Flame Retardants Market Summary

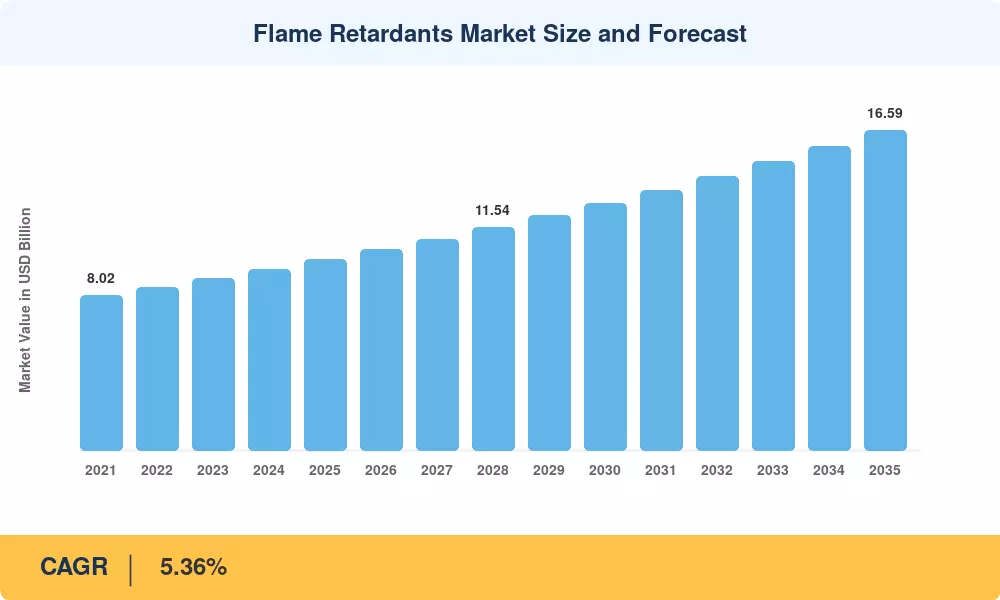

The Flame Retardants Market was valued at USD 9.88 billion in 2025 and is projected to reach USD 10.38 billion in 2026 before climbing to USD 16.59 billion by 2035, registering a CAGR of 5.36% during the forecast period. Tightening building-code standards across the European Union and new fire-safety mandates for electric vehicle battery enclosures under China's GB 38031 revision are two catalysts underpinning steady demand expansion. Regulatory pressure on brominated chemistries — amplified by REACH Annex XIV additions and EPA risk evaluations — continues to redirect procurement budgets toward aluminum hydroxide, phosphorus-based, and nitrogen-synergist systems [1][2].

A fundamental shift in chemistry is altering the flame-retardant market. Non-halogenated alternatives, which currently account for about 69.6% of global consumption, are displacing once-dominant legacy halogenated formulations. The EU's Construction Products Regulation (CPR) amendment, which is anticipated to affect over EUR 500 billion worth of building materials by 2030 and expedite the replacement cycle, especially favors low-smoke, low-toxicity additives [3]. Technologies for ultra-fine precipitated alumina trihydrate and microencapsulated red phosphorus are evolving simultaneously, enabling higher additive loadings without compromising polymer melt-flow properties.

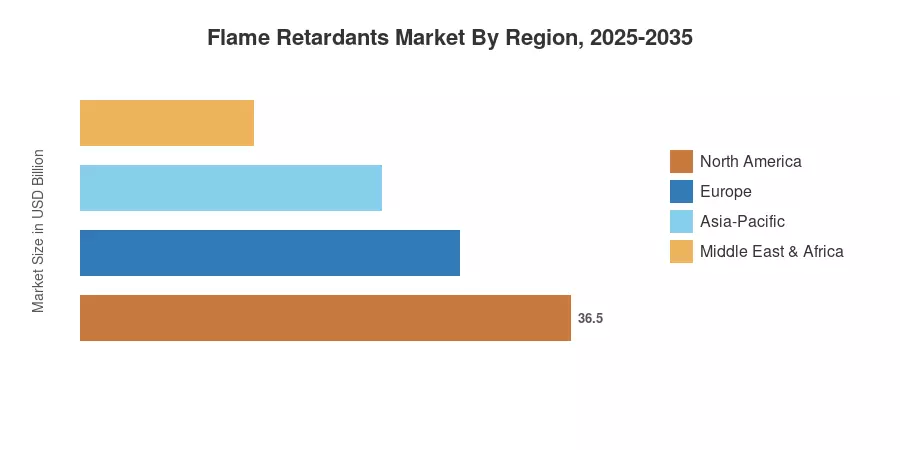

Due to significant infrastructure improvements and the density of electronics production, the Asia-Pacific has the fastest CAGR of 6.09% through 2035 and accounts for 47.1% of the Flame Retardants Market revenue. Europe makes up 24.2% of the global demand because of the stringent EN 13501 fire-classification requirements. Thanks to reshoring activity in semiconductor manufacturing and IBC code modifications, North America completes the top three with a 19.5% share. The volume should rise over the next ten years as the demands of urbanization, electrification, and sustainability come together.

Key Report Takeaways

• By Product Type

- Non-halogenated flame retardants captured 69.6% of the Flame Retardants Market in 2025, reflecting the broad shift away from brominated and chlorinated systems.

- Halogenated flame retardants are projected to register a CAGR of 3.48% through 2035, sustained by cost-sensitive wire-and-cable applications.

• By Application

- Polyolefins represented the largest application segment in the Flame Retardants Market, generating USD 3.88 billion in 2025.

- Polyurethane applications are advancing at a CAGR of 5.66% through 2035, propelled by construction foam insulation demand.

• By End-User Industry

- Building and construction held 37.0% of the Flame Retardants Market share in 2025, anchored by global infrastructure investment exceeding USD 2.5 trillion annually.

- Electrical and electronics end users are expanding at a 5.66% CAGR to 2035 as 5G infrastructure and EV power electronics proliferate.

• By Region

- Asia-Pacific commanded 47.1% of the Flame Retardants Market in 2025 and remains the fastest-growing region.

- Europe accounted for USD 2.39 billion in 2025 revenue, led by Germany, France, and the Nordic bloc.

Flame Retardants Market Size and Forecast (2021–2035)

Market Research Future estimates leverage primary supplier interviews, trade-flow analysis, and downstream polymer-consumption modeling, cross-validated against public financial disclosures and regional customs data. Historical values (2021–2024) reflect actual shipment volumes; 2025 is the base year, and 2026–2035 projections apply a calibrated CAGR of 5.36%.