Collagen Supplements Market Summary

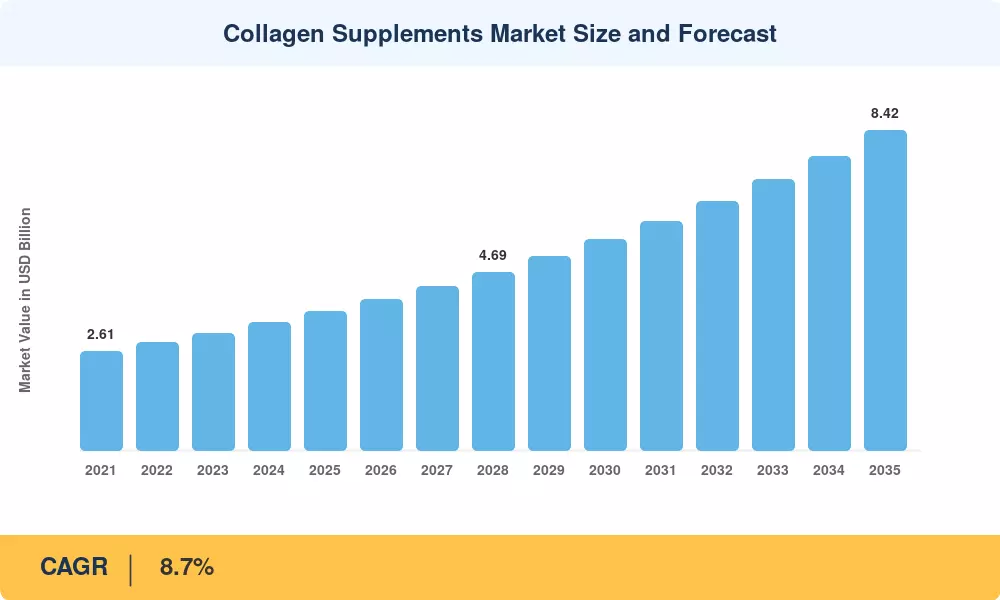

The Collagen Supplements Market is entering a decade-long expansion phase, with the Collagen Supplements Market valued at USD 3.65 billion in 2025 and projected to reach approximately USD 3.97 billion in 2026, before climbing to USD 8.42 billion by 2035 at a CAGR of 8.7% across the 2026–2035 forecast window. Two catalysts anchor this trajectory: rising healthcare expenditure on preventive nutrition — the U.S. Bureau of Economic Analysis tracked a 7.2% jump in supplement category spend in 2024 — and the EU Food Supplements Directive 2002/46/EC harmonization updates that have broadened cross-border product approvals for hydrolyzed collagen peptide powder formats.

Production economics are being rewritten by precision fermentation and tripeptide extraction. Legacy hide-and-bone rendering lines are giving way to microbial-derived recombinant Type I and Type III collagen, with venture investors directing more than USD 1.4 billion into fermentation-based ingredient platforms between 2022 and 2024. Marine collagen skin health applications now command premium shelf positions in beauty-from-within aisles, while bovine collagen joint support remains the volume backbone of the Collagen Supplements Market.

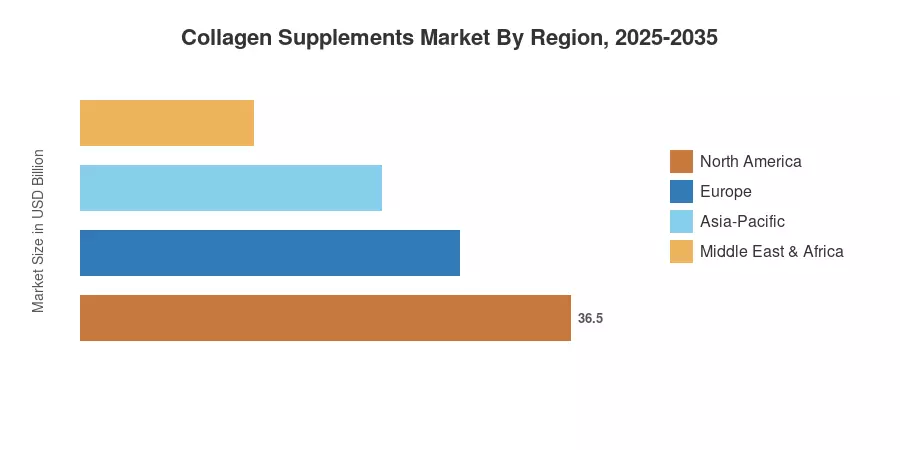

North America leads with a 36.4% revenue share, anchored by clinical-grade brand penetration in U.S. specialty channels. Asia-Pacific is the fastest-growing region at a 10.85% CAGR, fueled by Japanese and Korean beauty supplement trend culture, while Europe holds the second position on the strength of German and French sports nutrition brands. The next decade will be defined by ingredient transparency and clinical substantiation.

Key Report Takeaways

• By Product Type

- Powder formats commanded 54.6% of Collagen Supplements Market revenue in 2025, anchored by hydrolyzed collagen peptide powder bulk purchases through e-commerce

- Capsules and gummies will expand at a 9.45% CAGR through 2035, driven by convenience-oriented millennial buyers

- Drinks and liquid shots are reshaping single-serve consumption patterns in convenience retail

• By Source

- Animal-based ingredients held an 80.9% share of the Collagen Supplements Market in 2025, with bovine and marine sources dominating

- Plant-mimetic and fermentation-based formats are projected to grow at a 10.78% CAGR through 2035

• By Region

- North America captured USD 1.33 billion in 2025 revenue, led by the U.S. specialty retail channel

- Asia-Pacific will pace fastest at a 10.85% CAGR through 2035, with China and Japan leading volume gains

- Europe represented a 27.8% share in 2025, with collagen beauty supplement trend adoption strongest in Germany and France

Market Size and Forecast (2021–2035)

MRFR's market sizing draws on a triangulation framework combining manufacturer revenue disclosures, customs trade flows for hydrolyzed peptides (HS code 3504), retail scanner panel data (Nielsen, SPINS), and ingredient supplier shipment volumes. Year-over-year growth reflects post-pandemic normalization through 2022 and a re-acceleration phase from 2024 onward as collagen protein sports nutrition channels mature.

.webp?v=1783339559)