Alfalfa Market Summary

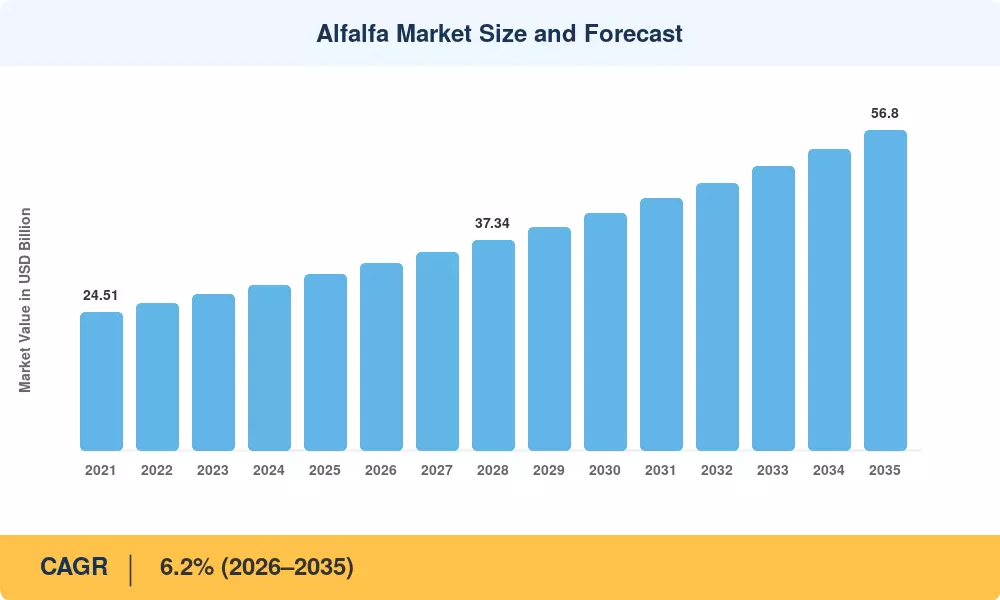

The Alfalfa Market reached USD 31.2 Billion in 2025 and is projected to climb from USD 33.1 Billion in 2026 to USD 56.8 Billion by 2035, expanding at a 6.2% CAGR through the forecast window. Two catalysts anchor this trajectory: China's USD 4.1 Billion industrial dairy expansion program under the 14th Five-Year Plan, and the USDA's USD 300 million Conservation Reserve Program incentive for legume rotations announced in 2024 [1][2]. These policy levers are reshaping how growers allocate acreage, particularly across the western U.S. and the Iberian Peninsula, where alfalfa hay forage nutrition remains central to ruminant productivity gains.

Production economics are shifting fast in the Alfalfa Market. Conventional rainfed cultivation is giving way to precision-irrigated, GPS-guided harvest systems and low-moisture baling lines that preserve alfalfa protein animal feed quality during ocean transit. BloombergNEF estimates global agritech capex tied to forage modernization crossed USD 2.8 Billion in 2024, with dehydrated alfalfa pellets emerging as the fastest-scaling export format from Spain and the United States [3]. Blockchain traceability pilots and climate-resilient genetics from Forage Genetics International are accelerating the transition.

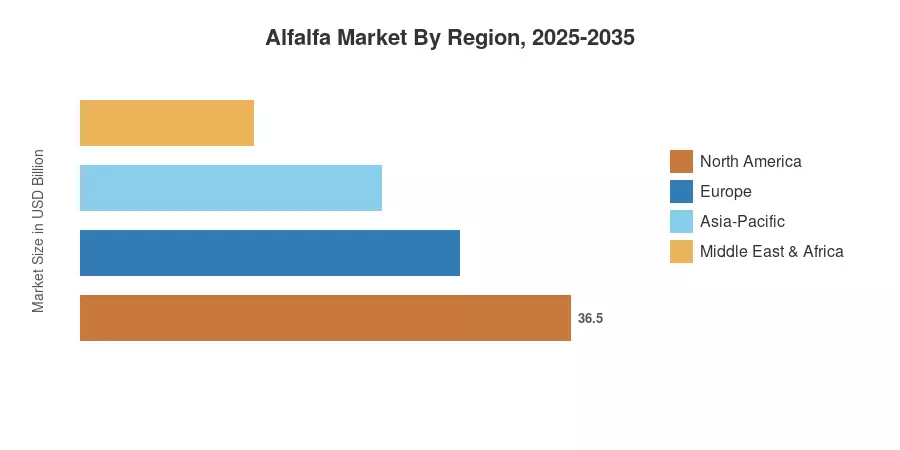

Asia-Pacific anchors the Alfalfa Market with a 32.4% share in 2025, driven by Chinese and Saudi import demand. South America, led by Argentina, is the fastest-growing region at 7.1% CAGR, while North America retains a 28.5% share as the dominant export hub. Demand-side momentum continues to favor protein-dense forage formats over the next decade.

Key Report Takeaways

• By Product Form

- Bales lead the Alfalfa Market with a 58% share in 2025, anchored by export-oriented dairy demand

- Dehydrated alfalfa pellets are the fastest-growing form at a 7.6% CAGR through 2035

- Alfalfa sprout health food applications are projected to reach USD 1.9 Billion by 2035

• By Application

- Dairy cattle feed remains the largest end use, valued at USD 18.4 Billion in 2025

- Beef cattle and feedlots are scaling at a 6.4% CAGR through the forecast window

- Equine and specialty livestock applications hold a 9% share of the Alfalfa Market

• By Region

- Asia-Pacific dominates the Alfalfa Market with USD 10.1 Billion in 2025 consumption value

- South America is the fastest-growing region at 7.1% CAGR through 2035

- Middle East & Africa holds an 11.8% share, anchored by Saudi and Emirati feedlot imports

Market Size and Forecast (2021–2035)

The figures below are calibrated against USDA FAS export data, Eurostat trade flows, and primary interviews with eight integrated forage processors. Volume conversions assume a global average of USD 280 per metric ton baled-equivalent.

.webp?v=1783339556)