Autonomous Trucks Market Summary

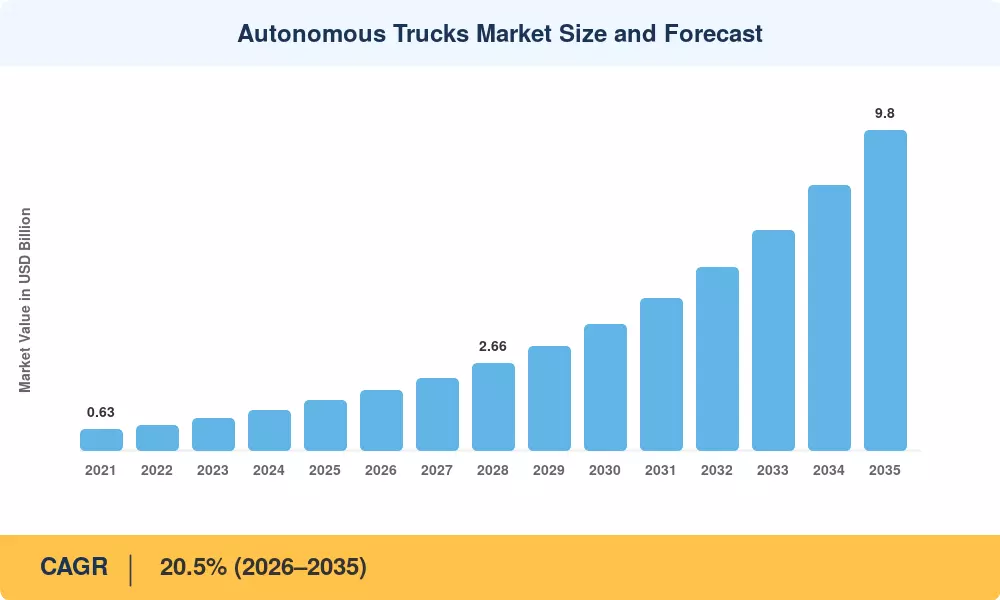

The global Autonomous Trucks Market reached an estimated USD 1.52 billion in 2025 and is projected to grow from USD 1.83 billion in 2026 to USD 9.80 billion by 2035, expanding at a CAGR of 20.5% during the forecast period (2026–2035). Two catalysts are accelerating this trajectory: the U.S. Federal Motor Carrier Safety Administration's evolving framework for automated driving system-equipped commercial vehicles and over USD 12 billion in cumulative venture and strategic investment directed at self-driving truck developers between 2020 and 2025 [1][2].

The current technological change substitutes sensor-fused autonomous stacks that combine cameras, radar, and high-resolution mapping for conventional driver-dependent long-haul operations. In Texas, Arizona, and the Sun Belt, truck manufacturers and technology partners have transitioned from controlled-track testing to continuous revenue-generating operations on designated highway corridors. A regulatory framework that did not exist five years ago is being provided by the European Commission's updated General Safety Regulation and the U.S. Department of Transportation's AV 4.0 policy framework [3][4].

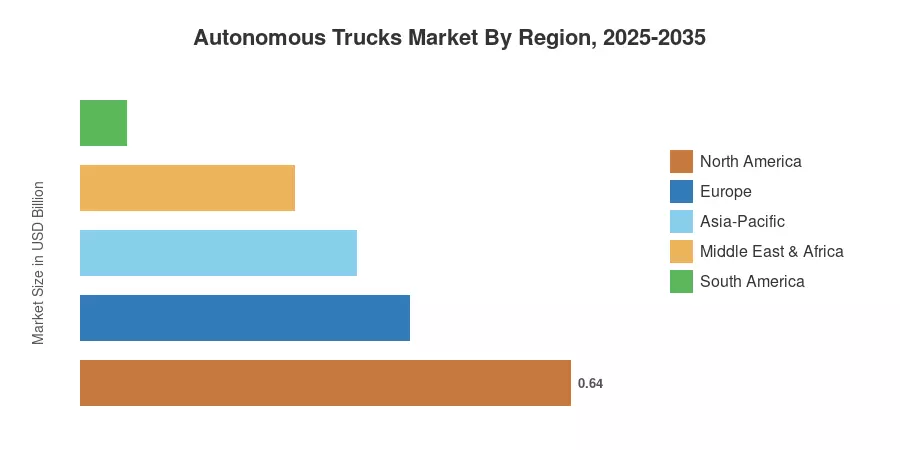

Due to favorable state-level laws and severe driver shortages, North America holds the largest part of the autonomous truck market, accounting for over 42% of global sales. With a predicted CAGR of 23.8%, Asia-Pacific is the fastest-growing area, driven by investments in smart-logistics infrastructure from China and Japan. With the help of pan-European corridor pilots and Germany's Autonomous Driving Act, Europe accounts for about 28% of the market. The market for autonomous trucks is expected to develop compoundingly through 2035 as commercialization expands beyond first-mover corridors.

Key Report Takeaways

• By Autonomy Level

- Level 4 systems dominate the Autonomous Trucks Market with approximately 58% revenue share in 2025, reflecting the hub-to-hub highway operating model favored by commercial fleets.

- Level 2/3 platforms account for an estimated USD 0.52 billion and serve as bridge technologies in mixed-fleet environments.

- Level 5 full autonomy remains pre-commercial but is projected to register the highest segment CAGR through 2035.

• By Application

- Long-haul freight and logistics represent the largest application of the Autonomous Trucks Market, capturing roughly 64% share.

- Mining and port-terminal operations together contribute approximately USD 0.31 billion in 2025 revenue.

• By Region

- North America leads the Autonomous Trucks Market with a 42% share, underpinned by corridor-specific state permits.

- Asia-Pacific is expanding at a CAGR of 23.8%, driven by government-backed logistics modernization.

- Europe's share stands at 28%, with Germany and the Netherlands leading regulatory adoption.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model triangulates top-down macro freight expenditure data with bottom-up autonomous unit deployments, validated against disclosed OEM and technology-developer revenues. Historical figures (2021–2024) reflect actual commercial operations and pilot-program revenues; base-year 2025 incorporates preliminary deployment data; forecast years (2026–2035) apply a compound growth function calibrated to fleet adoption curves and regulatory expansion timelines.