Web Content Management Market Summary

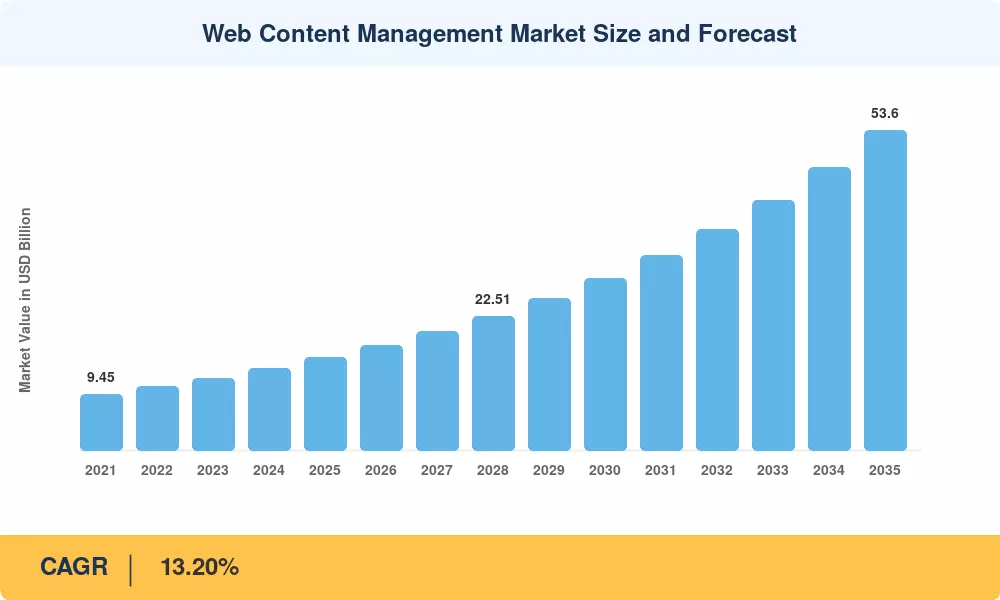

The Web Content Management Market reached an estimated USD 15.52 Billion in 2025 and is projected to climb from USD 17.57 Billion in 2026 to USD 53.60 Billion by 2035, advancing at a 13.20% CAGR across the forecast window. Two catalysts stand behind this trajectory: the global tightening of data-privacy regulations — GDPR enforcement fines alone surpassed EUR 4.2 Billion cumulatively by late 2024 [1] — and enterprise mandates to deliver consistent omnichannel customer journeys. Organizations that once treated web publishing as a marketing side project now view it as core digital infrastructure.

A decisive technology shift is reshaping the Web Content Management Market. Monolithic, server-rendered platforms are yielding to API-first and composable architectures that decouple the content repository from the presentation layer. estimated that enterprises allocating more than 30% of IT budgets to composable DX stacks grew 1.7× faster in revenue than peers during 2023–2024 [2]. Cloud-native deployment, AI-driven content tagging, and automated accessibility remediation are no longer premium add-ons — they are table-stakes capabilities buyers demand in every RFP.

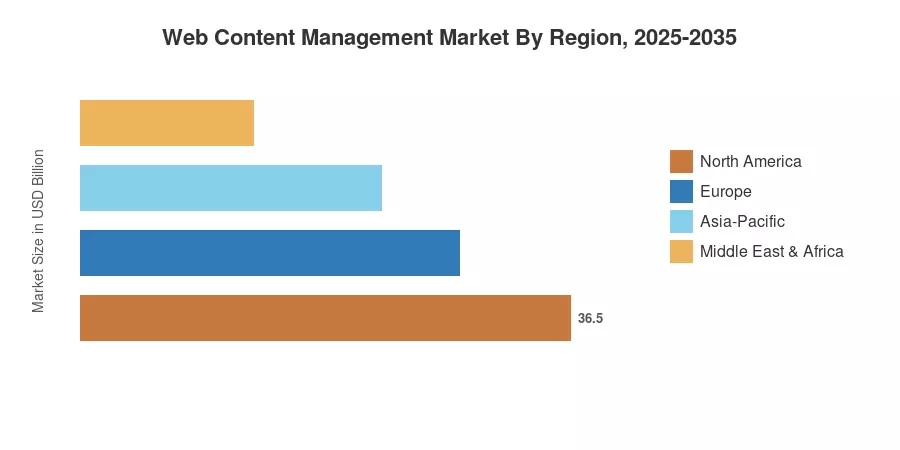

North America held roughly 37.0% of the Web Content Management Market revenue in 2025, anchored by hyperscaler cloud adoption and a mature SaaS ecosystem. Asia-Pacific is the fastest-growing region, tracking a 20.6% CAGR to 2035, propelled by digitalization programs across India, China, and Southeast Asia. Europe represents the second-largest block at approximately 27.5% share, where GDPR and the upcoming EU Accessibility Act continue to drive platform upgrades. As AI capabilities mature and regulatory complexity deepens, the Web Content Management Market is set for sustained double-digit expansion well into the next decade.

Key Report Takeaways

• By Component

- Solutions accounted for approximately 61.2% of the Web Content Management Market in 2025, driven by integrated AI authoring, digital asset management, and analytics modules.

- Services are projected to register a 21.0% CAGR through 2035 as enterprises seek implementation consulting and managed-service partnerships.

• By Deployment & Application

- Cloud deployment captured roughly 51.0% of the Web Content Management Market share in 2025.

- Personalized Customer Experiences is the fastest-growing application segment at a 23.2% CAGR, reflecting investment in real-time behavioral targeting.

• By Industry

- Retail and e-commerce commanded an estimated 28.6% vertical share in 2025.

• By Region

- North America led global revenue, while Asia-Pacific is expanding at the steepest CAGR among all regions.

Market Size and Forecast (2021–2035)

Market Research Future derives historical values from vendor financial disclosures and third-party IT spending surveys, then applies proprietary econometric modelling calibrated against macroeconomic and enterprise-adoption indicators to project the forecast period. All figures are in USD Billion at constant 2025 exchange rates.