Certified Global Research Member

Key Questions Answered

- Global Market Outlook

- In-depth analysis of global and regional trends

- Analyze and identify the major players in the market, their market share, key developments, etc.

- To understand the capability of the major players based on products offered, financials, and strategies.

- Identify disrupting products, companies, and trends.

- To identify opportunities in the market.

- Analyze the key challenges in the market.

- Analyze the regional penetration of players, products, and services in the market.

- Comparison of major players’ financial performance.

- Evaluate strategies adopted by major players.

- Recommendations

Why Choose Market Research Future?

- Vigorous research methodologies for specific market.

- Knowledge partners across the globe

- Large network of partner consultants.

- Ever-increasing/ Escalating data base with quarterly monitoring of various markets

- Trusted by fortune 500 companies/startups/ universities/organizations

- Large database of 5000+ markets reports.

- Effective and prompt pre- and post-sales support.

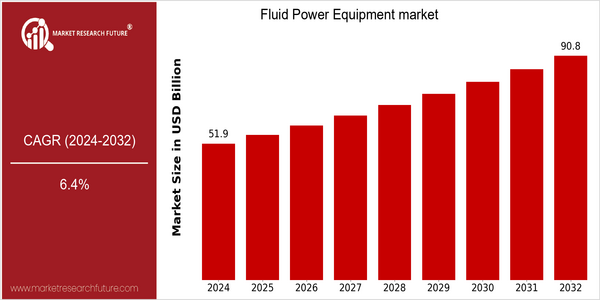

Market Size Snapshot

| Year | Value |

|---|---|

| 2024 | USD 51.85 Billion |

| 2032 | USD 90.76 Billion |

| CAGR (2024-2032) | 6.4 % |

Note – Market size depicts the revenue generated over the financial year

The global Fluid Power Equipment market is poised for significant growth, with a current market size of USD 51.85 billion in 2024, projected to reach USD 90.76 billion by 2032. This represents a robust compound annual growth rate (CAGR) of 6.4% over the forecast period. The increasing demand for automation across various industries, coupled with advancements in hydraulic and pneumatic technologies, is driving this upward trend. As industries seek to enhance efficiency and reduce operational costs, fluid power systems are becoming integral to modern manufacturing and construction processes. Key factors contributing to this market expansion include the rising adoption of electric and hybrid systems, which offer improved energy efficiency and lower emissions. Additionally, the growing emphasis on sustainable practices is prompting companies to invest in innovative fluid power solutions. Major players in the market, such as Parker Hannifin, Bosch Rexroth, and Eaton, are actively engaging in strategic initiatives, including partnerships and product launches, to enhance their market presence and meet evolving customer needs. For instance, recent collaborations aimed at integrating IoT technologies into fluid power systems are expected to further propel market growth by enabling smarter, more efficient operations.

Regional Market Size

Regional Deep Dive

The Fluid Power Equipment market is characterized by its diverse applications across various industries, including manufacturing, construction, and automotive. In North America, the market is driven by technological advancements and a strong emphasis on automation and efficiency. Europe showcases a robust regulatory framework that promotes sustainability and innovation, while the Asia-Pacific region is witnessing rapid industrialization and urbanization, leading to increased demand for fluid power solutions. The Middle East and Africa are experiencing growth due to infrastructural developments, and Latin America is focusing on modernization and energy efficiency in its fluid power systems.

Europe

- The European Union's Green Deal is influencing the fluid power market by mandating stricter emissions standards, prompting companies like Bosch Rexroth to develop eco-friendly hydraulic solutions.

- Innovations in digital hydraulics are gaining traction, with firms such as Moog Inc. investing in research to enhance system efficiency and reduce energy consumption.

Asia Pacific

- China's Belt and Road Initiative is driving significant investments in infrastructure, leading to increased demand for fluid power equipment in construction and manufacturing sectors.

- The rise of electric vehicles in countries like Japan and South Korea is prompting fluid power companies to adapt their technologies, with firms like Kawasaki Heavy Industries exploring hybrid systems.

Latin America

- Brazil's focus on renewable energy sources is driving innovation in fluid power systems, with companies like WEG Industries developing hydraulic solutions for wind and solar applications.

- Government initiatives aimed at modernizing infrastructure are creating opportunities for fluid power equipment suppliers, particularly in the construction and agricultural sectors.

North America

- The rise of Industry 4.0 has led to increased investments in automation technologies, with companies like Parker Hannifin and Eaton Corporation leading the charge in developing smart fluid power solutions.

- Regulatory changes aimed at reducing carbon emissions are pushing manufacturers to innovate, with the U.S. Department of Energy promoting energy-efficient hydraulic systems.

Middle East And Africa

- The UAE's Vision 2021 is fostering growth in the fluid power market by promoting advanced manufacturing technologies and sustainable practices.

- Saudi Arabia's National Industrial Development and Logistics Program is expected to boost demand for fluid power equipment in various sectors, including oil and gas.

Did You Know?

“Did you know that fluid power systems can achieve energy efficiencies of up to 90% when properly designed and maintained?” — International Fluid Power Society

Segmental Market Size

The Fluid Power Equipment market segment, encompassing hydraulic and pneumatic systems, plays a crucial role in various industries, including manufacturing, construction, and automotive. This segment is currently experiencing stable growth, driven by increasing automation and the need for efficient power transmission solutions. Key factors propelling demand include the rising emphasis on energy efficiency and the growing adoption of smart technologies in industrial applications. Currently, the adoption stage of fluid power equipment is in a mature phase, with companies like Bosch Rexroth and Parker Hannifin leading the way in innovative solutions. Notable applications include robotics in manufacturing, where hydraulic systems enhance precision and speed, and construction equipment that relies on pneumatic systems for operation. Macro trends such as sustainability initiatives and government regulations promoting energy-efficient technologies further catalyze growth in this segment. Technologies like IoT-enabled sensors and advanced control systems are shaping the evolution of fluid power equipment, enabling real-time monitoring and optimization of performance.

Future Outlook

The Fluid Power Equipment market is poised for significant growth from 2024 to 2032, with a projected market value increase from $51.85 billion to $90.76 billion, reflecting a robust compound annual growth rate (CAGR) of 6.4%. This growth trajectory is underpinned by the rising demand for automation across various industries, including manufacturing, construction, and agriculture, where fluid power systems are integral to enhancing operational efficiency and productivity. As industries increasingly adopt smart technologies and IoT solutions, the penetration of fluid power equipment is expected to rise, with usage rates potentially reaching over 60% in key sectors by 2032, driven by the need for more efficient and reliable power transmission systems. Key technological advancements, such as the development of energy-efficient hydraulic systems and the integration of digital controls, are set to reshape the landscape of the fluid power equipment market. Additionally, stringent environmental regulations and a growing emphasis on sustainability are prompting manufacturers to innovate and adopt eco-friendly practices, further propelling market growth. Emerging trends, including the shift towards electrification and hybrid systems, are expected to create new opportunities for market players, as they adapt to changing consumer preferences and regulatory frameworks. Overall, the Fluid Power Equipment market is on a promising path, characterized by innovation and a strong alignment with global industrial trends.

Covered Aspects:| Report Attribute/Metric | Details |

|---|---|

| Market Size Value In 2022 | USD 25.12 Billion |

| Growth Rate | 6.01% (2022-2030) |

Fluid Power Equipment Market Highlights:

Leading companies partner with us for data-driven Insights

Kindly complete the form below to receive a free sample of this Report

Tailored for You

- Dedicated Research on any specifics segment or region.

- Focused Research on specific players in the market.

- Custom Report based only on your requirements.

- Flexibility to add or subtract any chapter in the study.

- Historic data from 2014 and forecasts outlook till 2040.

- Flexibility of providing data/insights in formats (PDF, PPT, Excel).

- Provide cross segmentation in applicable scenario/markets.