Coronary Stents Market Summary

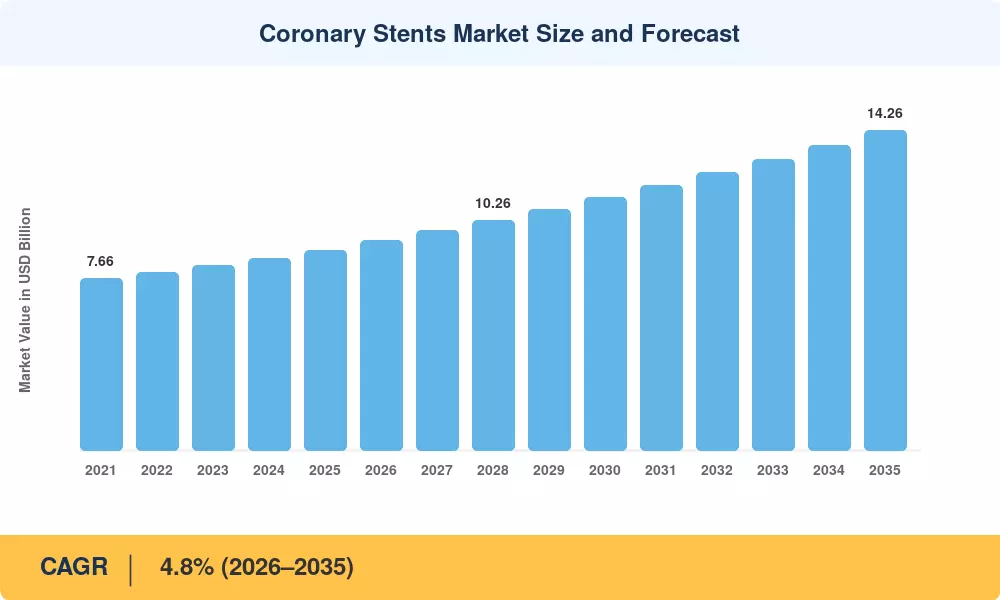

The Coronary Stents Market size was valued at USD 8.92 Billion in 2025, and the market is projected to grow from USD 9.35 Billion in 2026 to USD 14.26 Billion by 2035, registering a CAGR of 4.8% during the forecast period 2026–2035. Rising cardiovascular disease prevalence across aging populations and expanding insurance coverage in middle-income economies are anchoring procedure volumes. Government-led initiatives—such as India's Ayushman Bharat scheme and the U.S. Centers for Medicare & Medicaid Services (CMS) value-based reimbursement programs—continue to channel funding toward interventional cardiology infrastructure [1][2].

A technological shift is reshaping the Coronary Stents Market as legacy thick-strut platforms give way to ultrathin cobalt-chromium and platinum-chromium designs that reduce vessel injury and shorten antiplatelet therapy duration. AI-guided intravascular imaging, now embedded in catheterization lab workflows across more than 3,200 centers globally, improves lesion assessment precision and stent sizing accuracy [3]. The FDA cleared four next-generation stent platforms between 2023 and 2025, accelerating clinical adoption [4].

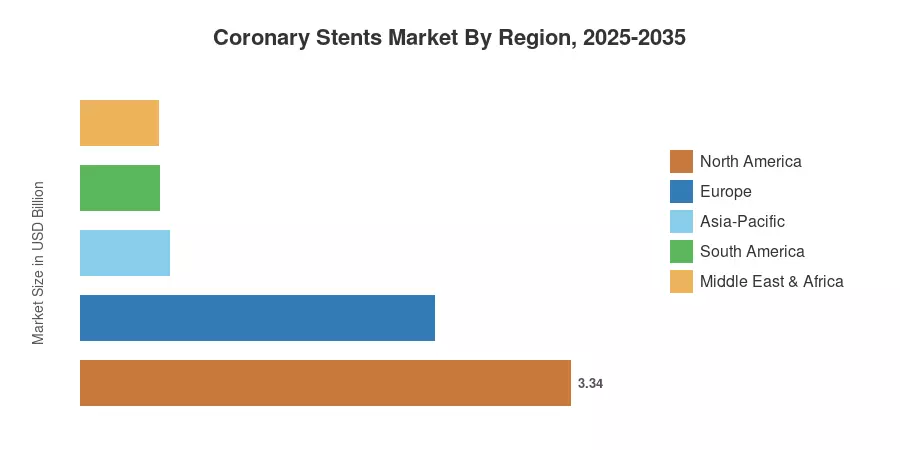

North America commanded approximately 37.4% of Coronary Stents Market revenue in 2025, supported by dense catheterization lab networks and favorable private-payer reimbursement. Asia-Pacific is the fastest-growing region at a projected 6.8% CAGR through 2035, driven by public procurement reforms in China and India that are lowering unit prices while pushing volume upward. Europe holds the second-largest share at roughly 27%, anchored by strong clinical trial ecosystems and CE-mark pathways that accelerate product launches.

Key Report Takeaways

• By Product Type

- Drug-Eluting Stent platforms accounted for approximately 70.3% of the Coronary Stents Market in 2025, reflecting clinician preference for controlled drug release and lower revascularization rates.

- Bioabsorbable Vascular Scaffolds are forecast to expand at an 8.1% CAGR through 2035, driven by growing demand for transient scaffolding in younger patient cohorts.

• By Biomaterial

- Metallic platforms represented 72.1% of Coronary Stents Market revenue in 2025, with cobalt-chromium alloys dominating the high-performance segment.

- Polymeric scaffolds are projected to grow at an 8.5% CAGR as bioresorbable polymer science matures.

• By Region

- North America led the Coronary Stents Market with a 37.4% revenue share in 2025.

- Asia-Pacific is advancing at a 6.8% CAGR through 2035, the fastest among all regions.

Coronary Stents Market Size and Forecast (2021–2035)

Market Research Future employs a bottom-up estimation model combining procedural volume data from national cardiovascular registries, average selling prices by stent category and region, and import-export trade statistics. Historical figures (2021–2024) are validated against company filings and hospital procurement databases; forecast values (2026–2035) apply segment-level growth assumptions adjusted for regulatory, demographic, and reimbursement trends.