Aluminum Ingots Market Summary

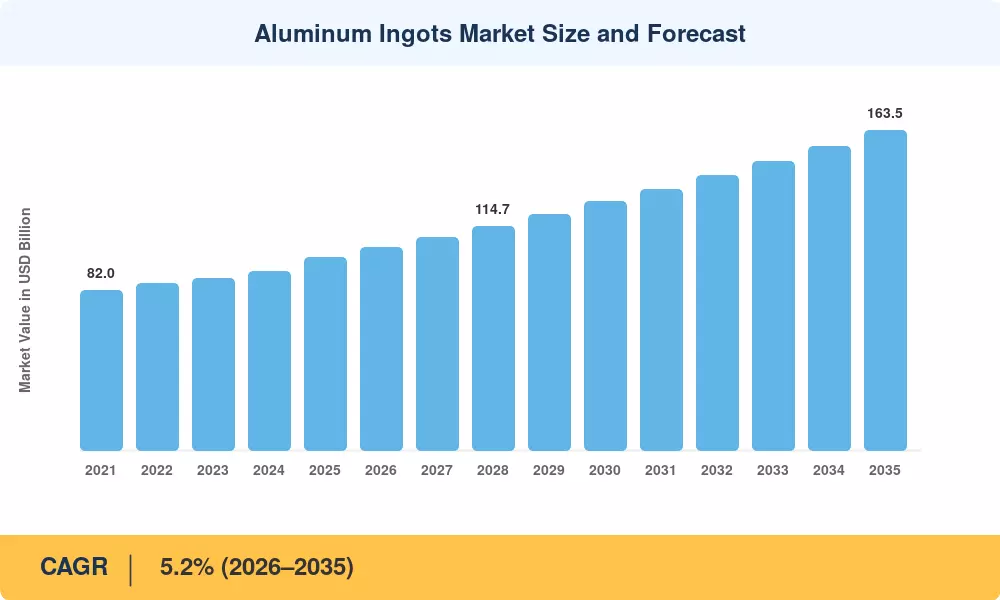

The global aluminum ingots market reached an estimated USD 98.5 billion in 2025 and is projected to grow from USD 103.6 billion in 2026 to USD 163.5 billion by 2035, registering a CAGR of 5.2% during the forecast period. This trajectory reflects accelerating demand from the automotive lightweighting revolution, where OEMs are replacing steel body panels and structural components with aluminum to comply with tightening CO₂ emission standards. The European Union's CO₂ fleet targets — mandating a 55% reduction by 2030 relative to 2021 baselines — have pushed automakers to increase per-vehicle aluminum content from roughly 180 kg to over 250 kg [1].

Across the supply chain, the aluminum ingots market is undergoing a structural shift from carbon-intensive Hall-Héroult smelting toward inert-anode and renewable-powered electrolysis. Rio Tinto and Alcoa's ELYSIS joint venture committed over USD 550 million to commercialize zero-carbon smelting technology by 2027, a move that could reshape cost curves industry-wide [2]. Governments in Canada, Norway, and Iceland have offered subsidized hydroelectric capacity to attract next-generation smelter investments, reinforcing the decarbonization push.

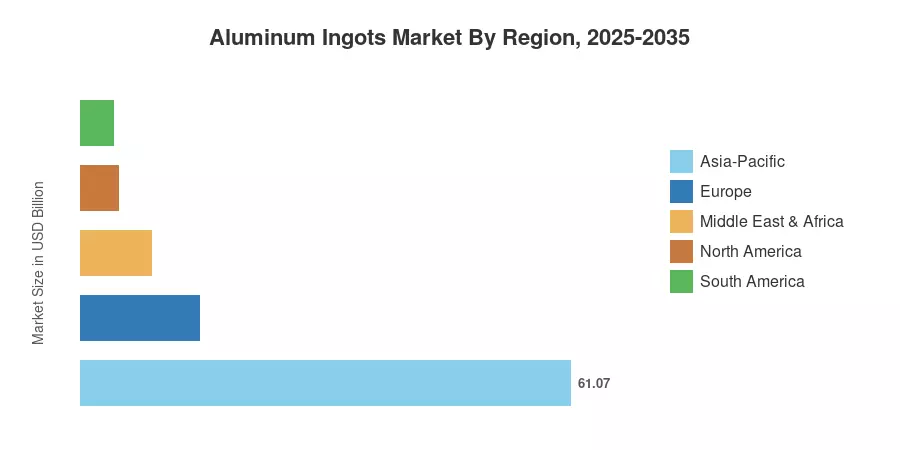

Asia-Pacific dominates the aluminum ingots market with approximately 62% of global value, driven by China's integrated smelter-foundry complexes. The region is simultaneously the fastest-growing, posting a projected CAGR of 5.8% through 2035 as India expands capacity under its National Aluminium Policy. Europe holds the second-largest share at roughly 15%, supported by the EU Carbon Border Adjustment Mechanism (CBAM), while North America accounts for about 10% on the back of reshoring initiatives. The decade ahead will reward producers that can deliver certified low-carbon ingots at scale.

Key Report Takeaways

• By Type

- Primary ingots command the largest share of the aluminum ingots market at approximately 68% of global revenue, underpinned by capacity expansions across China and the Middle East.

- Secondary (recycled) ingots represent the fastest-growing segment with a projected CAGR of 6.4%, driven by circular-economy mandates and lower energy input requirements.

• By Application

- Transportation holds approximately USD 31.2 billion in the aluminum ingots market, reflecting surging EV platform demand.

- Construction applications are expanding at a 5.5% CAGR as green-building certifications favor aluminum façade and framing systems.

- Packaging end-uses, particularly beverage cans and foil stock, maintain stable single-digit growth across mature economies.

• By Region

- Asia-Pacific leads the aluminum ingots market at 62% share, anchored by China's 40-million-tonne annual smelting capacity.

- North America is forecast to grow at a 4.8% CAGR as tariff protections and IRA incentives boost domestic smelter output.

- The Middle East & Africa region is valued at approximately USD 8.9 billion in 2025, with Gulf states leveraging low-cost energy for greenfield smelters.

Aluminum Ingots Market Size and Forecast (2021–2035)

The market size figures below draw on primary interviews with smelter operators and downstream fabricators, verified against public production data from the International Aluminium Institute (IAI) and World Bureau of Metal Statistics. Historical values (2021–2024) reflect actual trade-weighted shipment data; the base year 2025 incorporates preliminary H1 actuals and H2 estimates. Forecast values (2026–2035) apply a constant CAGR anchored to demand-side modeling across five regions and six application verticals.