Energy as a Service Market Summary

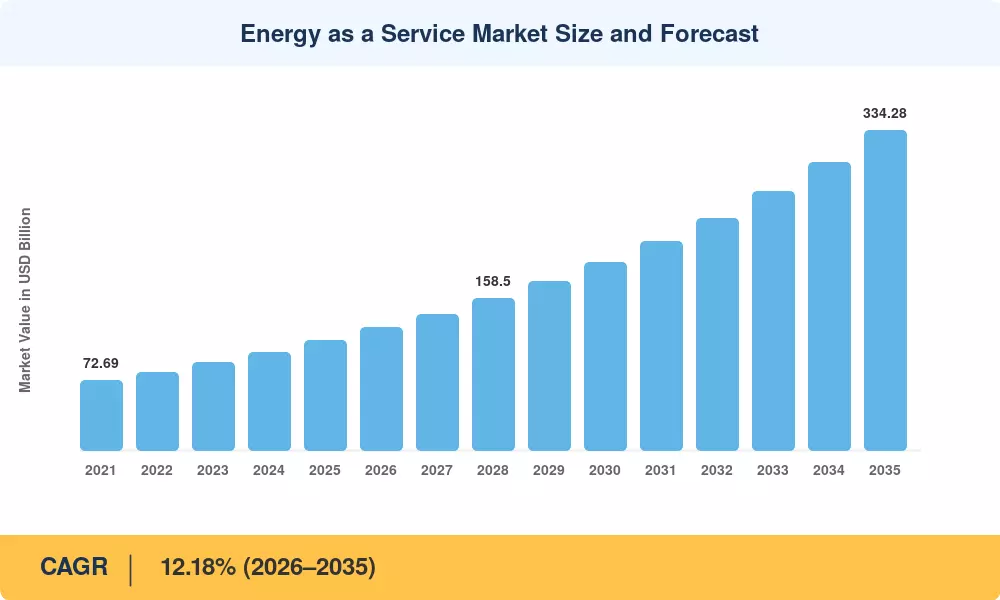

The Energy as a Service Market reached USD 115.12 Billion in 2025 and is projected to expand from USD 128.24 Billion in 2026 to USD 334.28 Billion by 2035, registering a CAGR of 12.18% across the forecast window. Corporate decarbonization pledges and the financial logic of converting capital expenditures into predictable operating costs are propelling demand for managed energy-as-a-service for commercial buildings. The Inflation Reduction Act alone unlocked over USD 369 Billion in clean-energy incentives, directly improving the unit economics of power-purchase agreements via EaaS providers and on-site solar and storage as a service contracts [2].

A structural technology shift is redefining how organizations procure and consume electricity. Legacy utility procurement—dominated by fixed tariffs and siloed asset ownership—is giving way to bundled subscription contracts that combine distributed generation, battery storage, intelligent load control, and real-time analytics. BloombergNEF estimates that global corporate clean-energy procurement surpassed 50 GW annually by 2024, with EaaS for renewable energy procurement accounting for a growing share of that volume [3]. Energy efficiency financing through EaaS models allows mid-market tenants to access upgrades previously limited to investment-grade portfolios.

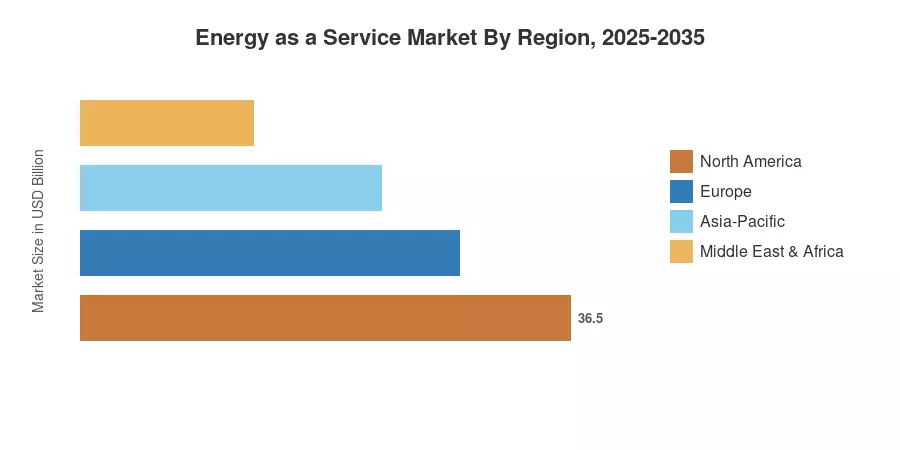

North America commanded roughly 45.1% of the Energy as a Service Market in 2025, underpinned by favorable tax-credit stacking and aggressive state-level renewable portfolio standards Asia-Pacific recorded the fastest regional CAGR at 17.62%, fueled by India's Production-Linked Incentive schemes and China's carbon-trading mandates. Europe held the second-largest share at approximately 26.3%, supported by the EU Energy Performance of Buildings Directive. The decade ahead will be defined by how quickly EaaS platforms scale AI-driven optimization and cross-border service delivery.

Key Report Takeaways

• By Service Type

- Energy Supply Services captured the largest segment of the Energy as a Service Market in 2025, accounting for 41.8% of global revenue

- Microgrid-as-a-Service is set to grow at a 15.2% CAGR through 2035, driven by resilience-focused procurement from hospital networks and data-center operators

- Energy Infrastructure Services generated approximately USD 27.4 Billion in 2025

• By Service-Delivery Model

- Pay-for-Service held 42.3% of the Energy as a Service Market share in 2025, reflecting enterprise preference for outcome-based contracts

- Leasing and Rental models are advancing at a 19.5% CAGR, making on-site solar and storage as a service accessible to smaller commercial tenants

• By Technology

- Distributed Generation represented 38.6% of the Energy as a Service Market in 2025

- EV-Charging Infrastructure is expanding at a 21.3% CAGR through 2035, as fleet electrification accelerates managed energy-as-a-service for commercial buildings

• By End User

- Commercial facilities accounted for 67.2% of 2025 revenue in the Energy as a Service Market

- Industrial customers are forecast to grow at a 14.8% CAGR to 2035

• By Region

- North America led the Energy as a Service Market with a 45.1% share in 2025

- Asia-Pacific registered the fastest CAGR at 17.62% through 2035

- --

MRFR's sizing methodology triangulates top-down revenue analysis (utility and vendor filings), bottom-up project-level aggregation, and secondary validation against IEA and BloombergNEF benchmarks[3]. Historical figures reflect actual contract values; forecast values incorporate policy-adjusted demand curves and technology cost-decline trajectories.