Bakery Products Market Summary

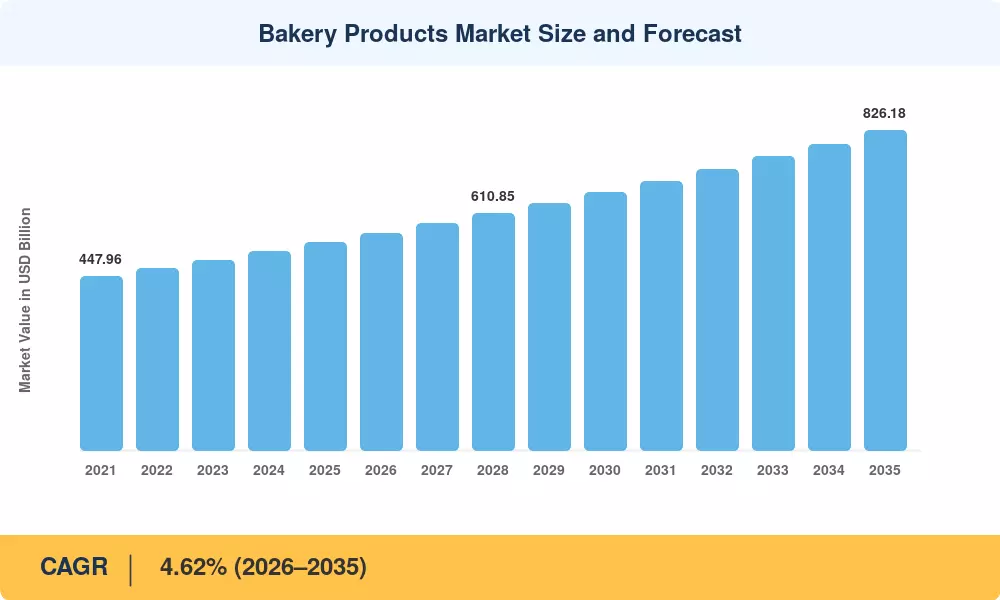

The global Bakery Products Market reached an estimated USD 536.70 billion in 2025 and is projected to expand from USD 561.48 billion in 2026 to USD 826.18 billion by 2035, registering a CAGR of 4.62% during the forecast period. Rising per-capita consumption of convenience food in urban centers and supportive food-safety regulations across the EU and North America are fueling this trajectory. Government-backed fortification mandates — such as India's FSSAI requirement for iron and folic acid in bread flour — have widened the addressable demand for staple bakery goods in populous emerging economies [2].

The Bakery Products Market is changing fast with the ongoing spread of COVID-19. Legacy batch-mixing lines are being replaced by continuous-process systems that feature vision-based quality inspection and AI-driven dough rheology controls. In 2024, the global bakery automation capital expenditure exceeded USD 4.8 billion, as manufacturers rush to fill the labor gap while preserving the artisan bread bakery trend that affects over 30% of premium SKUs in Western retail today. Robotic mini bakeries inside supermarkets are a leading example of this hybridization of automation and freshness.

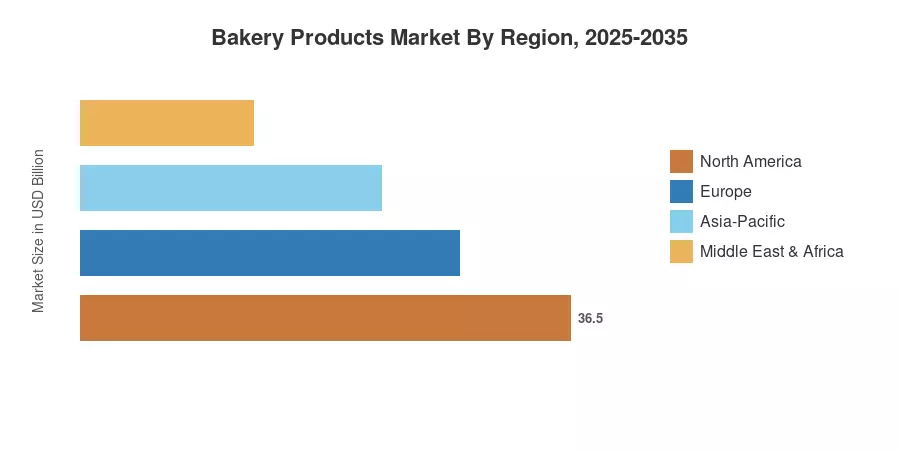

Europe held a share of around 35.1% in the Bakery Products Market in 2025, backed by entrenched bread culture in Germany, France, and Italy. Asia-Pacific is anticipated to be the fastest expanding region, at a CAGR of 6.08% through 2035, owing to increased urbanization and adoption of Western diets in China and India. North America accounted for the second-largest share of nearly 26.4%, supported by high demand for gluten-free bakery goods and clean-label bakery ingredients Frozen bakery, convenience food and e-commerce channels will certainly change the competitive landscape across all regions in the coming decade.

Key Report Takeaways

• By Product Type

- Bread accounted for approximately 48.1% of Bakery Products Market revenue in 2025, reflecting its universal role as a dietary staple reinforced by clean-label bakery ingredients reformulations

- Morning goods registered the fastest segment CAGR at 5.96% through 2035, driven by on-the-go breakfast culture and bakery product innovation in portion-controlled formats

- Cakes and pastries generated an estimated USD 121.5 billion in 2025, supported by premiumization and seasonal gifting demand

• By Distribution Channel

- Supermarkets and hypermarkets held roughly 50.2% of the Bakery Products Market share in 2025, leveraging in-store bakery sections and private-label expansion

- Online retail channels are growing at a 6.52% CAGR to 2035, with frozen bakery convenience food subscription models accelerating digital penetration

• By Form

- Fresh bakery items commanded about 76.6% share of the Bakery Products Market in 2025, though frozen goods are advancing at a 7.01% CAGR as cold-chain infrastructure improves globally

• By Geography

- Europe captured the largest regional share in the Bakery Products Market in 2025, while Asia-Pacific shows the strongest upside with a 6.08% CAGR to 2035

Bakery Products Market Size and Forecast (2021–2035)

MRFR's proprietary sizing model blends top-down macroeconomic indicators (GDP per capita, urbanization rate, food CPI) with bottom-up production and trade-flow data sourced from Euromonitor, FAO, and national statistics bureaus. Historical figures reflect actual reported revenues; forecast values apply a calibrated CAGR with annual adjustments for anticipated regulatory and macroeconomic shifts.

.webp?v=1783339557)