Horticulture Lighting Market Summary

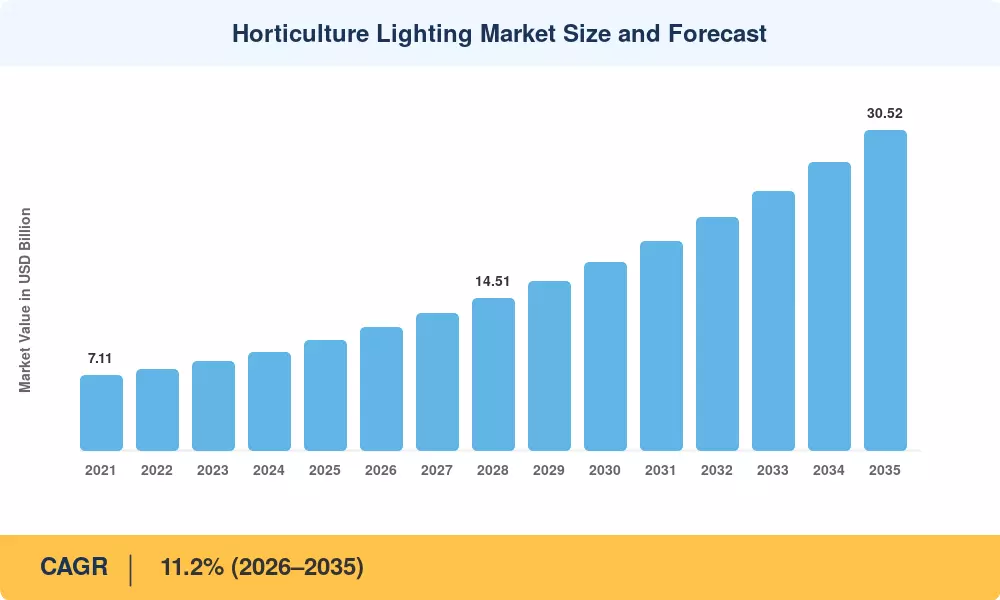

The global Horticulture Lighting Market reached an estimated USD 10.46 Billion in 2025, is projected to hit USD 11.74 Billion by 2026, and is forecast to grow to USD 30.52 Billion by 2035 at a CAGR of 11.2% during the 2026–2035 forecast window. Two catalysts are accelerating this trajectory: the wave of cannabis legalization across North American states—now encompassing over 40 U.S. jurisdictions with regulated adult-use programs—and the European Union's Fit-for-55 legislative package, which mandates aggressive energy-efficiency retrofits across commercial agriculture [1][2]. Together, these policy forces are pulling capital into advanced lighting systems at a pace the industry has rarely witnessed.

The technology backbone of the Horticulture Lighting Market is shifting decisively away from legacy high-intensity discharge (HID) fixtures toward precision-tuned LED platforms. Samsung and LG Innotek have scaled semiconductor wafer production to a point where fixture prices dropped an estimated 15–20% between 2024 and 2025, lowering the total cost of ownership for commercial growers [3]. Hardware commoditization, in turn, is pushing vendors upstream into cloud-based spectral analytics and subscription lighting-as-a-service models—a strategic pivot that mirrors broader platform-economy trends across industrial technology.

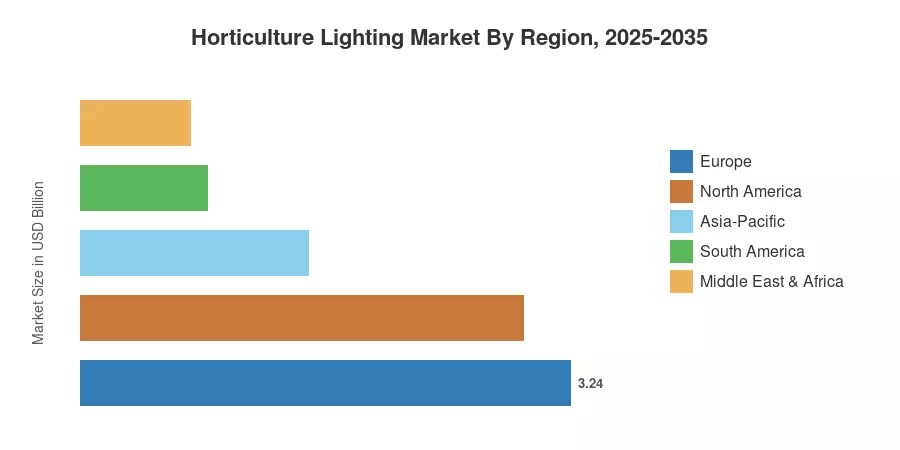

Europe remains the dominant region, accounting for roughly 31% of global Horticulture Lighting Market revenue in 2025, underpinned by Dutch greenhouse innovation and Scandinavian vertical-farm investment [4]. Asia-Pacific is the fastest-growing region with a projected CAGR of 14.4%, fueled by urban food-security mandates in Chinese and Japanese megacities. North America holds the second-largest share at approximately 28%, driven by cannabis cultivation infrastructure build-outs. The decade ahead will hinge on whether software-driven spectral intelligence can unlock yield improvements large enough to justify premium price points as LED hardware approaches commodity status.

Key Report Takeaways

• By Technology

- LED systems commanded approximately 81% of the Horticulture Lighting Market in 2025, reinforcing their position as the default fixture across commercial grow operations.

- Plasma and alternative light sources are projected to expand at a 13.4% CAGR through 2035, driven by research environments requiring continuous-spectrum output.

• By Offering

- Hardware revenue represented roughly 67% of the Horticulture Lighting Market in 2025, though software and services are gaining share at a 13.4% CAGR.By Installation

- Retrofit installations are forecast to grow at a 14.4% CAGR as growers replace aging HID systems under energy-efficiency mandates.

• By Region

- Europe held a 31% share of the Horticulture Lighting Market in 2025, led by the Netherlands, Germany, and the Nordic countries.

- Asia-Pacific is projected to register a 14.4% CAGR, the fastest among all regions.

- North America contributed approximately USD 2.93 Billion in 2025 revenue.

Horticulture Lighting Market Size and Forecast (2021–2035)

Market Research Future's estimates blend primary supply-side data (manufacturer shipment records, channel surveys) with demand-side validation (grower CapEx disclosures, utility rebate databases). Historical figures are reconciled against customs trade codes and semiconductor production indices, while the forecast applies a bottom-up build across six segmentation dimensions calibrated to regional policy timelines.