Centrifugal Pump Market Summary

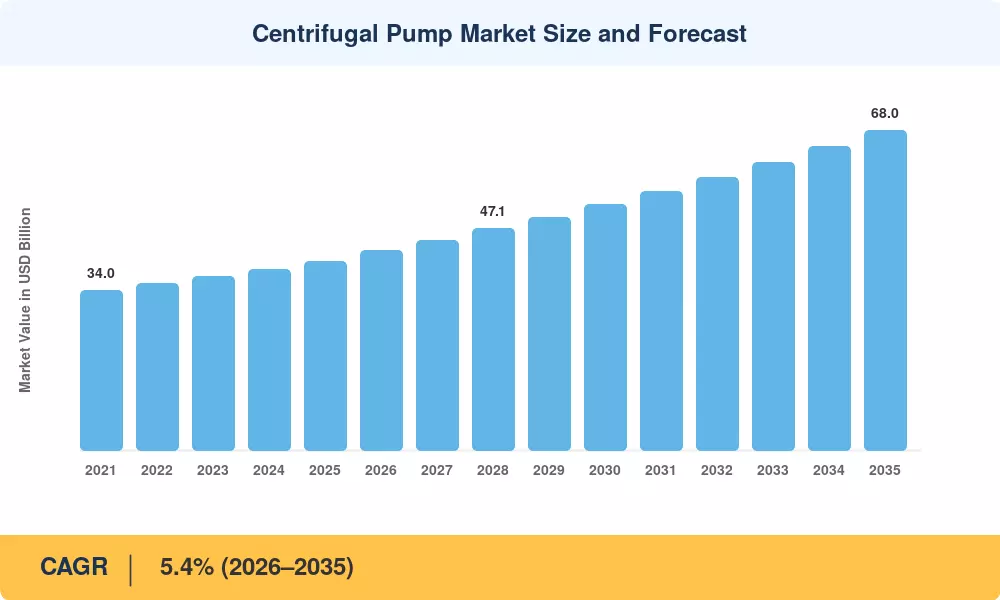

The Centrifugal Pump Market reached an estimated USD 40.2 billion in 2025 and is projected to climb from USD 42.4 billion in 2026 to USD 68.0 billion by 2035, registering a CAGR of 5.4% across the forecast window. Two forces are converging to sustain this trajectory: the global push to modernize aging water infrastructure — the U.S. EPA alone allocated over USD 12 billion in revolving-fund commitments for drinking-water and wastewater upgrades in fiscal 2024 [1] — and the accelerating buildout of oil-and-gas midstream capacity across the Middle East and Asia-Pacific, where national energy companies committed more than USD 180 billion in upstream capital expenditure during 2024 [2].

Technology is reshaping how centrifugal pumps are specified, operated, and maintained. Legacy fixed-speed motors are giving way to variable-frequency-drive (VFD) integration that cuts energy consumption by 20–40%, while IoT-enabled condition monitoring lets operators shift from calendar-based to predictive maintenance cycles. The European Commission's Ecodesign Regulation 2024/1516 has effectively mandated minimum efficiency standards for industrial pumps above 0.75 kW, accelerating the replacement of older units with high-efficiency designs across EU member states [3].

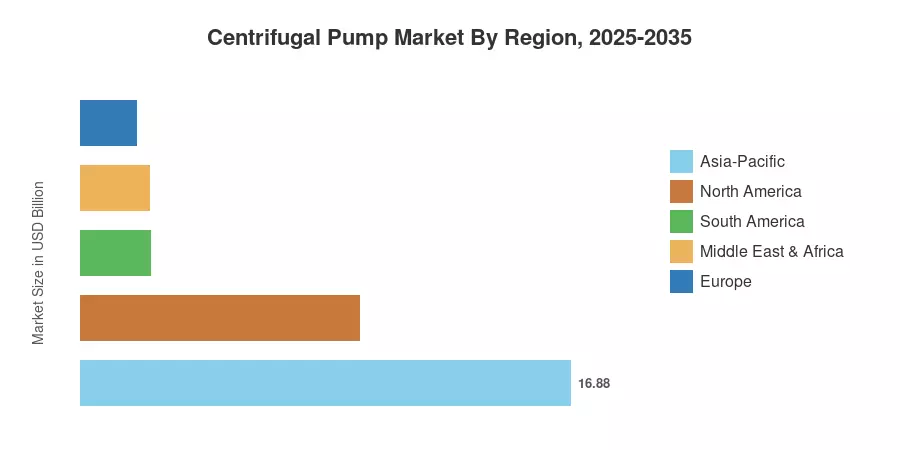

Asia-Pacific dominates the Centrifugal Pump Market with a 42% revenue share, driven by massive infrastructure buildouts in China and India. The region also leads as the fastest-growing geography, posting a projected CAGR of 6.2% through 2035. North America holds the second-largest share at 24%, underpinned by shale-sector demand and municipal water-system overhauls. Europe accounts for 22% of global revenue, with Germany's chemical processing corridor and the UK's water-utility renewal programs providing steady demand. As urbanization rates in Southeast Asia and Sub-Saharan Africa climb toward 60% by 2035, the next decade promises broad-based demand expansion [4].

Key Report Takeaways

• By Stage

- Single-stage pumps command approximately 62% of the Centrifugal Pump Market revenue share, reflecting widespread adoption in municipal water supply and irrigation.

- Multi-stage configurations are projected to grow at a CAGR of 6.8%, the fastest among product types, propelled by high-head applications in power generation and desalination.

• By Pump Design

- Axial and mixed-flow designs account for an estimated USD 3.2 billion in 2025 revenue, serving large-volume drainage and flood-control installations.

• By End User

- Oil and gas remains the largest end-user vertical with roughly 28% of the Centrifugal Pump Market, driven by upstream production and pipeline transfer requirements.

- Water and wastewater treatment is expanding at an estimated CAGR of 6.1%, fueled by regulatory mandates and population growth.

- Power-generation applications represent approximately USD 6.4 billion in 2025 base-year value.

• By Region

- Asia-Pacific holds 42% of the global Centrifugal Pump Market and leads regional growth.

- North America is valued at approximately USD 9.6 billion in 2025.

- Middle East & Africa is forecast to register a CAGR of 5.9%, driven by desalination mega-projects.

Centrifugal Pump Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining bottom-up equipment-shipment data from pump OEMs, top-down macroeconomic modeling of end-user capital expenditure, and validation through primary interviews with procurement managers across key verticals. Historical figures reflect actual trade and production data; forecast values apply the 5.4% compound growth rate anchored to verified demand catalysts.