Autonomous Ships Market Summary

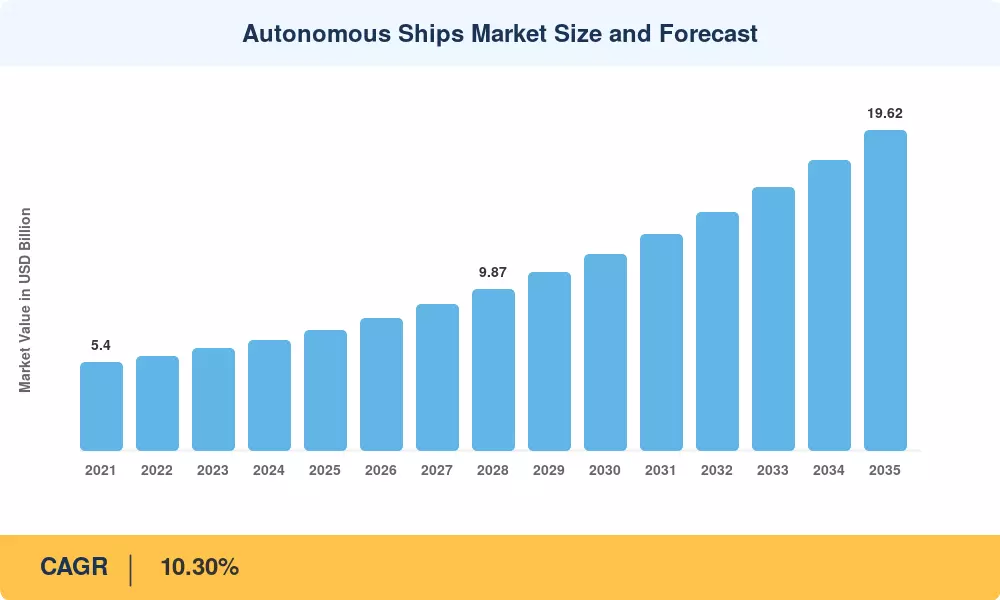

The Autonomous Ships Market was valued at USD 7.35 billion in 2025 and is projected to reach USD 8.11 billion in 2026 before climbing to USD 19.62 billion by 2035, registering a CAGR of 10.30% during the 2026–2035 forecast period. Two forces anchor this trajectory: the International Maritime Organization's (IMO) mandate to halve greenhouse-gas emissions by 2050, which is pushing fleet operators toward AI-assisted voyage optimization, and a sustained uptick in defense procurement budgets allocated to unmanned naval platforms across the Indo-Pacific theater [2]. Both catalysts translate directly into capital expenditure on autonomous navigation stacks, collision-avoidance sensors, and shore-based remote-control centers.

Integrated digital-twin platforms that combine LiDAR, high-definition cameras, and satellite-AIS inputs into a single situational-awareness layer are replacing legacy bridge equipment, such as radar consoles that depend on manual plotting, paper-based trip plans, and analog engine-room telegraphs [3]. Together, shipyards in China and South Korea have committed more than USD 2.1 billion to smart-ship construction initiatives through 2028, speeding up the pipeline for newbuilds and retrofits of autonomy-ready vessels [4].

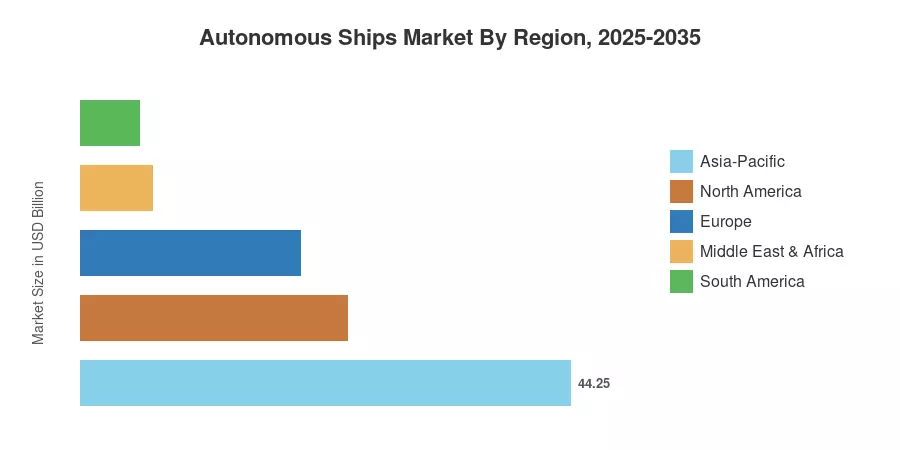

Due to concentrated shipbuilding capacity in China, Japan, and South Korea, the Asia-Pacific holds the largest share of the autonomous ships market, accounting for 44.25% of global revenue in 2025. The fastest-growing region is the Middle East and Africa, driven by maritime technology funds backed by sovereign wealth and massive port renovation projects. Europe has the second-largest stake, at about 20%, thanks to the EU's Horizon Europe maritime-autonomy research funding and Norway's regulatory leadership [5]. The rate at which classification societies complete type-approval procedures for completely autonomous ocean-going tonnage will determine the course of the next ten years.

Key Report Takeaways

• By Autonomy Level

- Partially autonomous vessels captured 76.10% of the Autonomous Ships Market in 2025, reflecting fleet operators' preference for human-supervised systems during the regulatory transition.

- Fully autonomous platforms are projected to advance at an 18.80% CAGR through 2035 as classification-society approvals expand.

• By Component

- Hardware represented the dominant component segment of the Autonomous Ships Market, while software revenues are expanding at a 14.75% CAGR through 2035.

• By Ship Type & End User

- Cargo vessels led with a 40.45% revenue share in 2025, underscoring the economic case for autonomous deep-sea freight operations.

- The government and military end-user segment is projected to register a 15.40% CAGR through 2035.

• By Region

- Asia-Pacific secured the largest regional slice of the Autonomous Ships Market in 2025.

- The Middle East & Africa region is the fastest-growing geography through 2035, expanding at a 14.10% CAGR.

Autonomous Ships Market Size and Forecast (2021–2035)

Market sizing relies on a triangulated methodology combining top-down revenue analysis of marine-equipment OEMs with bottom-up vessel-delivery and retrofit data from leading classification societies. Historical estimates (2021–2024) draw on audited annual reports, port-authority procurement records, and verified contract values, while forecasts (2026–2035) apply regression modeling calibrated against shipyard order-book pipelines and regulatory milestone timelines [6].

.webp?v=1783951664)