Digital Camera Market Summary

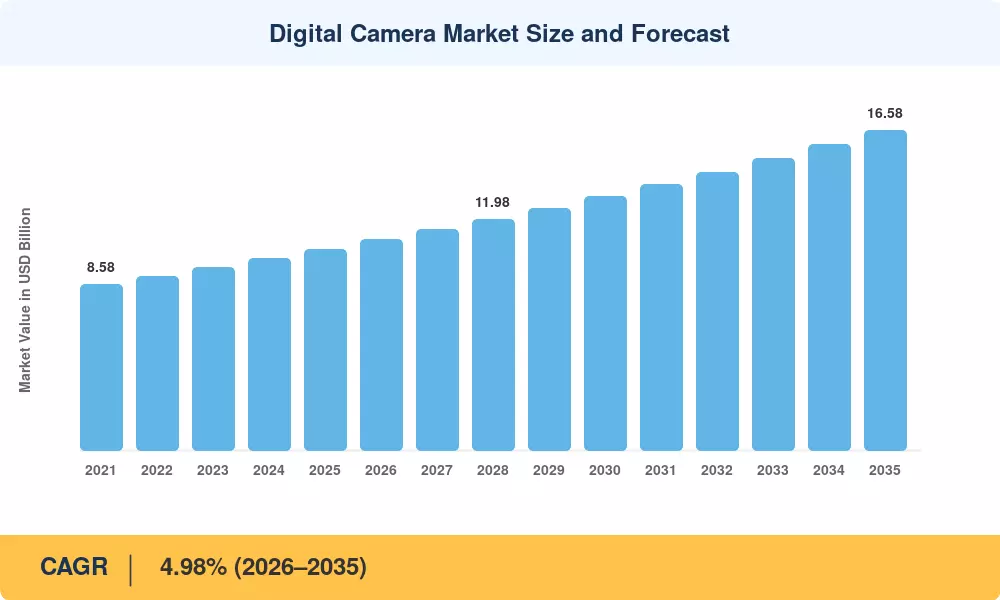

The Digital Camera Market was valued at USD 10.42 billion in 2025 and is projected to reach USD 10.93 billion in 2026 before climbing to USD 16.58 billion by 2035, registering a CAGR of 4.98% during 2026–2035. This trajectory reflects a structural pivot: manufacturers have abandoned the race to compete with smartphones on convenience and instead repositioned mirrorless full-frame digital camera systems as purpose-built instruments for professional creators. Canon's 22-year streak atop interchangeable-lens shipments [1] and Sony's aggressive R&D spend on computational autofocus and image stabilization underscore how premium hardware now commands rising average selling prices even as total unit volumes remain well below the smartphone era's peak.

A technology transformation is reshaping every price tier. Legacy DSLR sensor resolution and low-light performance advantages are migrating into lighter mirrorless bodies equipped with AI-driven subject tracking, in-body stabilization rated at seven-plus stops, and native 4K video-capable digital cameras that record internally at 10-bit color depth. The Camera & Imaging Products Association (CIPA) reported that interchangeable-lens camera shipment value rose 10% year-over-year in 2024 [2], confirming that the mix shift toward higher-value bodies and lenses more than offsets declining compact-camera volumes.

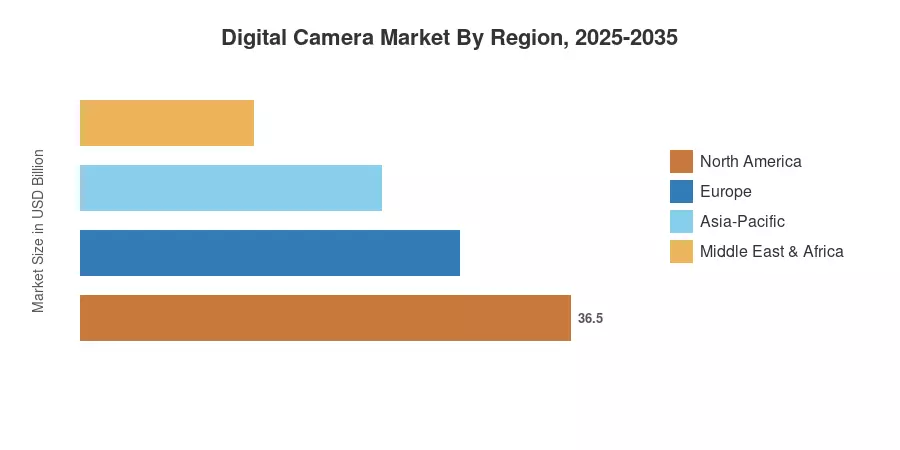

Asia-Pacific dominates the Digital Camera Market with an estimated 33.8% revenue share in 2025, fueled by Japan's manufacturing base and China's 213% surge in compact digital cameras for vlogging shipments [3]. Europe holds the second-largest share at roughly 27%, supported by travel-photography demand and strong prosumer adoption in Germany and the Nordic countries. The fastest-growing region is Asia-Pacific, advancing at a 6.18% CAGR through 2035. As creator-economy platforms proliferate globally, the Digital Camera Market is poised for sustained premiumization across all sensor tiers.

Key Report Takeaways

• By Camera Type

- Mirrorless systems captured 62.1% of the Digital Camera Market share in 2025, driven by the adoption of mirrorless full-frame digital camera systems among professional creators and filmmakers.

- Compact digital cameras for vlogging are advancing at a 4.22% CAGR through 2035 as live-stream integration and flip-screen designs attract social-media creators.

- DSLR sensor resolution and low-light performance remain relevant in sports and wildlife niches, but the segment's share is contracting year over year.

• By End User

- Content creators registered the fastest growth trajectory in the Digital Camera Market with a 6.92% CAGR through 2035, reflecting the monetization of short-form video.

- Professional photographers retained USD 3.72 billion in revenue in 2025, anchored by commercial, editorial, and wedding verticals.

• By Geography

- Asia-Pacific led the Digital Camera Market with 33.8% of global revenue in 2025.

- North America accounted for approximately USD 2.55 billion in 2025, underpinned by Hollywood production demand for 4K video-capable digital cameras.

MRFR's market-size estimates blend CIPA shipment data, manufacturer revenue filings, distributor channel checks, and proprietary demand modeling calibrated against macroeconomic indicators. Historical figures (2021–2024) rely on audited financials; the 2025 base year uses preliminary industry data; forecast values (2026–2035) apply a calibrated compound growth rate and scenario analysis.

.webp?v=1782888026)