Freight and Logistics Market Summary

The Freight and Logistics Market stood at USD 6.81 trillion in 2025 and is projected to reach USD 7.17 trillion by 2026 before climbing to USD 11.39 trillion by 2035 at a 5.28% CAGR during the 2026–2035 forecast window. Two structural catalysts underpin this trajectory: first, global merchandise trade volumes have rebounded past pre-pandemic peaks, with the WTO estimating a 3.3% annual expansion in goods trade through the late 2020s [1]; second, governments across Asia and the Middle East are channeling over USD 1.4 trillion into port, highway, and rail corridor investments during the current decade, creating fresh capacity that pulls freight volumes upward [2].

Technology is altering the cost equation in the Freight & Logistics Market. Autonomous yard-management systems, real-time visibility platforms and AI-driven demand sensing are replacing human warehouse picking and legacy paper-based customs clearance. forecasts that the digitization of logistics operations can lower total landing costs by 15–25% . The EU’s new Combined Transport Directive, which extends intermodal shift incentives through 2030 [4], is further bolstering that policy push.

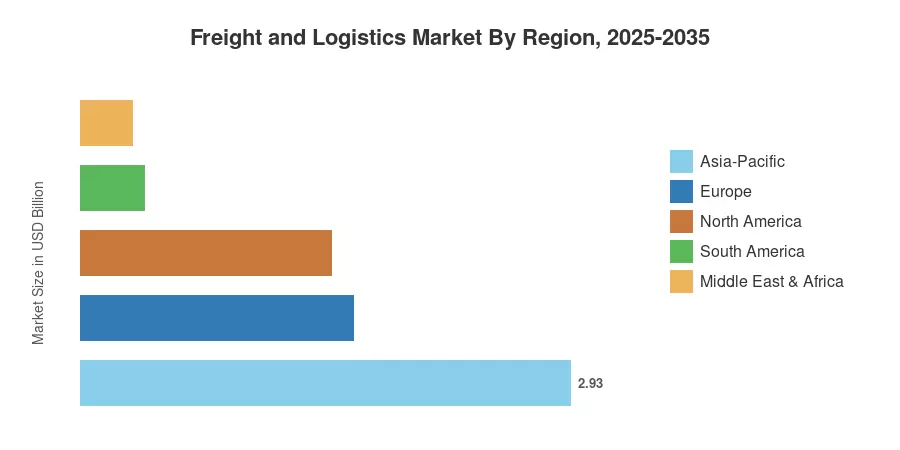

Asia-Pacific holds almost 43% of the Freight and Logistics Market share, owing to the Belt and Road corridors of China and the Gati Shakti infrastructure scheme of India. The region registers a CAGR of 5.92%, which is the fastest. Europe is second at 24%, supported by intra-EU trade density. North America is at 22% buoyed by nearshoring tailwinds changing U.S.-Mexico freight lines. The next decade will depend on how fast operators can transform capital-intensive physical networks into platform-orchestrated, data-rich ecosystems.

Key Report Takeaways

• By Logistics Function

- Freight Transport accounted for 56.8% of the Freight and Logistics Market in 2025, reflecting the dominant share of line-haul road, rail, and ocean movements.

- Freight Forwarding is on track to record a 5.58% CAGR through 2035 as cross-border complexity drives demand for intermediary coordination.

- Warehousing and Storage reached USD 680 billion in 2025, fueled by e-commerce fulfillment center expansion.

• By End User Industry

- Wholesale and Retail Trade captured 30.8% of the Freight and Logistics Market in 2025, reflecting omnichannel supply chain investment.

- Manufacturing is projected to grow at a 5.55% CAGR as reshoring and regionalization increase inbound raw-material flows.

• By Geography

- Asia-Pacific leads the Freight and Logistics Market at an estimated 43% share, backed by sustained infrastructure spending across China, India, and ASEAN.

- North America contributes roughly USD 1.50 trillion in 2025, with nearshoring driving cross-border volumes along the U.S.–Mexico corridor.

Freight and Logistics Market Size and Forecast (2021–2035)

Market Research Future (MRFR) projections are based on personal interviews with 350+ freight operators, forwarders and shippers and secondary research from national statistics bureaus, trade associations & regulatory filings. Historical statistics (2021-2024) are actuals; 2025 is the calibrated base year; 2026-2035 values are using a constant CAGR model that was validated against bottom-up segment estimates.