Agricultural Microbials Market Summary

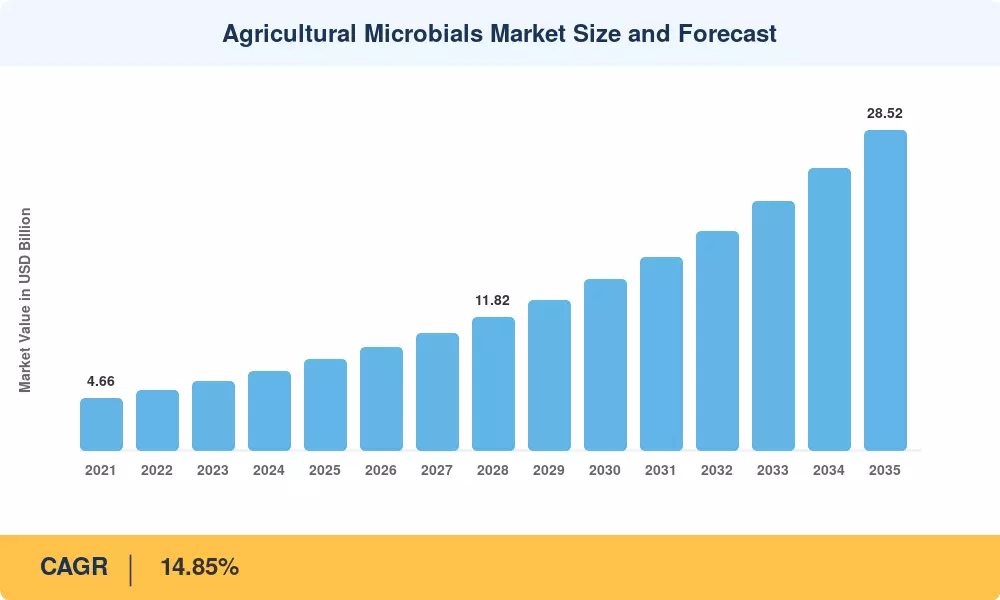

The Agricultural Microbials Market reached a valuation of USD 8.10 billion in 2025 and is projected to climb from USD 9.18 billion in 2026 to USD 28.52 billion by 2035, registering a CAGR of 14.85% across the forecast window. Two catalysts anchor this trajectory: input cost inflation for synthetic fertilizers — which spiked over 40% between 2022 and 2024 — and escalating global mandates for residue-free food production [2]. Carbon-credit programs paying USD 15–30 per metric ton of CO₂ equivalent for nitrogen reductions are turning microbial biostimulant technology adoption into a cash-positive decision for row-crop producers across the Americas [3].

The change is generational, as traditional chemical regimes of crop protection are replaced by microbial agents of biocontrol and products of beneficial soil microorganisms. AI-based strain discovery systems are cutting development times from five years to less than eighteen months, allowing vendors to rapidly refresh portfolios and stay ahead of increasing pest resistance [4]. The EU Farm to Fork objective to achieve 50% reduction of pesticides by 2030, supported by EUR 10 billion research investment under Horizon Europe, has triggered a regulatory green-lighting of plant growth boosting bacteria strains across the twenty-seven member states [5].

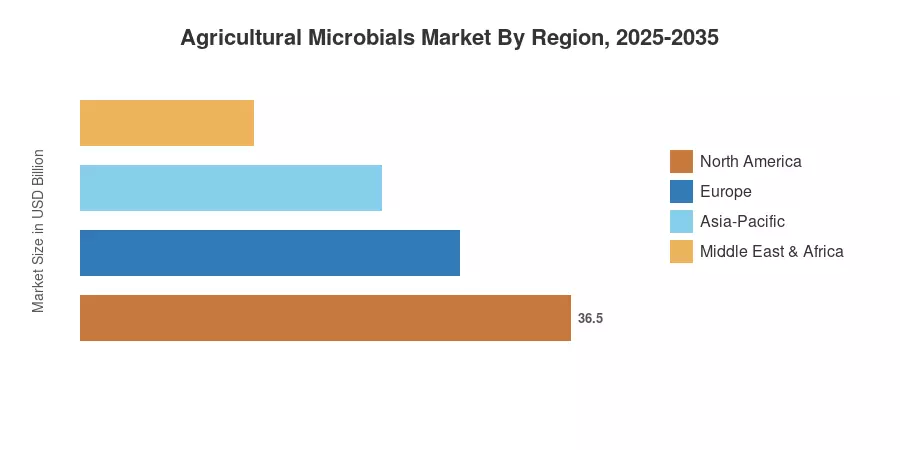

North America accounted for the largest portion of the Agricultural Microbials Market, with about 34% of 2025 revenue, due to large-acreage corn and soybean adoption. The Asia-Pacific region is the fastest-growing market with a CAGR of around 16.2%. This growth is driven by government subsidies and national targets for fertilizer reduction in India, China and Japan. Europe had the second-highest share with over 27% because of strict MRL laws and the rise of organic farming [6]. In the coming decade, mycorrhizal fungi soil health remedies and precision-applied bacterial inoculants will transform worldwide crop-input economics.

Key Report Takeaways

• By Type

- Bacteria captured roughly 46% of the Agricultural Microbials Market revenue in 2025, reflecting widespread rhizobium and Bacillus-based inoculant deployment across cereal crops

- Viruses are projected to expand at a CAGR of 19.5% through 2035, driven by rising baculovirus adoption in integrated pest management for high-value horticulture

• By Function

- Biopesticides commanded approximately 51% of the Agricultural Microbials Market share in 2025, anchored by biocontrol microbial agents targeting Lepidoptera and nematode complexes

- Biostimulants are forecast to grow at a 16.3% CAGR through 2035, as growers integrate microbial biostimulant technology into fertility programs to improve nutrient-use efficiency

• By Application

- Fruits and vegetables represented roughly 30.5% of the Agricultural Microbials Market size in 2025, fueled by residue-free export requirements in Europe and Japan

- Commercial crops are advancing at a 15.9% CAGR through 2035, as cotton and sugarcane producers adopt beneficial soil microorganism products to reduce input costs

• By Geography

- North America generated approximately USD 2.75 billion in 2025 Agricultural Microbials Market revenue

- Asia-Pacific is anticipated to register the fastest CAGR at 16.2%, supported by India's Paramparagat Krishi Vikas Yojana organic-farming subsidies and China's zero-growth fertilizer action plan

Market Size and Forecast (2021–2035)

MRFR’s sizing model triangulates bottom-up income from manufacturer shipments, distributor sell-through data and top-down cross-referencing with FAO crop-protection expenditure datasets. Historical figures (2021-2024) are audited, and the base year of 2025 is estimated. Values for 2026-2035 are based on a calibrated 14.85% CAGR with year-specific adjustments for regulatory milestones and commodity-price cycles.

.webp?v=1785504861)