Cheese Market Summary

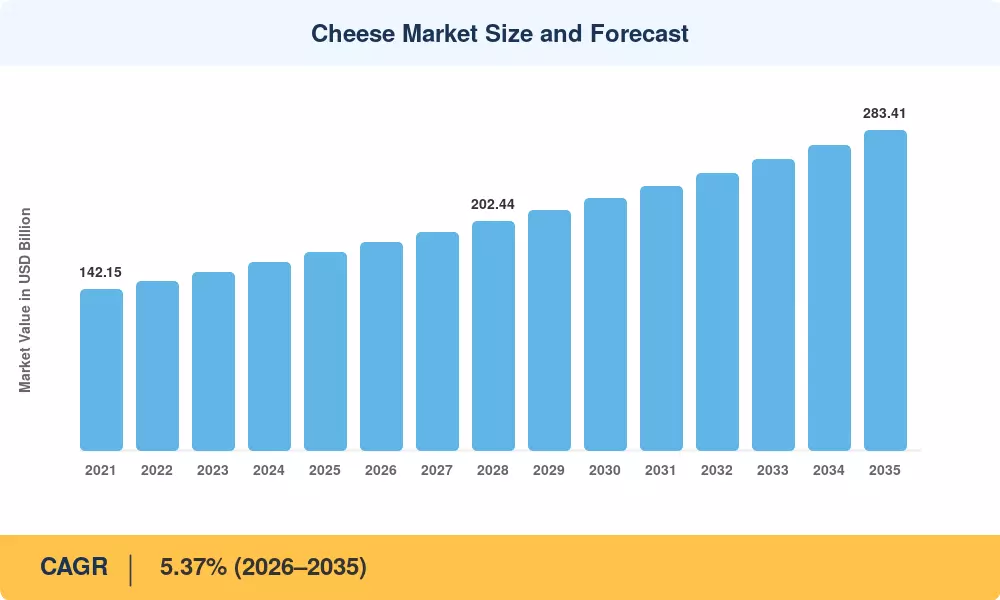

The global Cheese Market stood at USD 175.26 billion in 2025 and is projected to reach USD 182.50 billion in 2026 before climbing to USD 283.41 billion by 2035, advancing at a CAGR of 5.37% during the forecast period. This expansion reflects the convergence of rising protein-conscious diets across developing economies and aggressive retail modernization programs — the EU's Farm to Fork Strategy alone has earmarked over €10 billion in agri-food supply chain upgrades through 2030, strengthening cold-chain infrastructure that directly benefits cheese distribution [2]. Robust urbanization and increasing disposable incomes, particularly across Southeast Asia and Sub-Saharan Africa, continue to pull cheese consumption beyond traditional Western cooking applications into on-the-go snacking, premium entertaining, and convenience-driven foodservice menus.

Technological transformation is reshaping every link of the cheese value chain. Legacy batch-pasteurization and manual aging cellars are giving way to precision fermentation monitoring, IoT-enabled ripening chambers, and automated brine management systems. Dairy cooperatives in the Netherlands invested an estimated €1.4 billion in carbon-neutral processing infrastructure between 2022 and 2024, while U.S. specialty artisan cheese producers have adopted blockchain-based provenance tracking to satisfy growing consumer demand for transparency [3]. Plant-based cheese alternative formulations — leveraging cashew, oat, and precision-fermented casein — now represent the fastest-innovating R&D corridor, with venture capital backing exceeding USD 800 million globally in 2024 alone [4].

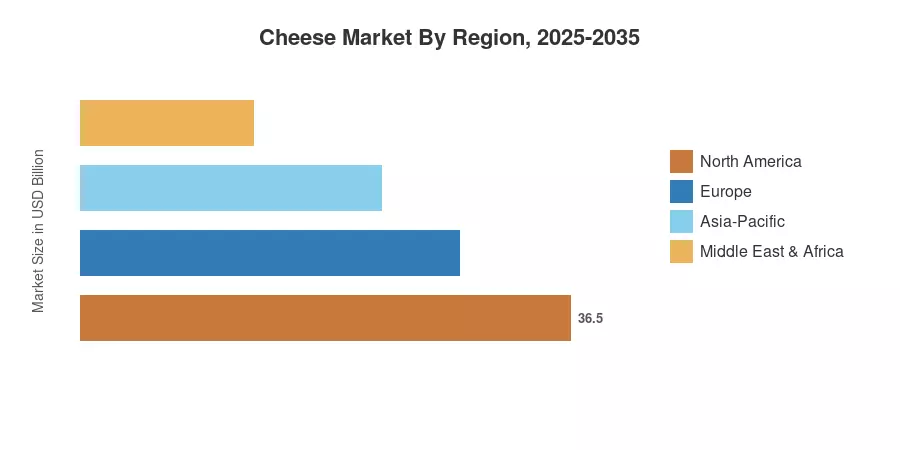

Europe commands the largest revenue share of the Cheese Market at roughly 29% of global value, anchored by France, Germany, and Italy's deeply embedded cheese consumption traditions. Asia-Pacific is the fastest-growing region at a CAGR exceeding 7.4%, powered by China's dairy expansion policies and India's rapidly scaling organized retail sector. North America holds the second-largest share at approximately 26%, driven by strong mozzarella processed cheese demand in QSR foodservice and rising natural aged cheddar cheese premiumization across retail channels The decade ahead will reward players who balance scale efficiencies with authentic provenance narratives and sustainability credentials.

Key Report Takeaways

• By Product Type

- Natural cheese captured approximately 77% of the Cheese Market in 2025, reflecting enduring consumer preference for natural aged cheddar cheese, Gouda, and Parmesan varieties

- Mozzarella processed cheese and other processed formats are forecast to grow at a 5.65% CAGR through 2035, driven by expanding QSR chains and convenience-oriented retail packaging

• By Milk Source

- Cow milk contributed over 56% of the Cheese Market value in 2025, reinforced by established dairy farming infrastructure in Europe and North America

- Goat milk cheese is poised to advance at a 6.82% CAGR to 2035, supported by lactose-sensitivity awareness and specialty artisan cheese positioning

• By Distribution Channel

- Retail held roughly 67% of the Cheese Market share in 2025, with hypermarkets and e-grocery platforms accelerating penetration

- Foodservice is rising at a 6.05% CAGR through 2035 as cheese consumption trends shift toward experiential dining and pizza-chain expansion globally

• By Region

- Europe led Cheese Market revenue in 2025 with a 29% share, while Asia-Pacific is expanding at the highest regional CAGR of 7.4%

- North America's Cheese Market accounted for approximately USD 45.57 billion in 2025, underpinned by strong per-capita consumption rates

Cheese Market Size and Forecast (2021–2035)

MRFR's market sizing integrates a triangulated methodology: bottom-up revenue aggregation from dairy cooperative filings, top-down calibration against FAO/OECD dairy production databases, and cross-validation with proprietary trade-flow models covering 42 countries. Historical figures (2021–2024) are actuals derived from audited company reports and customs data; the base year (2025) blends preliminary actuals with econometric adjustments; forecast years (2026–2035) apply segment-specific growth curves anchored to macroeconomic and demographic inputs[5].