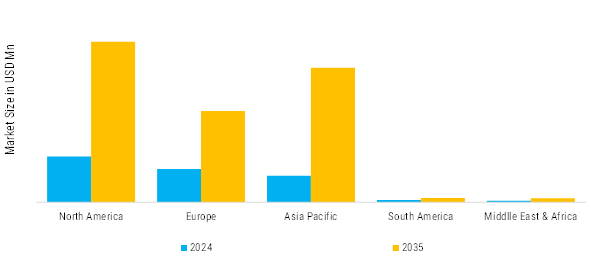

Data Center Cooling Market Summary

As per Market Research Future analysis, the Data Center Cooling Market size was valued at USD 11,730.21 Million in 2024. The Data Center Cooling market is projected to grow from USD 12,902.22 Million in 2025 to USD 42,301.45 Million by 2035, exhibiting a compound annual growth rate (CAGR) of 12.6% during the forecast period (2025 - 2035).

Key Market Trends & Highlights

The Data Center Cooling Market exhibits moderate growth amid supply constraints and rising demand from flame retardants and batteries

- AI and machine learning integration in cooling systems automate optimization, predicting heat loads and adjusting flows in real-time to cut energy.

- Free cooling and hybrid retrofits leverage ambient air or glycol loops to extend low-energy seasons, vital amid tightening carbon regulations.

- Hyperscalers like those building AI farms lead adoption, with dual-phase immersion targeting niche crypto and GPU clusters.

- Operators prioritize PUE reductions, with green hyperscale campuses backed by government incentives drawing billions in investment. Modular infrastructures like direct-to-chip coolers scale for hyperscale growth, accommodating AI's power spike.

Market Size & Forecast

| 2024 Market Size | 11,730.21 (USD Million) |

| 2035 Market Size | 42,301.45 (USD Million) |

| CAGR (2025 - 2035) | 12.6% |

Major Players

Schneider Electric, Vertiv, Rittal, Submer, Green Revolution Cooling, LiquidCool Solutions, Asetek, Trane Technologies, Daikin, Johnson Controls, Mitsubishi Electric, Carrier.