Ayurveda Market Summary

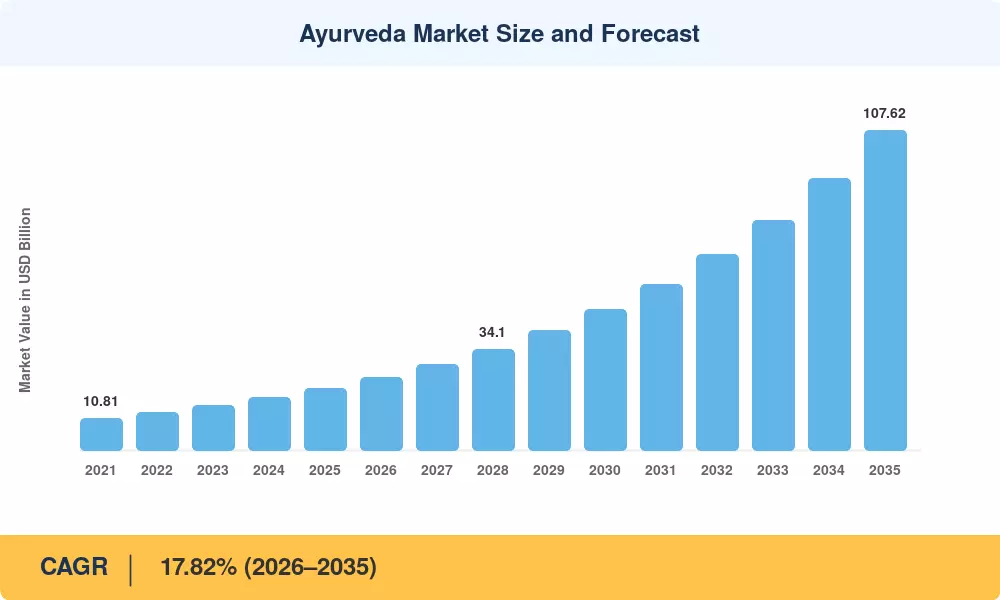

The Ayurveda Market stood at an estimated USD 20.84 billion in 2025 and is projected to reach USD 24.55 billion in 2026 before climbing to USD 107.62 billion by 2035, registering a CAGR of 17.82% during the forecast period (2026–2035). This rapid expansion is anchored in two converging forces: India's National AYUSH Mission, which has channeled over USD 580 million into traditional Indian healing infrastructure since 2020, and a global consumer pivot toward plant-based wellness that has made herbal medicine formulations a mainstream pharmacy category across Western Europe and North America[2].

The Ayurveda Market is undergoing a shift from unbranded, loosely controlled cottage manufacture to GMP-certified, clinically verified product lines. The local practitioners selling legacy formulas are being replaced by standardized dosha-based therapy regimens backed by randomized clinical trials. Mankind Pharma’s acquisition of Upakarma Ayurveda in 2022 was a statement that multinational pharma corporations now saw Ayurvedic dietary practices as a legitimate growth vertical worth deploying significant capital on [3][4].

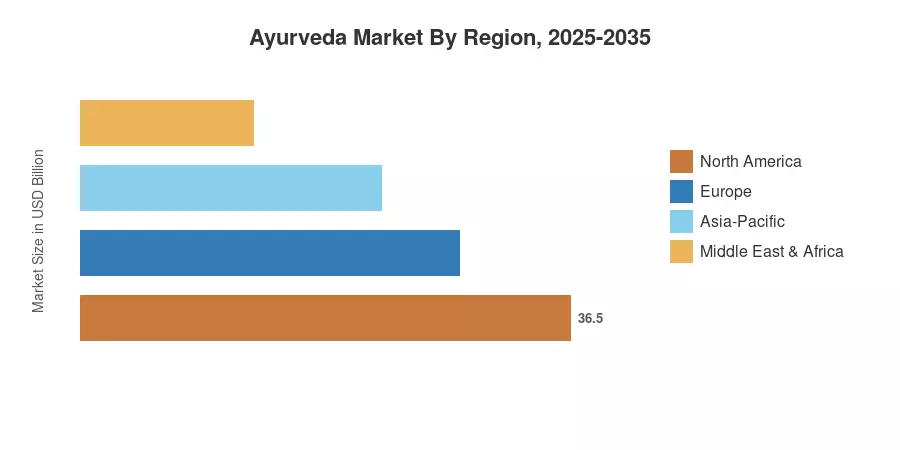

The Asia-Pacific region accounts for over 44% of the worldwide Ayurveda market revenue, which is attributed to India's deep-rooted cultural history and manufacturing capabilities. North America is the fastest-growing market with a CAGR of over 20 percent, driven by growing interest in panchakarma detox therapy among wellness-conscious customers. Europe has over 22% - the next largest - buoyed by the developing regulatory route of traditional herbal registrations in the EU. Bolstered by an expanding body of therapeutic data and digital commerce facilitating increased access, the Ayurveda Market is poised for sustained double-digit expansion through 2035 [5][6].

Key Report Takeaways

• By Form

- The Herbal segment accounts for the largest share of the Ayurveda Market, representing roughly 52% of 2025 revenue, driven by consumer preference for plant-derived herbal medicine formulations with transparent ingredient lists

- Herbomineral preparations are growing at a CAGR of approximately 19.4% through 2035, reflecting clinician interest in synergistic mineral-herb compounds for chronic disease management

- Mineral-based formulations contributed an estimated USD 2.71 billion in 2025, underpinned by demand for Bhasma-based traditional Indian healing products in South Asian markets

• By Application

- Medicinal applications dominate the Ayurveda Market, holding nearly 61% share in 2025, as dosha-based treatment protocols gain traction in integrative medicine clinics

- Personal care Ayurvedic products are expanding at a CAGR of approximately 18.9%, fueled by clean-beauty trends and rising consumer adoption of Ayurvedic dietary practices in skincare

• By Region

- Asia-Pacific leads the Ayurveda Market with a 44% revenue share, anchored by India's production ecosystem and government subsidies for AYUSH practitioners

- North America's CAGR of 20.3% makes it the fastest-growing region, as panchakarma detox therapy centers proliferate in metropolitan wellness hubs

- Europe holds a 22% share, supported by the EU's Traditional Herbal Medicinal Products Directive enabling standardized registrations

Market Size and Forecast (2021–2035)

MRFR's market sizing combines bottom-up revenue analysis from manufacturer filings, customs trade databases, and practitioner surveys, triangulated with top-down macroeconomic indicators including healthcare expenditure ratios and herbal supplement retail audits across 42 countries. All historical figures reflect actual market performance; forecast values apply the calibrated 17.82% CAGR uniformly.

.webp?v=1783335236)