Wealth Management Platform Market Summary

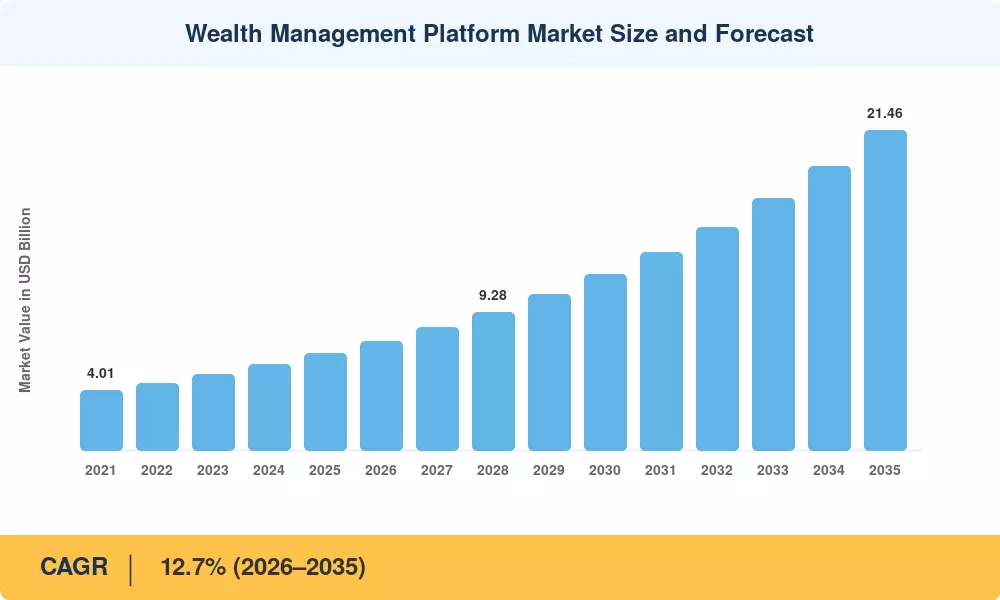

The Wealth Management Platform Market stood at USD 6.48 Billion in 2025 and is set to reach USD 21.46 Billion by 2035, expanding at a 12.7% CAGR across the 2026–2035 forecast window. Two forces are accelerating spending: the U.S. SEC's Regulation Best Interest, which pushed broker-dealers toward fee-based advisory and compliance-ready technology stacks, and the European Union's Digital Operational Resilience Act (DORA), which compels wealth firms to overhaul third-party risk management by January 2025. Together, these mandates are converting discretionary IT budgets into non-negotiable platform investments.

The technology shift underway in the Wealth Management Platform Market is structural. Spreadsheet-driven portfolio reconciliation, manual KYC workflows, and siloed custody reporting — staples of the advisory world through 2020 — are giving way to cloud-native, API-first platforms that ingest alternative datasets, tokenized-asset registries, and behavioral signals in near real time. Global wealth-tech venture funding topped USD 5.3 billion in 2024, according to, underscoring investor conviction that advisor-facing software still has a long runway [1].

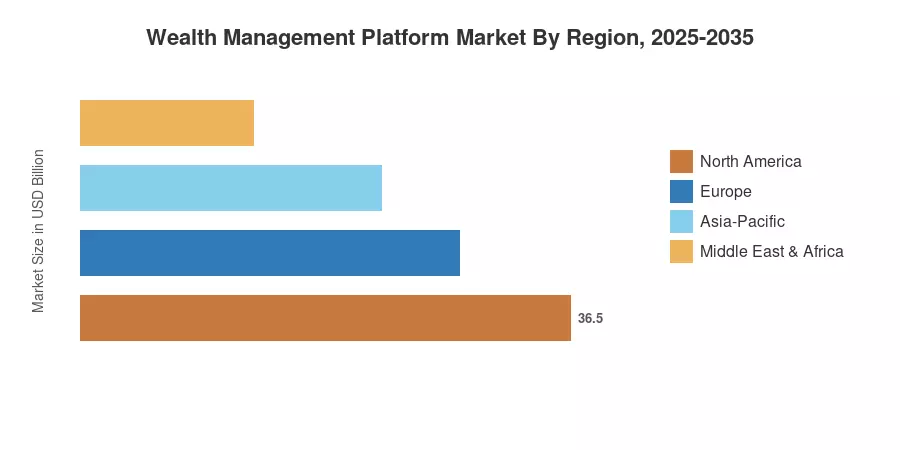

North America commands roughly 37% of the Wealth Management Platform Market, anchored by the sheer scale of U.S.-registered investment advisors and wirehouses. Asia-Pacific is the fastest-growing region at a projected 15.8% CAGR, fueled by surging high-net-worth populations in China and India. Europe holds the second-largest share at approximately 28%, where MiFID II's ongoing suitability requirements keep compliance-tech spending elevated. As generative AI copilots and embedded ESG analytics mature, the addressable investor pool will widen well beyond traditional affluent segments.

Key Report Takeaways

• By Deployment Type

- Cloud-based platforms claimed the dominant share of the Wealth Management Platform Market in 2025 at roughly 67%, driven by lower total cost of ownership and elastic scalability for mid-tier advisory firms.

- On-premise deployments retain relevance among large private banks with stringent data-residency mandates, though growth trails cloud by a wide margin.

• By End-User Industry

- Banks held the largest revenue share in the Wealth Management Platform Market in 2025, reflecting their established technology budgets and multi-channel distribution networks.

- Family offices and RIAs represent the fastest-growing end-user cohort at a 14.4% CAGR, as these firms trade legacy tools for institutional-grade analytics.

• By Region

- North America retained its leading position with the largest share of global revenue in 2025.

- Asia-Pacific is projected to advance at the fastest clip through 2035, propelled by wealth creation across China, India, and ASEAN markets.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates top-down macroeconomic wealth indicators (global HNW population, AUM growth) with bottom-up platform-license and SaaS-subscription revenue disclosed in vendor filings. Historical figures rely on verified annual reports and IT-spending surveys; forecast projections apply proprietary econometric models calibrated to a 12.7% CAGR across the 2026–2035 window.