Enterprise Content Management Market Summary

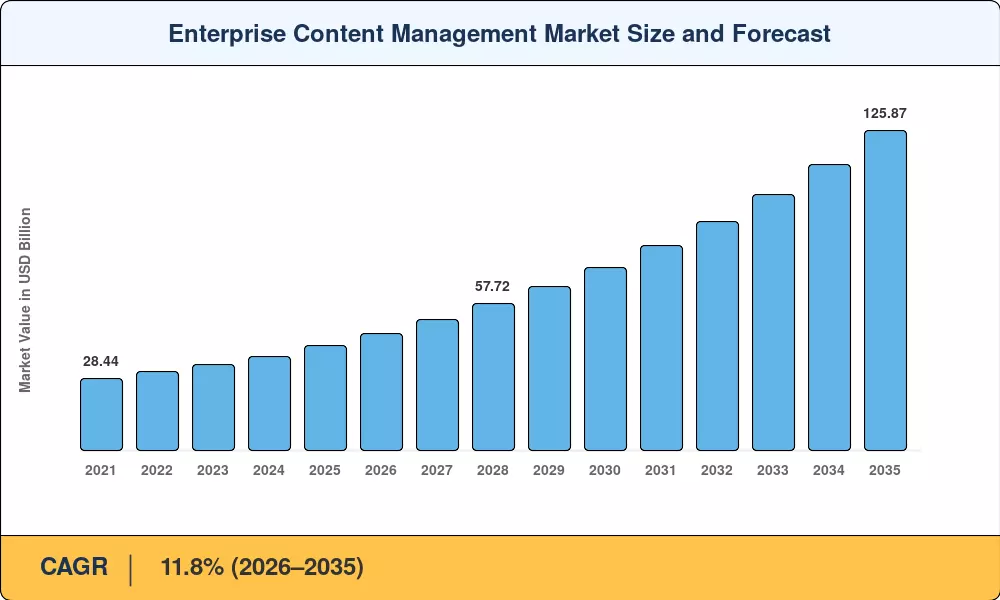

The Enterprise Content Management Market reached an estimated USD 41.25 Billion in 2025 and is projected to grow from USD 46.12 Billion in 2026 to USD 125.87 Billion by 2035, registering a CAGR of 11.8% during the forecast period. Two catalysts are accelerating this trajectory: the EU's Digital Operational Resilience Act (DORA), which took effect in January 2025 and compels financial institutions to maintain auditable digital records [1], and a wave of enterprise AI investment that exceeded USD 200 Billion globally in 2024, according to estimates [2]. These regulatory and technology forces are pushing organizations to replace aging file servers with platform-centric content architectures.

Legacy document repositories built in the early 2010s were designed for static storage, not for the AI-driven classification, auto-tagging, and workflow automation that modern operations demand. Enterprises now generate over 2.5 quintillion bytes of data daily, and roughly 80% of it is unstructured — contracts, invoices, clinical records, correspondence [3]. The shift toward intelligent document management and capture platforms capable of ingesting, classifying, and routing this content in real time represents the core technology transformation reshaping the Enterprise Content Management Market through 2035.

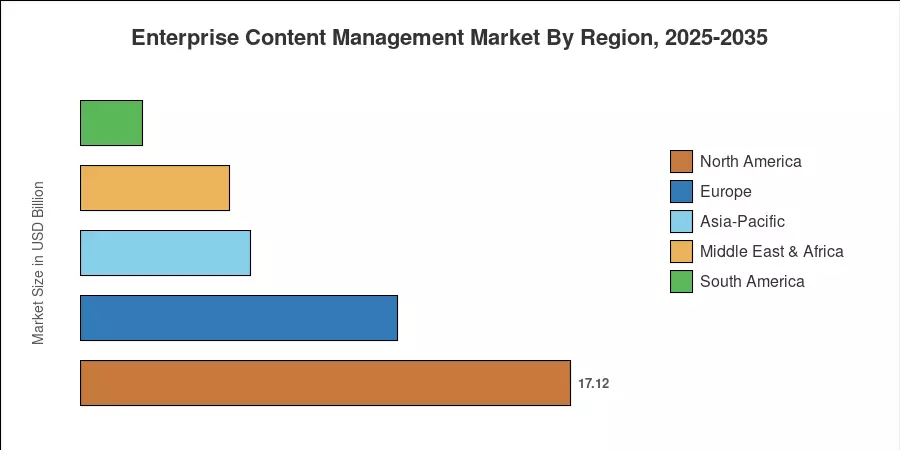

North America commanded a 41.5% revenue share of the Enterprise Content Management Market in 2025, anchored by early cloud adoption and stringent compliance mandates across financial services and healthcare. Asia-Pacific is the fastest-growing region at a 14.4% CAGR, fueled by government digitization programs in India, China, and ASEAN economies. Europe held the second-largest share at 26.8%, driven by GDPR enforcement and cross-border data residency requirements. The next decade will reward vendors that marry hyper-automation with sovereign-cloud compliance across these geographies.

Key Report Takeaways

• By Solution Type

- Document Management held a 30.2% revenue share of the Enterprise Content Management Market in 2025, reflecting deep adoption in compliance-heavy verticals.

- Digital Asset Management is poised to grow at a 14.3% CAGR through 2035, driven by media-rich workflows in retail and e-commerce.

• By Deployment Mode & Enterprise Size

- On-Premises deployment captured 57.1% of 2025 revenue, as regulated industries maintained on-site control over sensitive records.

- Small and Medium Enterprises are expanding at a 14.1% CAGR in the Enterprise Content Management Market, enabled by token-based and subscription pricing models.

• By Region

- North America led the Enterprise Content Management Market with a 41.5% share in 2025.

- Asia-Pacific is forecast to register the highest CAGR of 14.4% through 2035, with India and China as primary growth engines.

- BFSI accounted for a 24.1% share of end-user spending in 2025, reflecting intensive regulatory documentation requirements.

Market Size and Forecast (2021–2035)

Market Research Future's estimates combine bottom-up revenue analysis of leading vendors, regional IT spending benchmarks from the World Bank and OECD, and proprietary primary interviews with enterprise CIOs and content platform architects. Historical figures (2021–2024) are validated against vendor filings and IT spending data, while the forecast trajectory (2026–2035) applies regression-adjusted growth modeling calibrated to macro indicators and adoption curve analysis.