Chia Seeds Market Summary

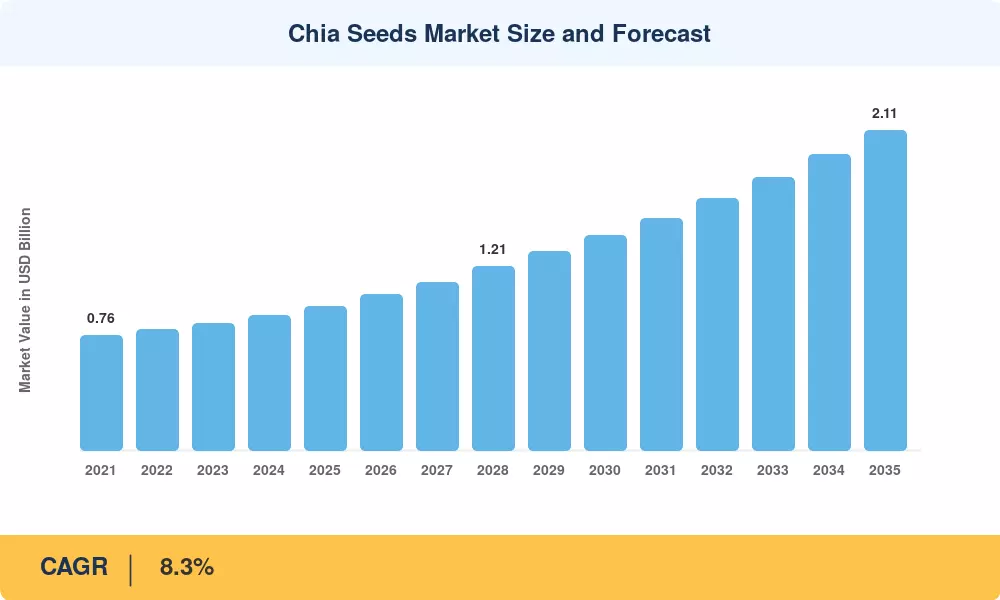

The global Chia seeds Market was valued at USD 0.95 Billion in the 2025 base year and is projected to reach USD 1.03 Billion in 2026, climbing to USD 2.11 Billion by 2035 at a compound annual growth rate of 8.3% across the forecast window. Two structural forces are accelerating demand: the U.S. Food and Drug Administration's updated qualified health claim guidance for seeds rich in alpha-linolenic acid, which lowered labeling barriers for packaged food manufacturers in late 2024, and the European Commission's allocation of EUR 240 million under Horizon Europe for sustainable protein crop research through 2027 [1]. These policy catalysts give brand owners and ingredient suppliers a clearer path to margin expansion.

On the supply side, conventional seed sourcing is giving way to precision agriculture programs in Bolivia and Paraguay, where drought-tolerant cultivar releases have pushed average yields above 1.2 metric tons per hectare — up from 0.8 metric tons just five years ago [2]. Vertical integration across farming, milling, and retail distribution has become the dominant corporate strategy, exemplified by multi-round venture funding for farm-to-shelf operators. This shift is compressing the cost structure for value-added products such as protein isolates and cold-pressed oils.

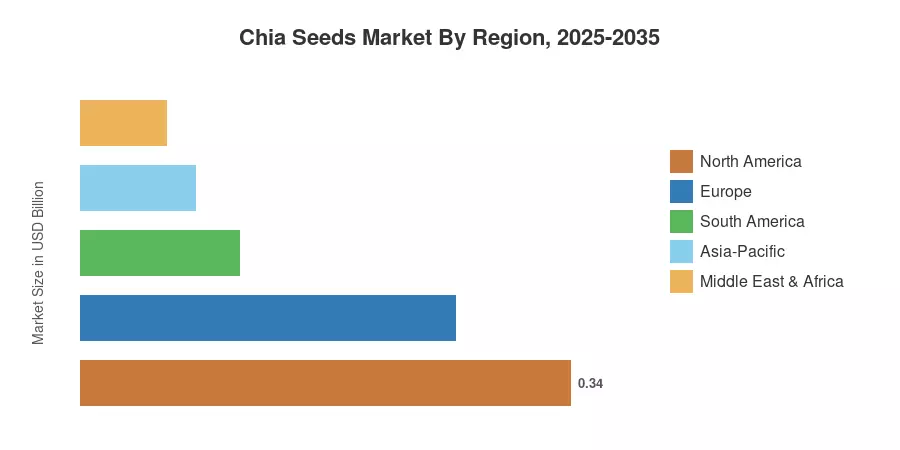

North America commands roughly 36% of the Chia seeds Market, driven by breakfast-cereal and snack-bar reformulation across the United States and Canada. Asia-Pacific represents the fastest-growing region at a projected CAGR of 8.5% through 2035, as health-conscious consumers in China, India, and Japan expand their intake of functional food imports. Europe holds the second-largest share at 27%, anchored by clean-label demand in Germany, the United Kingdom, and France. Over the next decade, convergence between nutraceutical innovation and mainstream grocery retail will continue to reshape the Chia seeds Market trajectory.

Key Report Takeaways

• By Form

- Whole seeds account for the dominant share of the Chia seeds Market, reflecting sustained bakery and beverage inclusion demand.

- Chia oil is the fastest-growing product form at a 9.6% CAGR, propelled by personal-care and nutraceutical interest.

• By Application

- Food and beverages represent 58% of global revenue, led by North American reformulation activity.

- Personal care and cosmetics applications are expanding as cold-press extraction costs decline.

• By Region

- North America held a 36% share of the Chia seeds Market in 2025, supported by retail channel saturation and FDA labeling clarity.

- Asia-Pacific is set to grow at the highest regional CAGR of 8.5%, with China and India scaling import volumes.

- South America contributed USD 0.11 Billion in 2025, reflecting its dual role as both producer and a nascent consumption hub.

Chia Seeds Market Size and Forecast (2021–2035)

Market Research Future's sizing model integrates trade-flow data from the Food and Agriculture Organization, customs-declaration volumes across 14 key import markets, and proprietary retailer sell-through estimates. Historical figures reflect audited annual reports and FAO STAT data, while the forecast applies a bottom-up volume-price methodology calibrated against primary interviews with growers, ingredient distributors, and CPG procurement teams.