Drip Irrigation Market Summary

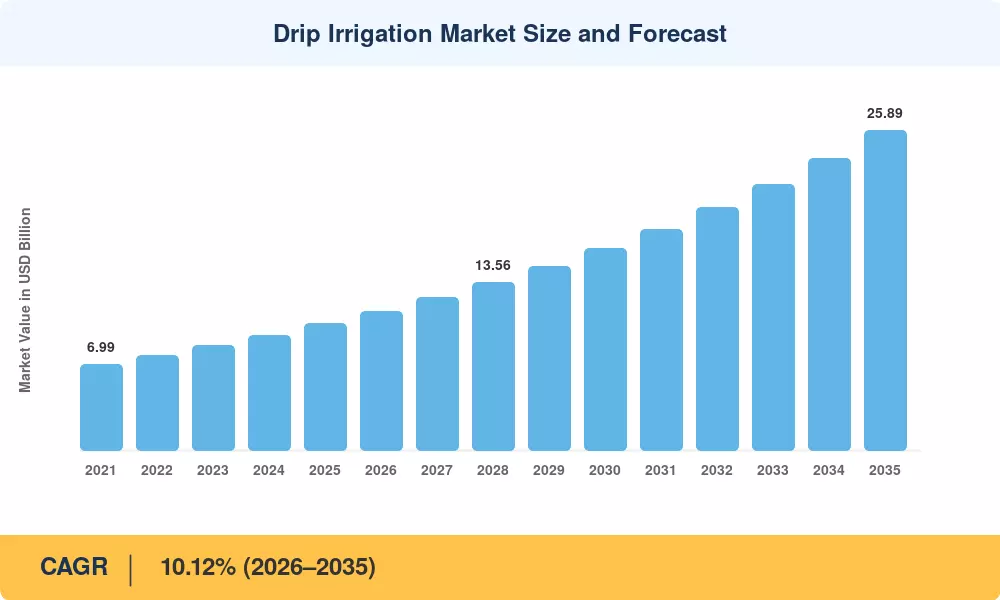

The Drip Irrigation Market stood at USD 10.28 billion in 2025 and is projected to reach USD 11.15 billion in 2026 before climbing to USD 25.89 billion by 2035, registering a CAGR of 10.12% across the forecast window. Two catalysts anchor this trajectory: India's Pradhan Mantri Krishi Sinchayee Yojana (PMKSY), which channels roughly USD 3.5 billion in cumulative micro-irrigation subsidies through 2028 [2], and the European Union's Common Agricultural Policy reform mandating a 25% reduction in freshwater abstraction for irrigated cropland by 2030 [3]. These policy levers compress payback periods for growers, turning precision water delivery agriculture from a long-horizon bet into a near-term operational upgrade.

A technological shift is altering the way water gets to the root zone. Legacy flood and furrow systems, which still represent an estimated 85% of irrigated hectares globally, are being progressively replaced with drip tape fertigation systems and micro drip emitter irrigation networks that reduce water consumption by 30–50% per hectare [4]. Smart drip irrigation automation platforms currently use soil-moisture sensors, weather APIs and variable-rate controllers to schedule watering cycles without manual intervention, reducing on-farm labor needs by up to 25% [5]. Investment in subsurface drip irrigation (SDI) sped up after California’s Sustainable Groundwater Management Act (SGMA) set basin-level extraction limits, with almond and pistachio growers beginning to refit entire blocks with underground drip lines [6].

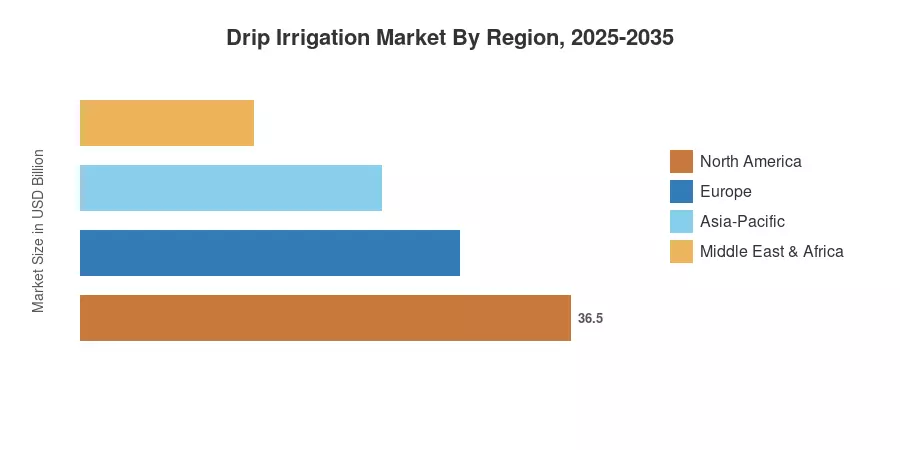

Asia-Pacific, with 45.0 share of the Drip Irrigation Market, anchors absolute demand with India’s subsidy architecture and China’s cotton-belt modernization program. Africa has the highest regional CAGR at 12.0%, driven by World Bank–financed climate-smart agriculture projects in East and West Africa [7]. Regionally, Europe is the second largest, and with water framework compliance and CAP eco-schemes, growers are being pushed towards precision water delivery agriculture. With growing freshwater stress on every continent, the Drip Irrigation Market is poised to be the go-to capital expenditure for irrigated agriculture by the mid-2030s.

Key Report Takeaways

• By Application

- Surface drip systems captured 72.0% of the Drip Irrigation Market revenue in 2025, reflecting the lower upfront cost per hectare for annual row crops.

- Subsurface drip irrigation SDI is projected to expand at a 12.5% CAGR through 2035 as permanent crop growers prioritize water savings and reduced tillage interference.

• By Component

- Drip tubes and drip tape fertigation system components accounted for USD 3.26 billion in 2025, anchoring the consumables segment.

- Controllers and sensors used in smart drip irrigation automation are forecast to log the highest component CAGR of 15.0% through 2035.

• By Geography

- Asia-Pacific led the Drip Irrigation Market with a 45.0% share in 2025, underpinned by India and China.

- Africa is poised for a 12.0% CAGR through 2035, the fastest among all regions.

- North America contributed USD 1.85 billion in 2025, driven by SGMA compliance and specialty-crop economics.

Drip Irrigation Market Size and Forecast (2021–2035)

The MARKET RESEARCH FUTURE market-sizing model triangulates manufacturer shipments, trade-flow statistics, and end-user surveys in 42 countries. Historical values (2021-2024) are cross-checked against customs databases and company reports. The 2025 base year is a blend of preliminary shipment data and channel checks. Forecast values (2026-2035) use a compound model based on expansion in irrigated area, subsidy disbursement timelines and technology adoption S-curves.

.webp?v=1785505180)