Automotive Interior Material Market Summary

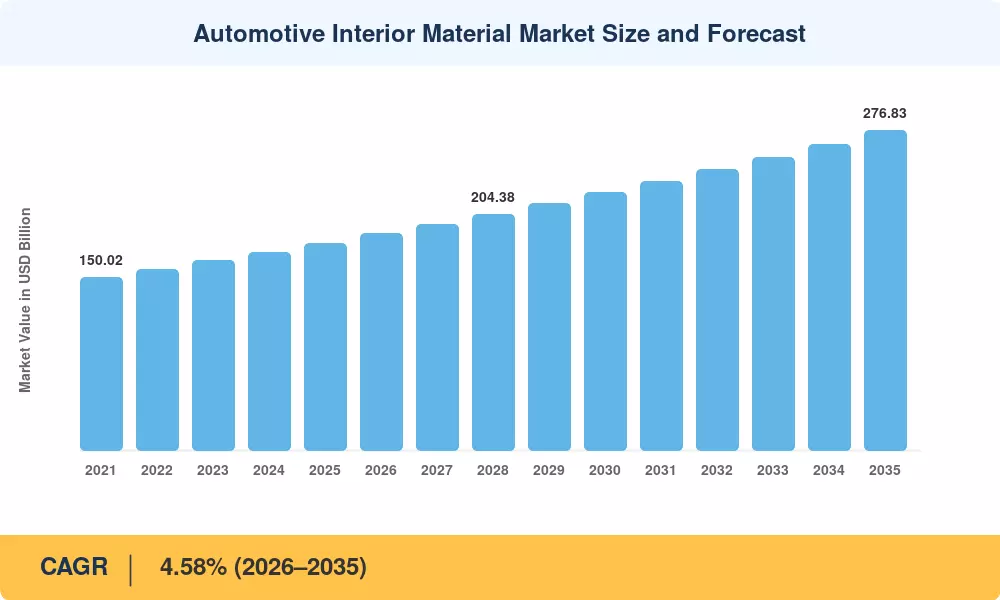

The Automotive Interior Material Market reached an estimated USD 179.46 Billion in 2025 and is projected to grow from USD 187.64 billion in 2026 to USD 276.83 billion by 2035, registering a CAGR of 4.58% during the forecast period. Two forces anchor this trajectory: tightening EU End-of-Life Vehicle regulations that mandate 25% recycled-content thresholds by 2030, and OEM capital programs exceeding USD 38 billion earmarked for cabin electrification across the top ten global automakers [2]. Together, these catalysts are reshaping procurement strategies for automotive upholstery materials, vehicle interior plastics, and dashboard materials.

A generational shift is underway inside vehicle cabins. Legacy PVC-based interior trim materials and petroleum-derived foams are giving way to bio-based polymers, recycled polyester automotive fabric materials, and chrome-free automotive leather materials. BMW's iFactory program, for instance, has committed EUR 1.2 billion to sustainable cabin sourcing through 2028, while Toyota's Bio-Plastics Initiative targets 30% plant-derived vehicle cabin materials across all new platforms by 2030 [3]. Software-defined cockpits amplify demand for lightweight automotive materials that accommodate high-density displays and centralized compute modules.

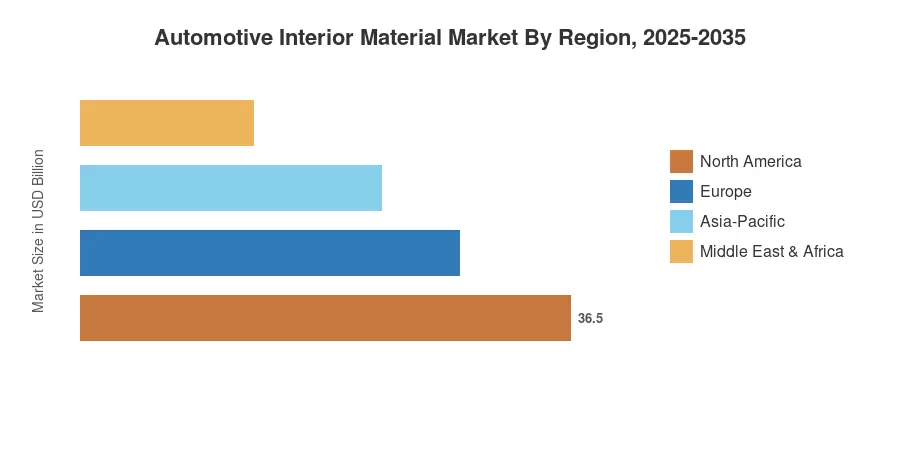

Asia-Pacific dominates the Automotive Interior Material Market with roughly 40% of global revenue, driven by China's and India's expanding passenger-car production. The region also posts the fastest CAGR at 4.72%, fueled by local innovation in automotive seating materials and cost-competitive manufacturing Europe holds about 27% share, anchored by premium OEM demand for sustainable car interior components. North America rounds out the top three, supported by reshoring incentives and growing EV-platform investment [4].

Key Report Takeaways

• By Vehicle Type

- Passenger cars captured approximately 70% of the Automotive Interior Material Market in 2025, reflecting mass-market cabin refresh cycles

- Electric passenger cars are advancing at a projected 4.62% CAGR through 2035, driven by silent cabin premiumization

• By Material Type

- Synthetic leather commanded roughly 43% revenue share in 2025 across the Automotive Interior Material Market, displacing genuine leather in mid-range vehicles

- Natural and recycled materials are forecast to post the highest segment CAGR at 4.65% as OEMs pursue ESG targets

• By Region

- Asia-Pacific led with 40% of the global Automotive Interior Material Market share in 2025

- South America and the Middle East & Africa present emerging-market upside, each growing above the global average CAGR

Market Size and Forecast (2021–2035)

MRFR market sizing is based on bottom-up supplier revenue aggregation and top-down vehicle-production volume modeling, cross-validated with OEM procurement disclosures, trade association data, and customs information from 42 countries.

.