Diagnostic Imaging Market Summary

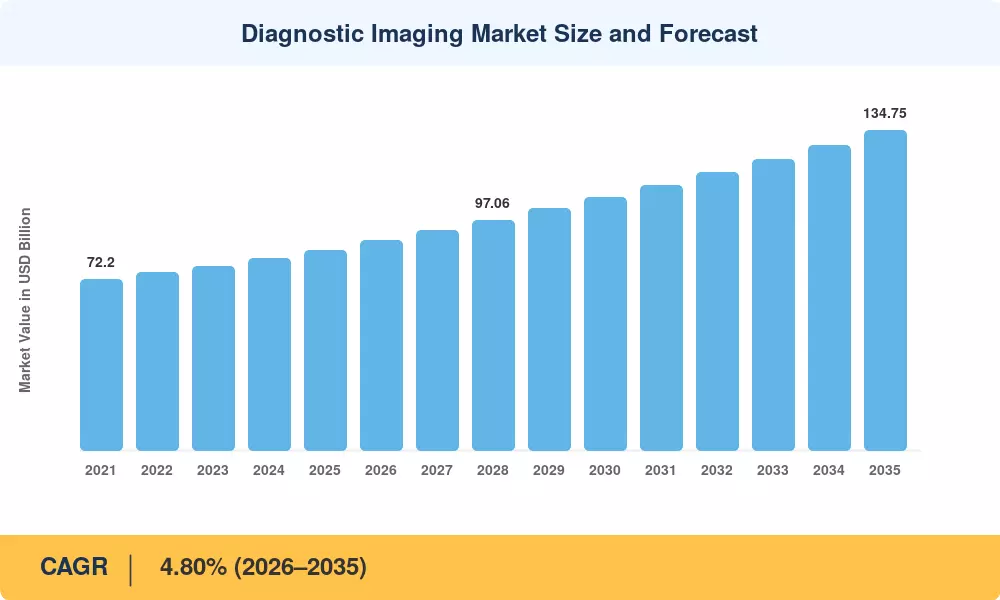

The global Diagnostic Imaging Market reached an estimated USD 84.40 billion in 2025, propelled by aging populations, rising chronic disease burdens, and sustained hospital capital-expenditure cycles across developed and emerging economies. From a 2026 starting value of USD 88.41 billion, Market Research Future (MRFR) projects the Diagnostic Imaging Market will grow at a 4.80% CAGR through 2035, reaching USD 134.75 billion. Government mandates around early cancer detection — including the European Commission's Beating Cancer Plan targeting 90% breast-screening coverage by 2025 and CMS reimbursement expansions for low-dose CT lung screening in the United States — have anchored demand at scale [1][2].

Clinical sites are changing the way they buy and deploy imaging assets through a technology change. Digital flat-panel detectors and AI-integrated reconstruction engines are replacing film-based and analog radiography systems, which are decreasing scan durations by 30–50% and reducing radiation dose [3]. The next platform change for the Diagnostic Imaging Market is photon counting CT, which gathers spectral energy data in a single acquisition and drew over USD 1.2 billion in combined R&D spend across key OEMs between 2022 and 2025 [4].

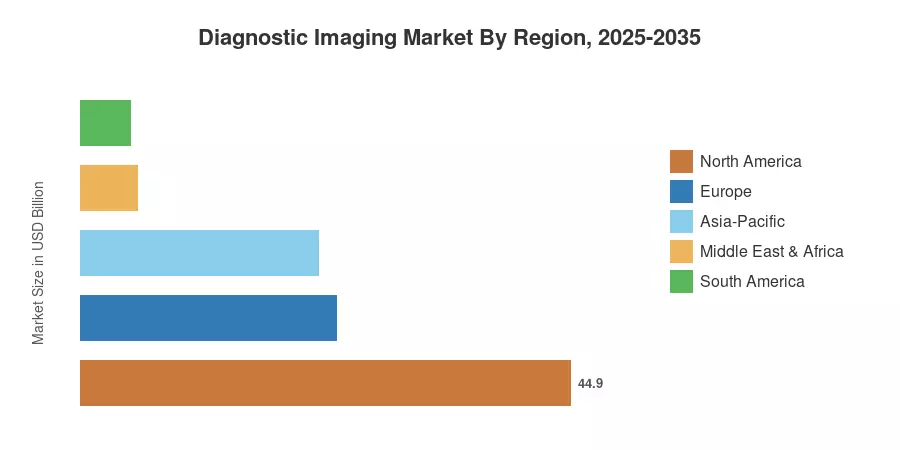

The revenue share of North America is 44.9%, driven by a dense installed base and the willingness of payers to reimburse sophisticated modalities. The Asia-Pacific area is the fastest expanding with a 5.9% CAGR led by government hospital development plans in India, China and Southeast Asia. Europe accounts for the second-largest proportion at 23.5%, as cross-border procurement procedures speed up equipment improvements. Diagnostic Imaging Market to grow at a steady mid-single-digit CAGR, driven by AI-enabled workflows and value-based reimbursement models changing site-of-care economics worldwide.

Key Report Takeaways

• By Modality

- X-ray anchored the Diagnostic Imaging Market with a 27.1% revenue share in 2025, reflecting high-volume emergency and orthopedic use cases across hospital and outpatient settings.

- Computed tomography is forecast to expand at a 6.8% CAGR through 2035, driven by photon-counting detector adoption and AI-assisted triage protocols.

- MRI is projected to surpass USD 22.50 billion by 2035 as ultra-high-field and helium-free magnet designs lower lifecycle costs.

• By Application

- Diagnostic applications accounted for 62.1% of the Diagnostic Imaging Market in 2025, spanning oncology, cardiology, and musculoskeletal evaluations.

- Therapeutic and interventional imaging is set to post a 7.1% CAGR through 2035, fueled by image-guided surgery and minimally invasive procedures.

• By End User

- Hospitals held 57.2% share in 2025, leveraging multimodality suites integrated with electronic health records.

- Diagnostic imaging centers are the fastest-growing end-user segment at a 7.6% CAGR, as payers steer referrals toward lower-cost freestanding sites.

• By Geography

- North America led the Diagnostic Imaging Market with a 44.9% share in 2025, supported by favorable reimbursement and technology-forward health systems.

- Asia-Pacific is expanding at a 5.9% CAGR as China and India scale domestic manufacturing and tier-2 hospital procurement.

Diagnostic Imaging Market Size and Forecast (2021–2035)

The Market Research Future (MRFR) sizing methodology combines bottom-up device-shipment statistics with top-down revenue tracking by geography and modality. Historical figures (2021–2024) are based on audited OEM disclosures and trade-association data; projection values (2026–2035) are based on a calibrated 4.80% CAGR adjusted for macro-demographic and technology-adoption assumptions.