Diagnostic Imaging Services Market Summary

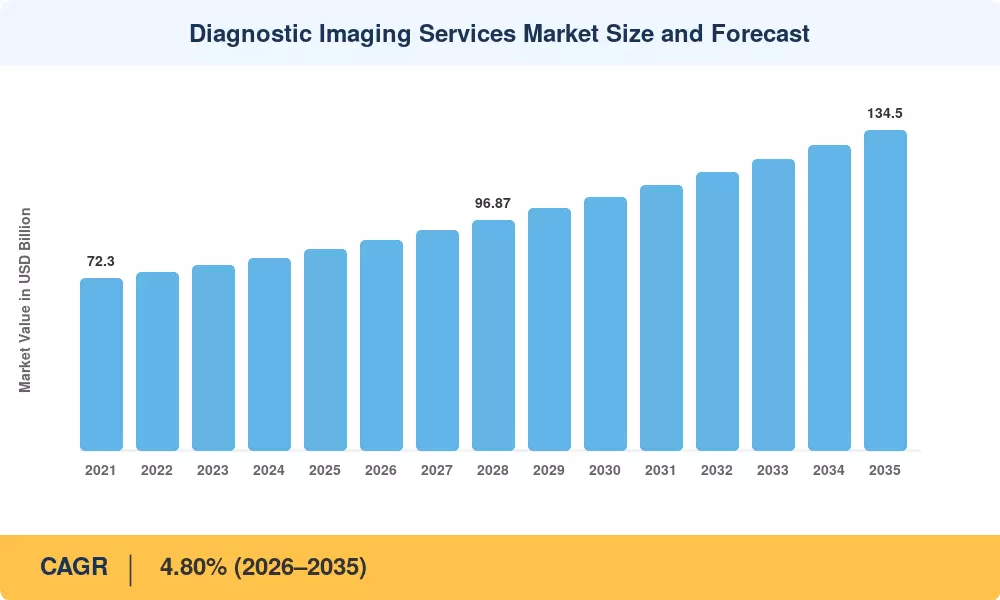

The Global Diagnostic Imaging Services Market size was valued at USD 84.40 Billion in 2025, and the market is projected to grow from USD 88.20 Billion in 2026 to USD 134.50 Billion by 2035, registering a CAGR of 4.80% during the forecast period 2026–2035. Two catalysts are accelerating this trajectory: the U.S. Centers for Medicare & Medicaid Services (CMS) expanded reimbursement coverage for advanced imaging modalities in 2024 [2], and Asia-Pacific governments collectively committed over USD 18 billion in hospital infrastructure funding between 2023 and 2025 [3]. These policy-driven capital flows are translating directly into higher scan volumes and wider geographic access across the Diagnostic Imaging Services Market.

The technology stack underpinning imaging services is shifting rapidly. Legacy analog X-ray and film-based workflows are giving way to fully digital, AI-augmented platforms that pair sub-second reconstruction with automated triage. GE HealthCare's 2024 rollout of its AI-embedded CT platform cut average read times by 34%, according to early clinical data [4]. Siemens Healthineers invested USD 1.2 billion in photon-counting CT development through 2025, signaling a generational shift in detector technology [5].

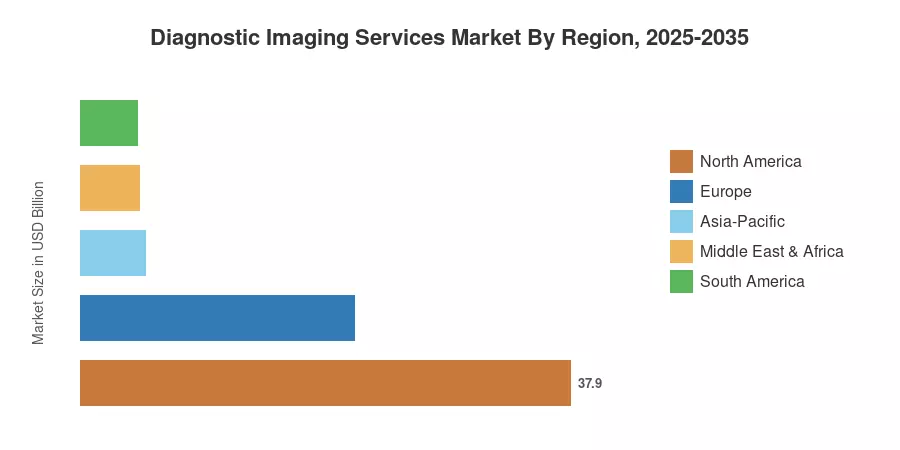

North America commanded a 44.90% revenue share in 2025, sustained by a dense installed base and robust payer reimbursement structures. Asia-Pacific is the fastest-growing region at a 5.95% CAGR through 2035, driven by government hospital expansion in India, China, and Southeast Asia. Europe held the second-largest share at 25.10%, anchored by universal healthcare mandates that guarantee imaging access. The Diagnostic Imaging Services Market is poised for sustained double-digit absolute growth as aging populations and chronic disease prevalence continue to elevate scan demand globally.

Key Report Takeaways

• By Modality

- X-ray anchored the largest modality share at 26.50% in 2025, driven by high-volume emergency and orthopedic use cases.

- Computed tomography is forecast to expand at a 6.85% CAGR through 2035, fueled by AI-assisted detection and faster scanner architectures.

- MRI services generated USD 18.70 billion in 2025, supported by neurological and oncological referral growth.

• By Application

- Diagnostic imaging accounted for a 62.10% share of the Diagnostic Imaging Services Market in 2025.

- Therapeutic and interventional imaging is projected to grow at a 7.10% CAGR through 2035, reflecting the shift toward image-guided procedures.

• By Region

- North America commanded 44.90% of the Diagnostic Imaging Services Market in 2025.

- Asia-Pacific is the fastest-growing region at a 5.95% CAGR to 2035.

- Europe contributed USD 21.19 Billion in 2025, led by Germany, the UK, and France.

Diagnostic Imaging Services Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a blend of primary interviews with hospital procurement directors, payer claims databases, OEM installation records, and regulatory filings across 42 countries. Historical figures (2021–2024) reflect audited revenue data; the 2025 base year uses validated Q4 2024 run-rate extrapolation. Forecast values (2026–2035) apply econometric modeling adjusted for demographic aging curves, reimbursement policy trajectories, and technology replacement cycles across the Diagnostic Imaging Services Market.