Cheese Powder Market Summary

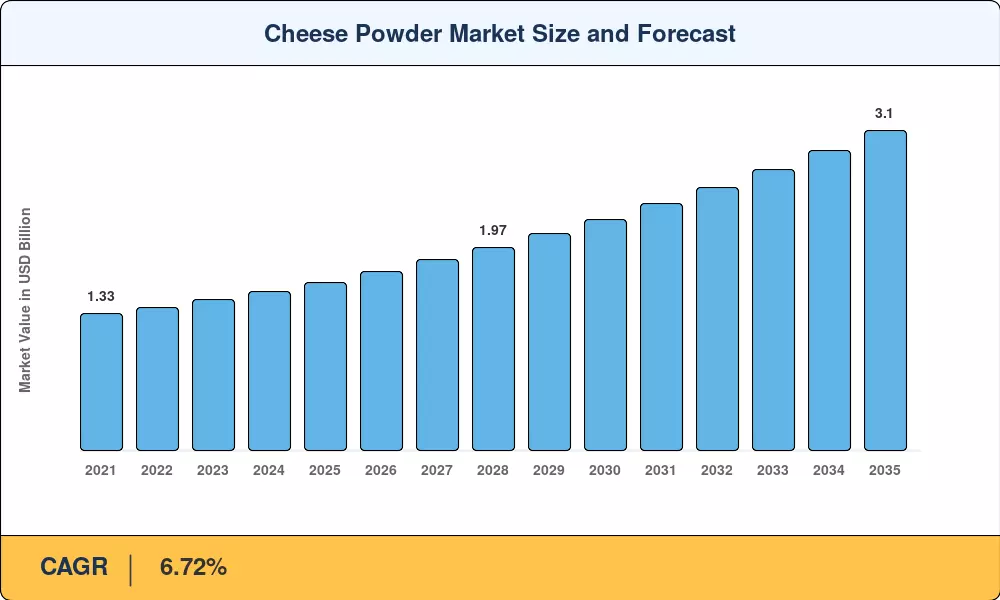

The global Cheese Powder Market reached USD 1.63 billion in 2025 and is projected to grow from USD 1.73 billion in 2026 to USD 3.10 billion by 2035, registering a CAGR of 6.72% over the forecast period (2026–2035). Rising demand from quick-service restaurant chains seeking shelf-stable, cost-effective flavor ingredients has been a critical catalyst, alongside tightening cold-chain economics that make powdered dairy formats increasingly attractive. Government-backed dairy processing modernization programs in India and Brazil have also channeled fresh capital into spray-drying infrastructure [1].

Technological evolution is reshaping how the Cheese Powder Market operates. Legacy drum-drying methods — long the industry standard — are giving way to pulse and electrostatic spray-drying systems that preserve delicate sulfur volatiles in aged-cheese varieties. A 2024 USDA Dairy Innovation Grant worth USD 48 million specifically earmarked pilot-scale electrostatic drying facilities across three U.S. states, signaling public-sector confidence in next-generation processing [2].

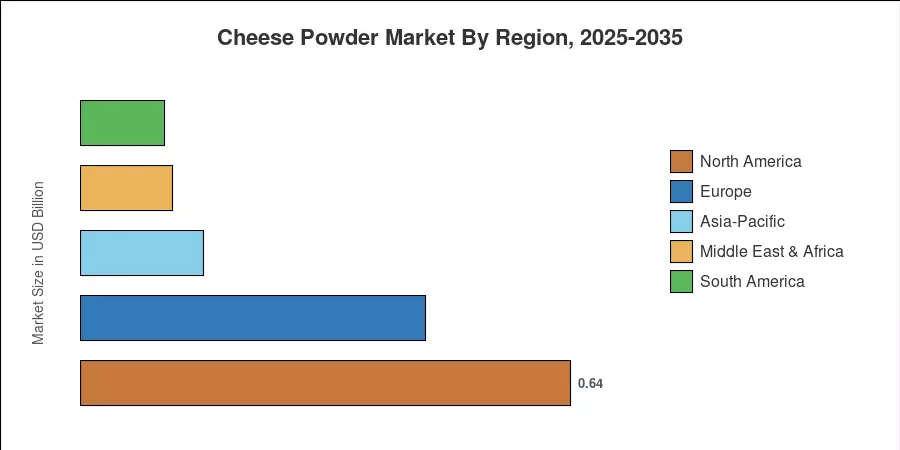

North America commands roughly 39.2% of the Cheese Powder Market, anchored by decades of snack-seasoning demand in the United States. Asia-Pacific stands as the fastest-growing region with a projected CAGR of 9.6%, fueled by multinational foodservice expansion into secondary and tertiary cities across India, China, and ASEAN nations. Europe holds the second-largest share at approximately 27.5%, driven by clean-label reformulation trends among Western European food processors. The next decade will likely see capacity additions across emerging regions narrow the gap with established markets.

Key Report Takeaways — Cheese Powder Market

By Product Type

- Cheddar accounted for approximately 34.0% of the Cheese Powder Market in 2025, supported by its dominant presence in snack seasonings and ready-meal bases.

- Mozzarella is forecast to expand at the fastest pace through 2035, riding demand from frozen-pizza and foodservice pizza chains scaling across the Asia-Pacific.

- Blue cheese powder is emerging as a premium niche, with specialty food processors paying 2.5–3× the price of standard cheddar powder.

By Application

- HoReCa/Foodservice captured roughly 56.3% of the Cheese Powder Market revenue in 2025, as chains prioritize labor savings and consistent flavor profiles.

- Food processing is projected to register a CAGR of 8.5% through 2035, led by bakery, soups, sauces, and ready-meal categories.

By Region

- North America retained the largest share of the Cheese Powder Market in 2025, accounting for an estimated 39.2% of global revenue.

- Asia-Pacific is positioned as the fastest-growing region, with a forecast CAGR of 9.6% during 2026–2035.

Cheese Powder Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines bottom-up revenue aggregation from manufacturer disclosures, trade-flow analysis from FAO and USDA databases, and proprietary demand modeling validated against downstream consumption patterns across foodservice and retail channels.