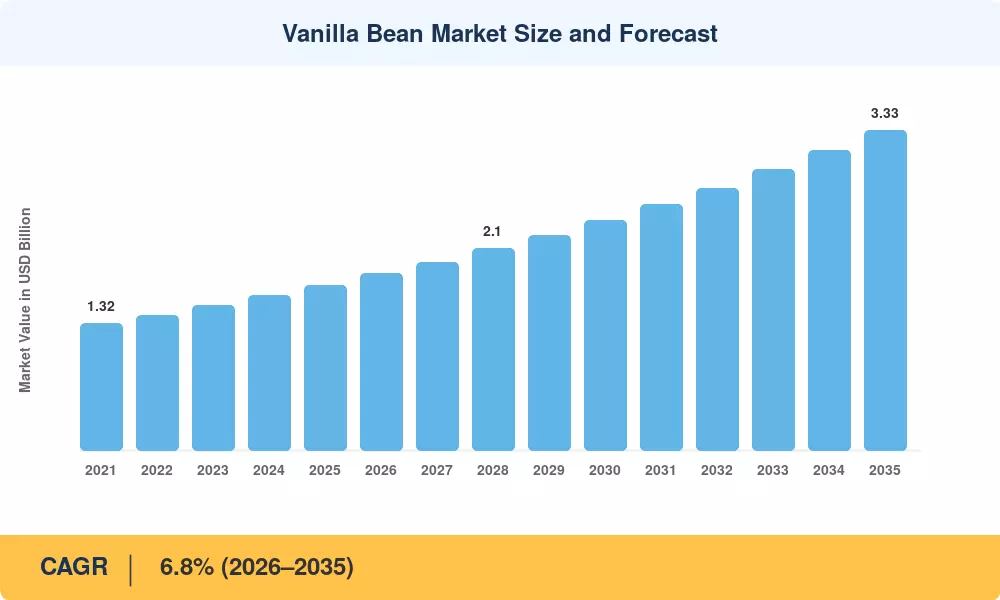

The vanilla bean market reached an estimated USD 1.72 billion in 2025 and is projected to grow from USD 1.84 billion in 2026 to USD 3.33 billion by 2035, registering a CAGR of 6.8% across the forecast period. Clean-label legislation in the EU and the U.S. FDA's tightened guidelines on "natural flavor" declarations have pushed food manufacturers to replace synthetic vanillin with natural vanilla flavor compounds, creating a demand floor that price volatility alone cannot erode [2]. The global ice cream sector — valued at over USD 90 billion — remains the single largest consumption channel, and premium brands increasingly specify origin-traceable vanilla planifolia cultivation sources from Madagascar and Comoros [3].

Supply-side transformation is accelerating across the vanilla bean market. Controlled-environment agriculture pilots in Israel, Australia, and the Netherlands are challenging the centuries-old model of open-field vanilla planifolia cultivation by compressing the 9-month curing and drying vanilla beans cycle to under 4 months using enzymatic and ultrasonic post-harvest techniques [4]. Blockchain-verified traceability platforms now cover roughly 18% of globally traded vanilla extract and vanilla paste volumes, up from less than 3% in 2020 [5].

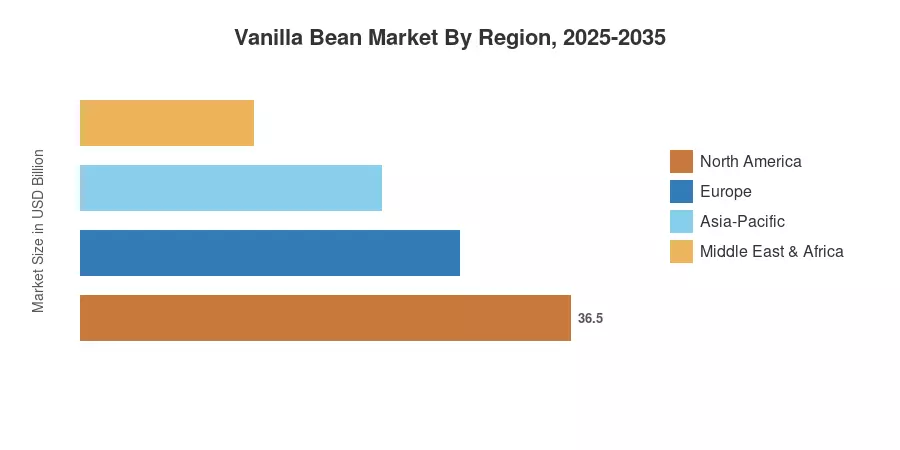

North America holds an estimated 35.2% share of the vanilla bean market, anchored by the United States' outsized demand for natural vanilla flavor compounds in dairy, bakery, and personal-care formulations. Asia-Pacific represents the fastest-growing region at a projected CAGR of 7.8%, driven by rising consumption of Western-style desserts in China and India. Europe remains the second-largest consumption base, accounting for roughly 28.4% of global value, with France and Germany serving as refining and re-export hubs for Madagascar and Tahitian vanilla beans.

Key Report Takeaways

• By Form

- Whole vanilla beans commanded the largest revenue share in the vanilla bean market in 2025, driven by artisanal bakery and fine-dining demand for premium-grade pods.

- Vanilla extract and vanilla paste collectively represent the fastest-growing form segment at a CAGR of 7.4%, fueled by industrial food-processing scalability.

• By Application

- Food and beverage applications accounted for over 68% of the global vanilla bean market consumption in 2025, with ice cream and confectionery as dominant end-use channels.

- Cosmetics and personal-care applications are projected to reach USD 0.52 billion by 2035 as Madagascar and Tahitian vanilla beans gain traction in fragrance formulations.

• By Region

- North America held a 35.2% share of the vanilla bean market in 2025, supported by robust clean-label and organic certification mandates.

- Asia-Pacific is expected to register a 7.8% CAGR through 2035, with China and India leading demand for natural vanilla flavor compounds.

Vanilla Bean Market Size and Forecast (2021–2035)

MRFR's market sizing combines customs trade data from UN Comtrade, farm-gate price surveys in Madagascar, Uganda, and Papua New Guinea, and proprietary demand-side modeling calibrated against quarterly earnings disclosures from leading flavor houses. Historical values reflect actual traded volumes adjusted for quality-grade price differentials; forecast values apply an econometric model linking clean-label regulatory adoption, vanilla planifolia cultivation area expansion, and downstream reformulation rates[7].